In its capacity as the government’s fiscal agent, the Central Bank of Kenya is in the debt market seeking an additional 15.0 billion shillings from the May bond; FXD1/2023/03.

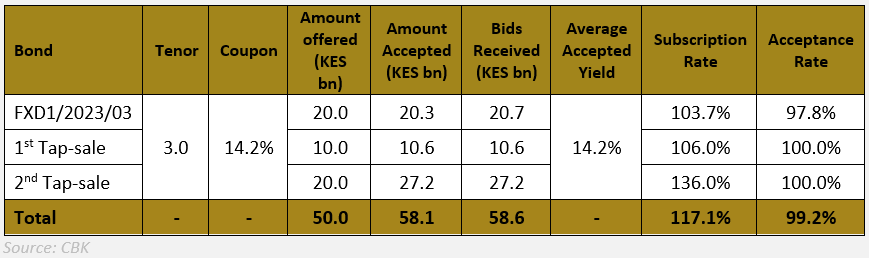

Notably, this is the third time the bond has been offered to investors as a tap-sale, following two prior issuances in May. In addition, the bond had been oversubscribed in all preceding offers, including the principal issuance.

The government has raised a total of 58.1 billion shillings against the 50.0 billion shillings promised.

The average yield on the bond is 14.228 percent, which is also the bond’s coupon rate. The band is available for sale until 23rd June 2023 or upon attainment of quantum, whichever comes first.

Related Content: Kenyan Hustlers If Taxed Per Month Can Raise Over Ksh 500B A Year To Finance The Housing Project

See below the performance of the bond in the previous issues;

Read More:

- Matatu Operators And Long Distance Drivers Issues Strike Notice, Here’s Why

- East African Cables Administration Stopped By The Court

- Kenyan Passport Ranked Position 98 In Global Rankings

The bond offers a higher return relative to its tenor and the repetitive issue in the tap-sale market highlights the government’s need for cash.

In addition, we suspect that the offer is intended to cover any excess expenditure in the FY’2022/2023 budget as it nears completion in June 2023.

Related Content: Comprehensive Analysis Of Taxation In Kenya: Burdens, Purpose, And Why Kenyans Need To Wake Up And Demand Better From Their Taxes

Key to note, the government needs an additional 39.6 billion shillings to meet the current domestic borrowing target of 425.1 billion shillings which we believe is attainable given that less than a month ago, the net domestic borrowing was at a yawning 49.3 percent less than the prorated target.

As interest rates climb, it is crucial to note that the bond offers investors who missed out on prior issues a chance to participate. Medium-term investors seeking good returns and a short-to-medium-term lock-in period should consider investing.

We expect an oversubscription on the sale despite the tightened liquidity. Investors will likely loosen up their cash reserves considering the good returns that the bond offers.

Related Content: The Chokehold Of Unfair Taxation: Strangling Kenya’s Businesses And Startups

This story is a statement sent from the Standard Investment Bank (SIB)