Money lenders can finally call the Kenya Revenue Authority “bro”. That is the funny way of describing one of the most important, and most misunderstood, changes in the Finance Act 2026. From 1 July 2026, the tax law expressly recognises that when a qualifying lender suffers a genuine bad debt, the loss may include the principal, the interest and other amounts connected to that debt. For years, the principal was the centre of a bitter tax war. Parliament has now written the answer into the law.

The reform sounds technical, but the issue is simple. Every loan has at least two parts. The first part is the principal: the lender’s own money advanced to the customer. The second part is the interest: the charge for allowing the customer to use that money. There may also be lawful fees or other amounts linked to the credit facility.

Imagine that a lender gives a customer KSh1 million and expects KSh100,000 in interest. The total amount due is KSh1.1 million. The customer stops paying, cannot be traced or has no recoverable assets. The lender follows the required recovery process, eventually concludes that the debt is genuinely irrecoverable and writes it off. The tax question is then unavoidable: what exactly has the lender lost for income-tax purposes? Is it only the KSh100,000 interest, or is it the full KSh1.1 million exposure?

For a long time, KRA’s strict position was that the principal was capital and therefore should not be deducted as a bad debt. In that view, only income items such as interest could qualify, subject to the law and the bad-debt guidelines. The lender could lose the money it advanced, but KRA could still treat the principal as a non-deductible capital loss.

Lenders argued that this did not reflect the economics of lending. A manufacturer trades in goods. A retailer trades in stock. A professional firm trades in services. A bank, microfinance institution or digital lender trades in money and credit. The principal advanced to customers is not a decorative asset sitting outside the business; it is the raw material from which the lending business earns income. When that principal disappears in a genuine default, the lender has suffered an ordinary business loss.

This disagreement mattered because income tax is charged on taxable profit, not on cash that has vanished. If a lender earned KSh500 million but permanently lost hundreds of millions of shillings in loans, refusing the principal deduction could leave the lender paying tax as though the missing money still existed. That could produce a tax bill detached from the lender’s real economic position.

Before the 2026 amendment, section 15(2)(a) of the Income Tax Act allowed a deduction for bad debts incurred in producing income where the Commissioner was satisfied that the debts had become bad. The Commissioner’s bad-debt guidelines, issued through Legal Notice No. 37 of 2011, then set out the circumstances in which a debt could be treated as uncollectable. But the guidelines also excluded capital expenditure, and that phrase became the fault line. KRA frequently treated the loan principal as capital. Lenders treated it as trading stock.

The Finance Act 2026 now says, in substance, that for a person carrying on a money-lending business, and for banks or financial institutions licensed under the Banking Act, the Microfinance Act or the Central Bank of Kenya Act, a bad debt includes the principal, the interest and any other amount relating to the debt. That is the decisive change. Parliament has removed the main argument KRA used to disallow the principal merely because it was principal.

This is not a casual favour to every person who has ever lent money. The provision operates within the Income Tax Act and the Commissioner’s guidelines. A taxpayer must be carrying on the relevant lending business and must show that the debt has actually become bad. A friendly loan to a cousin, a hidden shareholder withdrawal dressed up as a loan, an undocumented advance or a debt written off for convenience does not automatically become a tax deduction.

The word ‘bad’ is doing heavy legal work. A debt is not bad simply because the borrower is late, stubborn or temporarily short of cash. The 2011 guidelines require the creditor to take reasonable steps to collect it and to establish that it has become uncollectable. The debt may qualify where a court order extinguishes the creditor’s contractual right, the debtor is insolvent or bankrupt, there is no security that can be realised, the security has been realised but is insufficient, the cost of further recovery would exceed the amount likely to be recovered, or recovery has been abandoned for another objectively reasonable cause.

In practice, KRA will still expect evidence. That may include the loan agreement, disbursement records, repayment history, demand notices, telephone and email follow-ups, field-recovery reports, CRB information, searches for assets, security-realisation documents, court records, insolvency records, internal credit-committee approvals and the accounting entry that records the write-off. The amendment expands what can form part of the bad debt; it does not abolish the duty to prove that the debt is genuinely bad.

The Branch International dispute illustrates the size of the problem. In Branch International Limited v Commissioner of Domestic Taxes, the Tax Appeals Tribunal dealt with gross loan write-offs of about KSh902.4 million and net cash losses of about KSh796.7 million after recoveries. The Tribunal set aside the assessment relating to the disallowed cash loss, finding that Branch had placed ledger evidence before it that had not been effectively displaced. The case demonstrated how a single dispute over loan write-offs could place hundreds of millions of shillings of taxable income in contention.

Other decisions exposed the uncertainty. In Premier Credit Limited v Commissioner of Domestic Taxes, decided in February 2026, the Tribunal accepted the stricter view that loan principal was capital and therefore not deductible under the pre-amendment framework. When similar businesses can face materially different outcomes depending on how the court interprets principal, capital and trading stock, the tax system becomes unpredictable. The Finance Act has now replaced that uncertainty with an express statutory rule.

