The savings rate within a nation is shaped by a rather complex interplay of economic, social, and policy factors.

Typically, developing economies aspire to achieve higher savings rates as a means of buffing up capital for vital investments in areas such as infrastructure, education, and overall economic advancement while advanced economies may have lower savings rates due to higher consumption levels.

Read Also: Dear Entrepreneur, Here Are 10 Money Habits Of The Rich

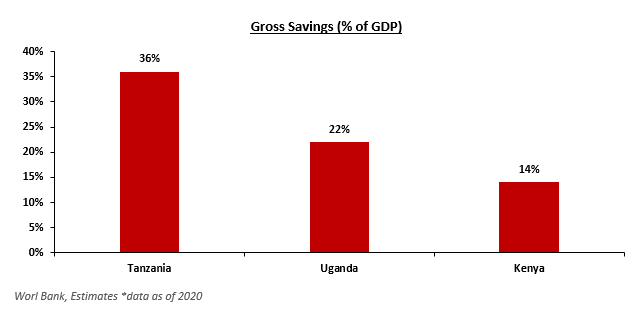

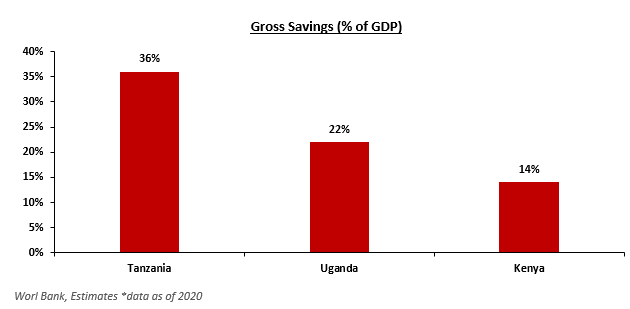

In the context of Kenya, we note that the country’s savings-to-GDP ratio has consistently trailed those of neighboring nations like Uganda and Tanzania for an extended period spanning over a decade as shown below:

In 2021, Kenya’s savings rate rose to 16% of GDP primarily due to the resumption of most economic activities and the reinstatement of most employees’ salaries following the COVID-19 slowdown – we note that pension contributions account for the larger part of the savings.

That said, we suspect that the lower ratio (as compared to the recommended ratio for lower-middle-income countries – 26%) is likely due to a higher rate of unemployment coupled with lower disposable income.

Read Also: Dear Entrepreneur, Become Successful By Dropping The Following Behavior

See below a chart comparing the rates of unemployment in the three countries;

Some of the factors affecting disposable income in Kenya include;

- Tax Policies – The level and structure of taxes, particularly income and consumption taxes such as VAT, can have a considerable impact on disposable income. Controversy specifically arises when taxation is concentrated on one group of the population e.g employees in the formal sector,

- Social Security & Pension Contributions – Mandatory contributions to social security, pension plans, and other similar programs such as the housing levy reduce disposable income, and

- Wages & Employment – Wage levels and employment opportunities influence the income earned by individuals. A lower minimum wage and a weak job market potentially reduce disposable income.

Read Also: Top 10 Business Opportunities For You In Eldoret

Below we look at the take-home salary and recurrent expenditures for two breadwinners; one earns KES 100,000 and the other earns KES 50,000.

Our assumptions are; i.) Both have 3 children, ii.) Both have no personal vehicles, iii.) Both work in the same area and iv.) Both contribute to a personal pension scheme.

Read Also: Dear Entrepreneur, Here Are Six Steps To Become A Millionaire By 30

We observe that the two individuals hardly meet their basic recurrent needs, let alone leisure and other one-off expenditures such as clothing. As a result of the squeezed pockets, many are forced to depend on loans from saccos, chamas, or digital apps such as Tala and Branch.

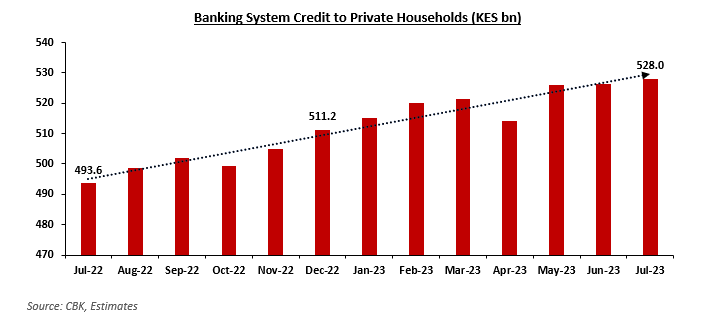

Consequently, the volume of loans disbursed to private households has been steadily increasing, as many individuals resort to borrowing from one lending app to settle obligations with another which has given rise to a cyclic pattern of indebtedness.

See below a chart showing the growth of credit advanced to private households since July 2023;

Read Also: 6 Strategies Employee Retention To Help Improve Your Business

It is worth noting that taxation policies and proposals for mandatory contributions continue to increase but the minimum wage and most employees’ salaries remain the same – with the real earnings adjusted to inflationary pressures dwindling over time.

As the government persists in raising the mandatory medical fund contributions to 2.75%, it is the employees in the formal sector who are most acutely affected. Furthermore, the National Social Security Fund (NSSF) contributions are slated to increase annually for the next four years, potentially placing additional strain on individuals’ financial resources.

Read More:

- The Devastating Impact of Delayed Payments: A Looming Threat to SMEs In Kenya

- Dear Entrepreneur, 10 Tips For Unlocking The Power Of Compounding To Become Rich

- Why Kenyans Should Start Saving The Little They Have While Young

This leaves formal sector employees with only two viable alternatives:

- Either accept a reduced standard of living, or

- Rely on loans for their survival.

Read Also: Six Pillars Of Entrepreneurial Success: Unveiling The Key Ingredients For Achievement And Success