Kenya Power is no longer just a story about a utility selling electricity to homes, shops, factories, and offices. The deeper story, as Standard Investment Bank’s valuation update makes clear, is that Kenya Power is being pushed into a new electricity age where the most valuable asset may not be the bill it sends to customers, but the grid it controls.

SIB has upgraded Kenya Power from HOLD to BUY and placed a fair value estimate of KES 25.57 per share on the company, against a market price of KES 15.50 at the time of the report. That implies a 65.0% upside. But this is not a blind celebration. It is a cautious vote of confidence in a business that has real assets, a national network, improving numbers, and a dangerous efficiency problem that can either unlock value or destroy it.

The reason this matters is simple. Kenya’s electricity market is opening up. The Energy (Electricity Market, Bulk Supply and Open Access) Regulations, 2026 are designed to dismantle the old single-buyer structure and create a more competitive, multi-supplier electricity market. In ordinary language, large consumers will increasingly be able to buy power from different suppliers, while Kenya Power’s network becomes the road through which that power travels.

Kenya Power may lose part of its historic monopoly over direct retail sales, especially among high-value commercial and industrial customers. But it can still win if it becomes the indispensable infrastructure landlord of the electricity economy: the company that owns and operates the wires, collects wheeling charges, keeps the network stable, and earns from every serious player that needs access to the national grid.

Read Also: Kenya Power Goes Digital For Electricity Connection Applications To Speed Up Service Delivery

The biggest enemy is not competition but leakage

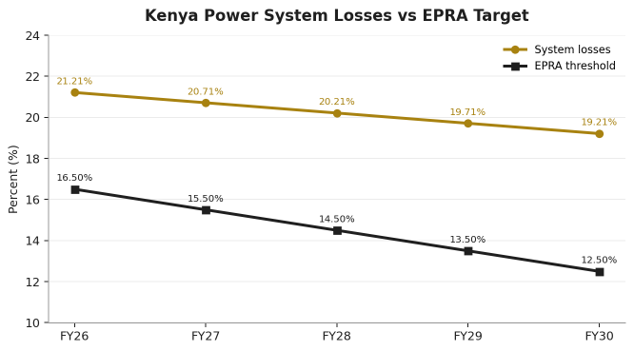

Competition will hurt Kenya Power if the company remains slow, inefficient, and dependent on tariff protection. But the most immediate enemy is not competition but leakage. SIB notes that system losses improved from 23.16% to 21.21%, but this is still far above the regulator’s target. The report frames the gap as a direct hit to earnings because losses above the allowable threshold cannot simply be passed to consumers through tariffs.

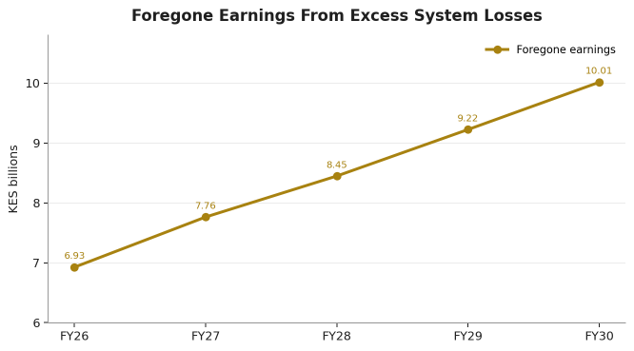

The numbers are brutal. SIB estimates that every one percentage point of system losses above the target costs costs Kenya Power about KES 1.5 billion in revenue. At the current inefficiency level, the company is leaking roughly KES 6.9 billion from annual earnings. This is why smart meters, feeder upgrades, energy accounting, replacement of faulty meters, and grid automation are not technical side issues. They are the core investment thesis.

A normal business loses money when customers refuse to pay. Kenya Power loses money even before some of that power becomes a bill. Every percentage point recovered is not just an engineering win; it is cash, margin, confidence, and valuation coming back into the company.

Source: SIB estimates. Annual system losses and EPRA thresholds from FY26 to FY30.

Source: SIB estimates. Values converted to KES billions from the report table.

