There is a version of wealth that attracts attention: the new car, the expensive watch, the dramatic business launch, the sudden social-media announcement and the lifestyle that appears to have changed overnight. Then there is the version that actually lasts. It is quieter, slower and far less glamorous. It is built in private through patient ownership, disciplined investing, reinvestment, prudent risk-taking and the willingness to delay consumption.

Most people do not fail to build wealth because they lack intelligence. They fail because the process feels too slow. A small monthly investment does not look powerful in its first year. A modest parcel of land may sit unchanged for years. A young business can demand more money than it produces. Shares can move sideways. Skills can take years to become commercially valuable. During this stage, the builder sees effort while the outside world sees almost nothing.

That is the difficult truth about long-term wealth: the most important years often look unimpressive. The foundations are being laid, but the building has not yet risen above the fence.

|

The seduction of shortcuts

Shortcuts are attractive because they promise to remove time from the equation. They suggest that one trade, one deal, one connection, one speculative asset or one perfectly timed opportunity can replace years of patient accumulation. Occasionally, someone does get lucky. The mistake is turning an exceptional outcome into a general strategy.

Quick money and durable wealth are not the same thing. Quick money may come from timing, leverage or chance. Durable wealth requires systems: assets that retain or grow value, cash flows that can survive pressure, adequate liquidity, controlled debt, diversified sources of income and the discipline to protect capital after it has been created.

A shortcut asks, “How quickly can I multiply this money?” A wealth-building mindset asks, “How do I own something valuable, keep contributing to it, manage the risks, and allow it to compound for many years?” The second question sounds less exciting. It is also far more useful.

1. Patience Is an Economic Asset

Patience is often mistaken for inactivity. In investing, patience is active restraint. It is the decision not to interrupt a sound long-term plan simply because the results are not yet dramatic. It means continuing to save when nobody is applauding, continuing to learn when the skill has not yet paid, and continuing to own productive assets through seasons when headlines are frightening.

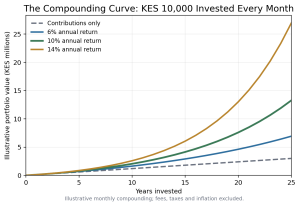

Compounding explains why time matters so much. Returns earned today can generate additional returns tomorrow. Contributions made early have more years to participate in that process. At first, the growth appears almost linear because the capital base is small. Later, the curve bends upward because returns are being earned not only on the original money, but also on accumulated gains.

The graph is a mathematical scenario, not a prediction. Higher returns generally involve higher risk and greater uncertainty.

In the illustration above, the investor contributes KES 10,000 every month. After 25 years, total personal contributions equal KES 3 million. Yet the projected final value can be much higher because time allows investment returns to accumulate on top of prior returns. The exact outcome will depend on the assets selected, fees, taxes, inflation, volatility and investor behaviour. The principle, however, remains: time can become a productive partner.

This is why consistency matters more than waiting for a “perfect” moment. Markets, businesses and economies rarely offer perfect clarity. The person who keeps postponing until every risk disappears may discover that the largest risk was the time they allowed to pass.

The cost of waiting is often invisible

Delay does not send an invoice. There is no monthly statement showing the compounding that never happened. That makes procrastination feel harmless. But every year postponed is a year in which capital could have been earning, learning, and expanding.

Figure 2: Starting age can matter as much as the monthly amount.

Illustrative KES 10,000 monthly investment to age 60 at a constant 10% annual return; real markets do not deliver constant returns.

The person who starts at 25 does not merely make ten more years of contributions than the person who starts at 35. Their earliest contributions also receive an additional decade to compound. The advantage becomes increasingly difficult to recover because the late starter is not only chasing missed deposits; they are chasing missed growth on those deposits.

This should not discourage anyone who is starting late. The best available starting point is still now. A late beginning can be strengthened through higher contributions, better earning capacity, lower fees, sensible risk-taking and a longer working or investing horizon. The lesson is not that late starters are doomed. It is that delay has a measurable cost, and action is usually more valuable than endless preparation.

2. Ownership Changes the Financial Equation

Income is essential, but income alone is not wealth. A salary, professional fee, or business payment supports life today. Ownership creates a value claim that can continue beyond the original work. That claim may take the form of shares, a business, intellectual property, income-producing property, equipment, a pension fund, a digital product or another productive asset.

The central shift in wealth creation is moving from merely earning money to using part of that money to acquire assets. This does not mean buying anything that can be called an investment. It means acquiring ownership in something with a credible ability to produce cash flow, appreciate, reduce future expenses, or strengthen earning power.

Consumption ends the transaction; ownership can continue it

When money is spent entirely on consumption, the benefit may be immediate but finite. When money acquires a productive asset, the transaction can continue generating value. A machine can improve output. A professional certification can expand income. Shares can represent ownership in profitable companies. A business system can serve customers repeatedly. Intellectual property can be licensed. Productive land can support housing, agriculture, logistics, or industry.

