Analysts from Genghis Capital have prophesized a potential in the East African Breweries stock, projecting its price at 207.5 shillings per share, an upside of 18.6 percent.

“Against our FY22 estimates, we see a significant potential on the counter with an 18.6 percent upside based on a target price of 207.50 shillings,” said Genghis in their latest report.

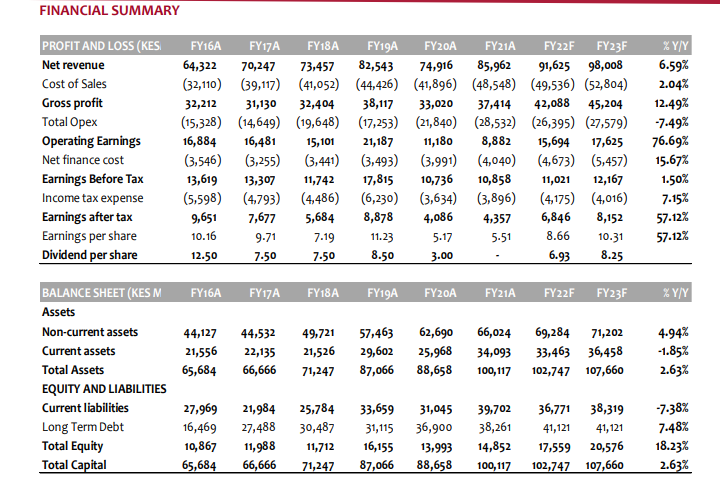

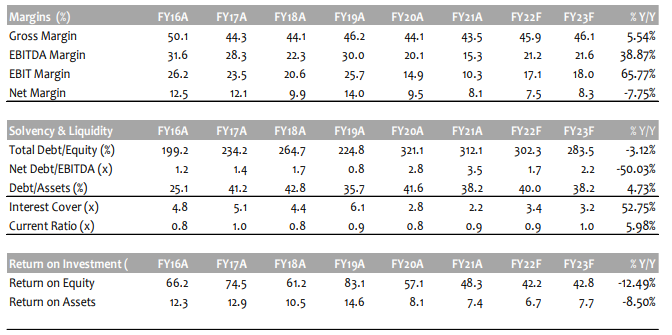

For the FY22, analysts estimate that the EPS will grow 57.12 percent y/y to 8.66 shillings driven by a 6.59 percent y/y rise in net revenue. This rise is on the back of the gradual ease in containment measures in Kenya and Uganda, which we foresee as a major boost to the on-trades.

“In line with this, we project an increased revenue contribution by Tanzania and Uganda to 16.9 and 19.7 percent, respectively,” they added.

Kenya is estimated to register a 2.42 percent y/y growth in net sales to about 58.1 billion shillings. Kenya’s aggregate contribution is however projected to decline.

The net revenues for EABL are projected that they will come in at 91.6 billion shillings Kenya is prognosticated to lead the pack with an estimated net revenue of 58.1 billion shillings (+2.42% y/y) with Uganda and Tanzania coming in at about 18.1 billion shillings (+10.75% y/y) and KES 15.4Bn (+19.65% y/y), respectively.

From a growth perspective, Tanzania takes center stage and analysts opine that in FY24, there will be parity in revenue contributions for the Uganda and Tanzania businesses.

The key driver to the forecasted stellar growth in Tanzania is the vibrancy of the Serengeti Brands (+19% y/y in FY20 and +12% y/y in FY21), coupled with EABL’s increased stake in Serengeti Breweries Limited (SBL) that promises more returns in the future.

“That said, we expect the Kenyan market to remain key to the business in both the near and long term with a lion share of revenue contribution albeit modest growth.”

“We expect a strong performance by mainstream spirits in the ongoing financial year on the back of their resilience to the pandemic (+23% y/y in FY21) and affordability against the backdrop of a relatively lenient price revision in mainstream spirits.”