The tariff review was withdrawn, but the message from the regulator is clear

Kenya Power’s tariff review, submitted on behalf of the sector, has been withdrawn. On the surface, this looks like a setback for a company that faces revenue shortfalls when actual electricity demand falls below the assumptions used to set tariffs. But SIB’s interpretation is more important: future tariff relief will likely be conditional.

The regulator is no longer likely to reward inefficiency with blanket tariff increases. Any tariff adjustment will require technical validation from EPRA, and the report suggests that relief will be linked to Kenya Power reducing system losses below the target loss factor and expanding or improving its network. In other words, the company cannot simply ask households and businesses to pay more while the grid continues to bleed value.

This is a healthier direction for the economy. Expensive power punishes factories, SMEs, schools, hospitals, cold rooms, salons, welders, millers and every household that depends on electricity to survive. If Kenya Power wants a stronger revenue base, it must earn it through efficiency, reliability and customer trust.

The hidden debt problem: why payables matter like borrowings

One of the sharpest parts of SIB’s valuation update is the treatment of trade payables as de facto debt. In a clean balance sheet, payables are a normal part of working capital. But when they age for too long, they start behaving like financing. They become a form of shadow debt because the company is effectively delaying payments to fund itself.

SIB therefore reclassifies the protracted payables as financial-liability equivalents in its DCF framework. This makes the valuation more conservative. It also explains the report’s headline: shadow debt erodes equity value. The market may see Kenya Power’s improving profitability, but the valuation must also ask a harder question: who is still waiting to be paid, for how long, and what does that do to the true enterprise value?

This is why the transfer of transmission assets to KETRACO matters. SIB argues that the transfer remains pivotal for balance sheet optimisation and compliance with the Energy Act, but progress appears stalled. The report suspects a pricing deadlock, with Kenya Power’s asset valuation likely above KETRACO’s acquisition threshold. Until that is resolved, the expected relief to finance costs and liquidity remains delayed.

The numbers: steady revenue, rising profit, better shareholder returns

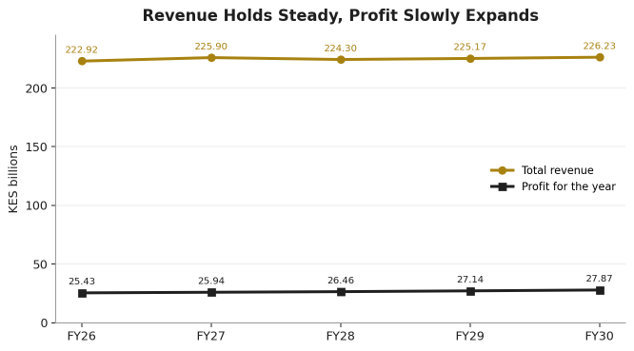

SIB’s earnings model is not built on a fantasy of explosive revenue growth. Revenue is projected to hover around KES 223 billion to KES 226 billion through FY30. The more interesting movement is in profitability, where profit for the year is forecast to rise from KES 25.4 billion in FY26 to KES 27.9 billion in FY30.

That is the heart of the story. Kenya Power does not need to become a glamorous growth company to create value. It needs to keep costs disciplined, reduce losses, ease financial pressure, clean up working capital, and turn its grid into a regulated revenue engine. If that happens, a slow revenue line can still produce a stronger profit line.

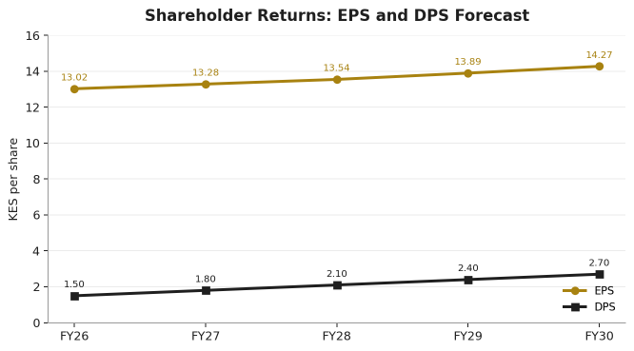

SIB also forecasts EPS moving from KES 13.02 in FY26 to KES 14.27 in FY30, while DPS rises from KES 1.50 to KES 2.70 over the same period. For shareholders, this suggests the investment story is not only about price upside; it is also about the possibility of a gradual return of income as the company repairs itself.