The reform should therefore be understood as a clarification of the tax base, not a government bailout of lenders. It gives qualifying lenders a deduction against taxable income. It does not require KRA to refund the entire unpaid loan. It does not transfer the borrower’s debt to the taxpayer. It does not create a public fund that quietly settles Tala, Branch, bank or microfinance balances.

A TAX DEDUCTION REDUCES TAXABLE PROFIT. IT DOES NOT REPLACE THE MONEY THE LENDER LOST.

| THE KSh1.1 MILLION EXAMPLE Principal advanced: KSh1,000,000 Interest due: KSh100,000 Potential qualifying bad debt: KSh1,100,000 | WHAT THE TAX EFFECT MAY LOOK LIKE At an illustrative 30% corporation-tax rate, a KSh1.1 million deduction could reduce tax by up to KSh330,000. The lender still carries roughly KSh770,000 of the loss before other accounting and tax effects. The precise result depends on taxable profits, prior recognition of interest, timing and the applicable tax rules. |

The arithmetic makes the point. If the full KSh1.1 million qualifies and the lender has sufficient taxable profits, a 30 per cent tax rate may produce a tax benefit of up to KSh330,000. KRA has not paid KSh1.1 million. The lender has merely avoided paying tax on income equal to a loss that the law now recognises. Even in the simplified example, the lender still absorbs about KSh770,000 before considering collection expenses, funding costs and other accounting effects.

The timing also matters. Interest may already have been recognised as income in an earlier period, or it may not have been recognised depending on the applicable accounting and tax treatment. The borrower may later make a payment after the loan has been written off. In that case, the recovery is not free money. A lender that previously claimed the bad-debt deduction will ordinarily have to recognise the recovered amount in the period of recovery under the applicable tax rules. Branch itself told the Tribunal that subsequent recoveries were recorded as income.

The biggest public misunderstanding is the belief that a tax write-off cancels the underlying loan. It does not. A write-off is an accounting and tax decision by the creditor. A waiver is a legal decision to release the debtor. They are not the same thing. Unless the lender expressly forgives the debt, settles it, loses the legal right through a court process, or the claim becomes unenforceable under the law, the borrower remains liable under the credit contract.

That means a borrower should not read the Finance Act and conclude, ‘KRA has carried my burden, so I no longer need to pay.’ The lender may continue lawful recovery efforts, may sell or assign the debt where the law permits, may report accurate negative credit information under the Credit Reference Bureau framework and may accept payment years after the accounting write-off. The tax treatment is between the lender and KRA. The repayment obligation is between the borrower and the lender.

There are, however, limits on how a lender may recover. The Digital Credit Providers Regulations, 2022 prohibit threats, violence, obscene language, shaming, unauthorised access to a customer’s contacts, messages to people in the customer’s phone book and other forms of harassment. A bad debt is not a licence to humiliate a borrower. The creditor may demand payment, but it must do so lawfully and with respect for privacy and dignity.

The same regulations also limit what a licensed digital credit provider may recover once a loan becomes non-performing. Broadly, the recoverable amount is capped by the principal outstanding when the loan became non-performing, contractual interest not exceeding that principal and reasonable expenses incurred in recovery. This reflects Kenya’s in duplum principle: interest should not grow without limit until a small loan becomes an impossible lifetime sentence.

The borrower should also understand limitation periods carefully. An action founded on contract is generally subject to a six-year limitation period under section 4 of the Limitation of Actions Act, but acknowledgements, part-payments, judgments, securities and the particular facts can change the analysis. It is therefore dangerous to assume that silence or the passage of a few years has automatically erased a debt. Only a proper review of the contract and the legal history can answer that question.

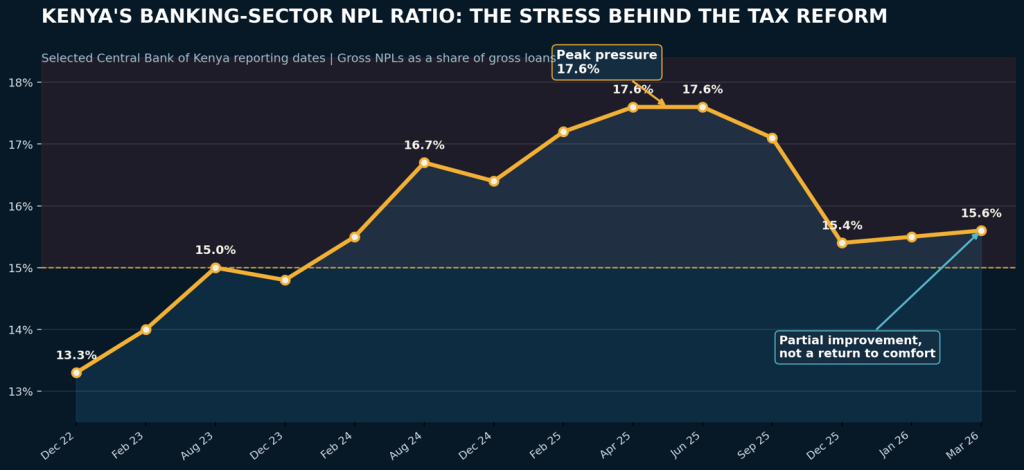

Why did this reform become so urgent? Because Kenya’s banking system has been carrying unusually high levels of non-performing loans. Central Bank of Kenya data show the gross NPL ratio rising from 13.3 per cent in December 2022 to 15.0 per cent in August 2023, 16.7 per cent in August 2024 and a peak of 17.6 per cent in April and June 2025. It improved to 15.4 per cent in December 2025, but stood at 15.6 per cent in March 2026. The direction has improved from the peak, but the system remains under severe pressure.

