During the week, the equities market was on an upward trajectory, with both NASI and NSE 25 gaining by 1.7%, while NSE 20 gained by 0.9%.

This took their YTD performance to gains of 7.1% and 5.4% for NASI and NSE 25, respectively, while NSE 20 declined by 0.9% on a YTD basis.

The equities market performance was driven by gains recorded by large-cap stocks such as KCB, Co-operative bank, Safaricom, and Equity of 5.1%, 3.4%, 2.0%, and 1.9%, respectively.

The gains were however weighed down by losses recorded by other large-cap stocks such as Standard Chartered Bank and EABL which declined by 1.6% and 0.7%, respectively.

During the week, equities turnover increased by 10.8% to USD 35.0 mn, from USD 31.6 mn recorded the previous week, taking the YTD turnover to USD 1.2 bn.

Foreign investors remained net sellers, with a net selling position of USD 12.5 mn, from a net selling position of USD 5.7 mn recorded the previous week, taking the YTD net selling position to USD 80.4 mn.

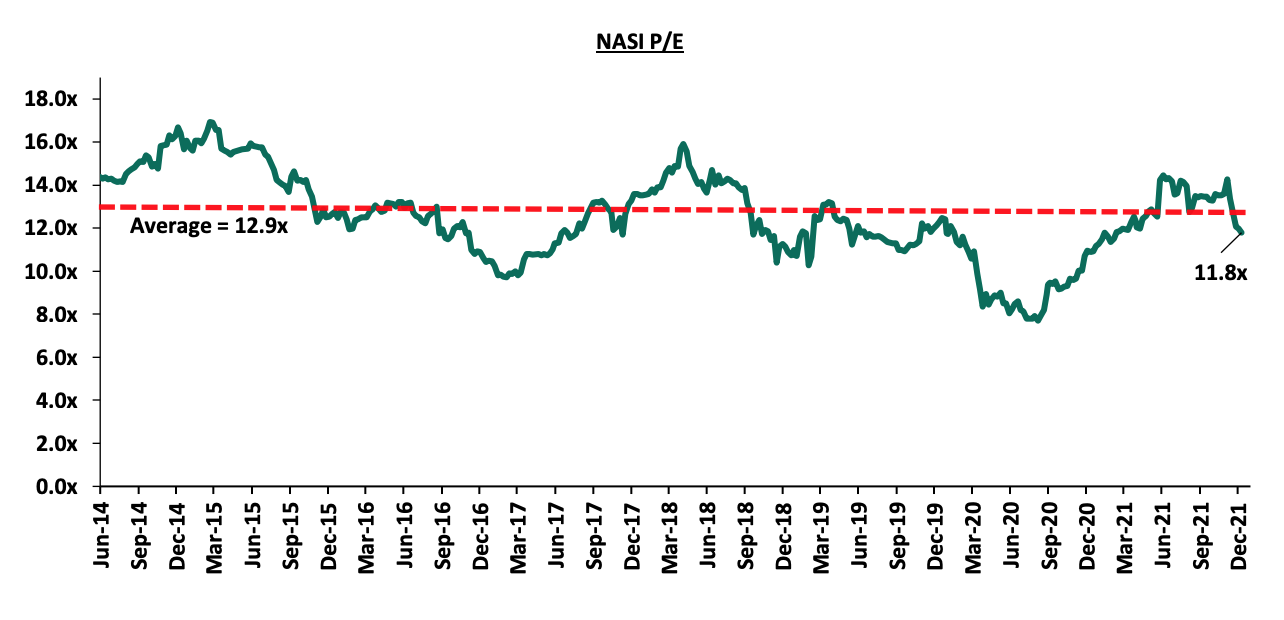

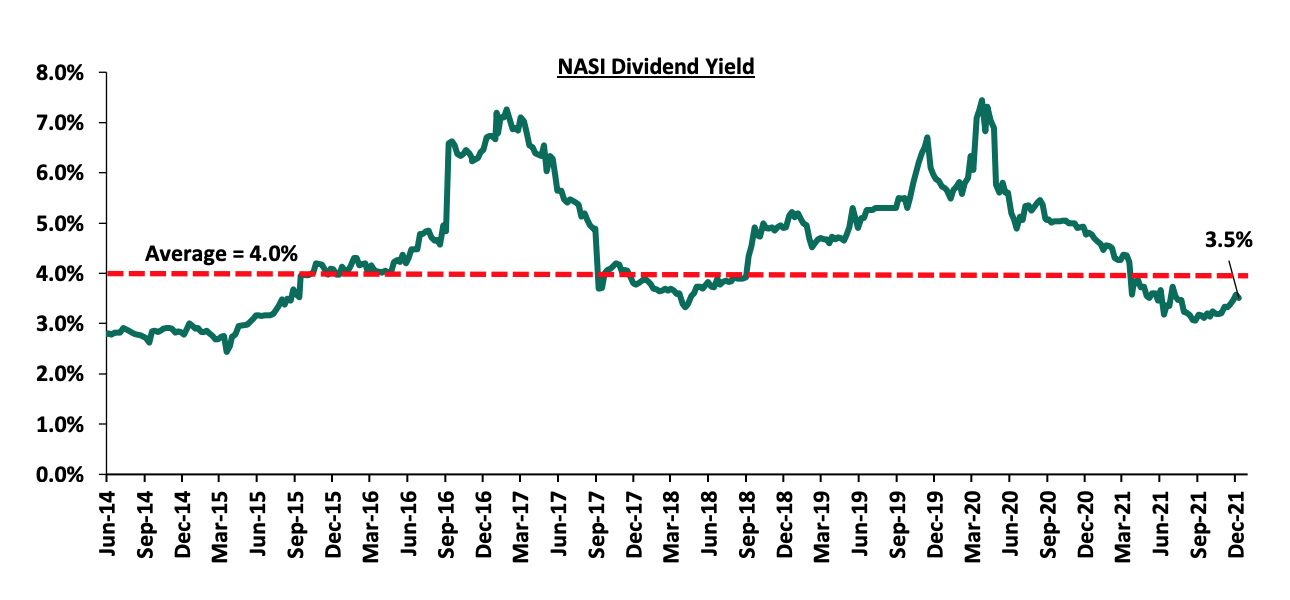

The market is currently trading at a price-to-earnings ratio (P/E) of 11.8x, 8.8% below the historical average of 12.9x, and a dividend yield of 3.5%, 0.5% points below the historical average of 4.0%.

Notably, this week’s P/E is the lowest it has been since February 2021. Key to note, NASI’s PEG ratio currently stands at 1.3x, an indication that the market is trading at a premium to its future earnings growth.

Basically, a PEG ratio greater than 1.0x indicates the market may be overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued.

The current P/E valuation of 11.8x is 53.1% above the most recent trough valuation of 7.7x experienced in the first week of August 2020. The charts below indicate the historical P/E and dividend yields of the market.