Source: SIB earnings model. Revenue and profit converted to KES billions.

Source: SIB earnings model. EPS and DPS are in Kenyan shillings per share.

A balance sheet trying to heal

The balance sheet story is also improving. SIB notes that Kenya Power has aggressively reduced its debt profile, helped by early repayment of high-interest loans. In the audited base year, borrowings fell from KES 98.5 billion in FY24 to KES 87.6 billion by June 2025, while the weighted average cost of debt eased from 5.03% to 3.84%. The report says lower interest expenses, down by KES 2.58 billion in the last cycle, are now supporting the bottom line.

Looking ahead, SIB’s forecast shows total equity rising from about KES 130.7 billion in FY26 to KES 216.1 billion by FY30. Total borrowings are projected to ease more gradually. The message is that Kenya Power’s recovery is possible, but it is not automatic. It depends on whether operational discipline can move faster than the risks around open access, captive power, receivables, aging payables and losses.

Source: SIB balance sheet forecasts. Borrowings combine current and non-current borrowings from the earnings model.

Read Also: Market Closes Lower as Major Indices Slip; Kenya Power Leads Turnover

What this means for ordinary Kenyans and businesses

This valuation update is not only for traders and institutional investors. It speaks directly to the cost of running an economy. When power is unreliable or expensive, every business suffers. A bakery pays more to bake bread. A welder loses customers when machines go off. A cold-room operator loses stock. A small hotel raises prices. A factory delays expansion. A household buys fewer tokens. A student studies in darkness. Power is not a luxury; it is the bloodstream of production.

That is why the open-access reforms must be understood carefully. If they work, they can attract private capital, deepen competition, improve price discovery, strengthen grid accountability and open the door to more efficient electricity supply. But if Kenya Power fails to modernise, the reforms can also expose its weaknesses. Big customers will look for cheaper and more reliable alternatives, while the company carries the weight of legacy obligations.

The best outcome for Kenya is not a weak Kenya Power. The best outcome is a disciplined Kenya Power: one that stops leaking power, pays suppliers on time, bills accurately, connects customers faster, gives industry reliable electricity and earns fairly from a grid that everyone needs.

SIB’s BUY call is therefore not a simple cheer for a cheap stock. It is a bet on transformation. Kenya Power has a national grid, a stronger earnings base, a possible infrastructure-landlord future and a valuation that still carries upside. But the company is also carrying the burden of system losses, receivables, delayed payables, stalled asset restructuring and a changing market that will no longer protect inefficiency forever.

The old Kenya Power survived by being unavoidable. The new Kenya Power must thrive by being useful. It must become the toll road of Kenya’s electricity future: reliable enough for private producers, affordable enough for industry, efficient enough for the regulator and transparent enough for investors.

If Kenya Power cleans the grid, repairs the balance sheet and turns open access into an infrastructure opportunity, the upside SIB sees can become more than a valuation line in a report. It can become a national productivity story. But if the company allows losses and shadow debt to continue eating value, then the same grid that gives it strategic importance will become the wire through which value leaks away.

Key data points from the SIB report

| Metric | FY26 | FY27 | FY28 | FY29/FY30 direction |

| System losses | 21.21% | 20.71% | 20.21% | Falls to 19.21% by FY30 |

| EPRA threshold | 16.50% | 15.50% | 14.50% | Tightens to 12.50% by FY30 |

| Foregone earnings | KES 6.93bn | KES 7.76bn | KES 8.45bn | Rises to KES 10.01bn by FY30 |

| Revenue | KES 222.9bn | KES 225.9bn | KES 224.3bn | KES 226.2bn by FY30 |

| Profit for year | KES 25.4bn | KES 25.9bn | KES 26.5bn | KES 27.9bn by FY30 |

| EPS | KES 13.02 | KES 13.28 | KES 13.54 | KES 14.27 by FY30 |

| DPS | KES 1.50 | KES 1.80 | KES 2.10 | KES 2.70 by FY30 |

Read Also: Kenya Power Boosts Interim Dividend by 50% After Strong Profit Growth