| 15.6% | OF GROSS BANK LOANS WERE NON-PERFORMING IN MARCH 2026 That was below the 17.6% peak recorded in 2025, but still high enough to show that Kenya’s credit stress is far from over. |

Source: Central Bank of Kenya Monetary Policy Committee releases, selected reporting dates. Latest official ratio identified for this report: March 2026.

Behind those percentages are households whose incomes have been squeezed, businesses whose cash flows have collapsed, employers dealing with delayed government payments, farmers exposed to weather and price shocks, and lenders trying to recover money in a weak economy. A high NPL ratio is not merely a banking statistic. It is a map of economic distress. It tells us that a large share of borrowers are struggling to turn income into repayment.

The tax amendment will help lenders report a more realistic taxable profit. It may also reduce the risk premium that lenders build into pricing when they fear that an unrecoverable principal will be denied for tax purposes. Greater certainty can improve provisioning, capital planning and the valuation of loan books. For digital lenders and microfinance institutions, whose portfolios contain many small unsecured loans, the change may be especially important because recovery costs can quickly exceed the value of an individual debt.

But no one should pretend that a tax deduction solves the NPL crisis. It cleans up the tax treatment after a loan has failed. It does not restore the borrower’s income, revive a closed business, reduce the cost of credit, improve government payment discipline or create jobs. Kenya still needs a stronger economy, better credit assessment, responsible lending, transparent pricing, early restructuring of distressed loans and effective insolvency processes.

The amendment also creates a new enforcement risk. Once principal, interest and related amounts are expressly deductible, some taxpayers may be tempted to label ordinary arrears as bad debts, accelerate write-offs, move connected-party advances into the loan book or claim unsupported recovery expenses as amounts related to the debt. KRA’s next battlefield will therefore not be whether principal is legally capable of deduction. It will be whether the specific debt was real, business-related, properly documented and genuinely irrecoverable.

The phrase ‘any other amount relating to the debt’ will require careful administration. It may cover legitimate charges directly connected to the credit facility, but it should not become a blank cheque for penalties, internal allocations or invented fees. Lenders will need clear accounting policies, consistent treatment across borrowers and an audit trail showing how every amount was calculated. KRA will need to enforce the rule without quietly recreating the same principal-versus-capital dispute that Parliament intended to end.

There is also a question of fairness between formal and informal credit. Regulated banks, microfinance institutions and licensed digital lenders are visible to KRA, CBK and the courts. Informal lenders often operate outside the same reporting, consumer-protection and tax systems. The reform should not encourage unlicensed lending or allow private arrangements to masquerade as commercial loan books. Tax relief must follow lawful business activity, not replace licensing and regulatory compliance.

For lenders, the message is clear: the Finance Act 2026 is a major victory, but the victory comes with paperwork. The principal can now be part of the bad-debt deduction, but only where the debt meets the statutory and administrative tests. A weak file will remain a weak claim. A board resolution saying ‘write it off’ cannot substitute for proof that reasonable recovery efforts were made and that continued pursuit was commercially pointless or legally impossible.

For borrowers, the message is even clearer: do not celebrate a tax write-off as debt forgiveness. KRA has not become your guarantor. Your loan agreement has not disappeared. Your CRB history may still be affected. Lawful recovery may continue. Where repayment has become impossible, the responsible response is to engage the lender early, seek restructuring, negotiate a settlement that is recorded in writing and obtain professional advice where the amount or consequences are serious.

For policymakers, the reform should be accompanied by stronger public education. Kenya has millions of borrowers who do not distinguish between a provision, a write-off, a waiver, a settlement and a limitation defence. That confusion creates false hope, predatory collection opportunities and needless disputes. Every lender should communicate clearly when a loan is written off for accounting purposes but remains legally due, and when it has actually been forgiven or settled.

The Finance Act has therefore ended one war but exposed a larger national problem. KRA and lenders may finally agree that a genuine bad debt can include the money advanced, the interest expected and related amounts. That is sensible tax policy. Yet the NPL graph shows that the victory arrives in an economy where too many people and businesses cannot repay in the first place.

So yes, money lenders can now call KRA ‘bro’. But the relationship has limits. KRA will recognise a properly proved loss; it will not reimburse the lender shilling for shilling. It will not cancel the borrower’s contract. It will not repair a broken credit market. The real test of the reform is whether it produces honest taxable profits, disciplined lending, lawful recovery and a clearer understanding of debt—without turning tax relief into either a loophole for lenders or a false escape route for defaulters.

Read Also: Why Wealth Belongs to Those Who Keep Investing When Life Gets Hard