Ownership also changes how a person relates to economic growth. Consumers pay into the system. Owners hold claims on parts of the system. The long-term goal is not to stop consuming; it is to ensure that consumption does not absorb every shilling that could have been converted into an asset.

|

Not every asset is equally productive

Ownership must still be evaluated intelligently. Some assets generate income but grow slowly. Some appreciate but produce no cash flow. Some are liquid; others may take months to sell. Some protect against inflation; others are vulnerable to it. A business can create extraordinary value but may also fail. Land can preserve value in one location and remain stagnant in another. Shares can generate long-term growth while experiencing severe short-term declines.

The purpose of disciplined investing is therefore not simply to own more things. It is to assemble a resilient portfolio of assets whose risks, liquidity, cash flows and time horizons make sense together. Wealth is strongest when it is not dependent on one customer, one employer, one property, one stock, one political relationship or one source of income.

3. Reinvestment Is the Engine Room

Earning a return is only the first step. What happens to that return can determine whether capital merely survives or truly compounds. Dividends can be spent or reinvested. Business profits can fund lifestyle upgrades or strengthen inventory, technology, distribution and talent. Rental income can disappear into consumption or reduce debt and finance the next asset.

There is nothing wrong with enjoying the fruits of work. The danger comes when every early gain is harvested before the tree has developed deep roots. Many promising businesses and investment portfolios remain permanently small because the owner keeps removing the capital required for expansion.

Figure 3: Reinvesting returns allows the capital base to grow on itself.

The “returns withdrawn” scenario keeps the original capital and annual contributions but removes investment gains each year

The gap in the graph is not created by a higher contribution. It is created by what happens to the return. When gains remain invested, they become part of the capital base that earns future gains. When they are withdrawn, the investor receives income but sacrifices part of the compounding effect.

A practical wealth strategy can balance both needs. Early in the accumulation phase, a higher proportion of returns may be reinvested. Later, once assets are sufficiently large and diversified, part of the income can support living expenses without damaging the underlying capital. The objective is to avoid consuming the seed before it has produced a sustainable harvest.

4. Discipline Matters Most When the Story Becomes Uncomfortable

It is easy to believe in long-term investing during a rising market. Discipline is tested when prices fall, a business loses customers, inflation rises, an investment thesis is questioned, or a neighbour appears to be getting rich much faster through speculation.

Volatility creates two opposite dangers. The first is panic: selling a sound asset solely because its price has fallen. The second is denial: holding a fundamentally broken asset merely to avoid admitting a mistake. Discipline is not blind loyalty. It is the ability to distinguish temporary price movement from permanent deterioration in value.

A disciplined investor has rules before emotions become intense. They understand the purpose of the investment, the expected holding period, the acceptable level of loss, the conditions that would invalidate the thesis, and the amount of liquidity needed outside the portfolio. These rules do not eliminate risk, but they reduce the chance that fear or greed will make every decision.

Figure 4: Behaviour can create a lasting gap even when investors begin with the same amount.

Hypothetical annual returns are deliberately volatile. The illustration compares continued investing with a permanent exit to 3% cash after the first major decline.

The disciplined investor in the illustration does not avoid losses. Their portfolio falls in difficult years. What changes the long-term outcome is that they continue contributing and remain exposed to subsequent recoveries. The panic investor protects themselves from future declines, but also removes themselves from future growth. In real life, moving to cash can sometimes be prudent; the problem is making a permanent decision from a temporary moment of fear.

5. Wealth Is Built by Systems, Not Motivation

Motivation is unreliable. It rises after a powerful speech, a financial scare, or a new goal, then fades when ordinary life returns. Systems are more dependable. They turn wealth-building from an occasional act of enthusiasm into a default behaviour.

| SYSTEM | WHY IT MATTERS |

| Pay yourself first | Move a defined amount into savings or investments immediately after income arrives, before discretionary spending expands. |

| Automate contributions | Use standing orders or scheduled transfers so investing does not depend on monthly willpower. |

| Maintain an emergency reserve | Keep sufficient liquid funds so a short-term crisis does not force the sale of long-term assets at the wrong time. |

| Review, do not obsess | Evaluate performance and allocation periodically, but avoid reacting to every daily price movement or rumour. |

| Increase contributions with income | When earnings rise, direct part of the increase toward assets before lifestyle costs absorb the entire improvement. |

| Protect against concentration | Diversify across assets, sectors, customers and income sources where practical. |

A good system should be realistic enough to survive difficult months. An aggressive plan that collapses after three pay cycles is weaker than a moderate plan maintained for ten years. The objective is not to impress anyone with the size of one contribution. It is to build a repeatable process that can continue through school fees, business pressure, family responsibilities, market declines and changing income.

6. The Human Side of Wealth: Sacrifice Without Losing Your Life

Financial advice can become cold when it treats people as spreadsheets. Real life contains children, parents, illness, unemployment, generosity, grief, celebration and responsibilities that cannot always be optimised. Building wealth should not require a person to become emotionally absent or permanently afraid to spend.

Discipline is not punishment. Delayed gratification does not mean delayed living. It means choosing deliberately: enjoying what matters, resisting what merely performs status, and refusing to trade long-term freedom for short-term applause. A sustainable wealth plan includes room for dignity, rest, relationships and giving. It simply refuses to let every desire become an emergency purchase.

The deepest purpose of wealth is not display. It is agency. It is the ability to survive a shock, educate a child, care for family, leave a harmful situation, fund an idea, employ others, support a cause, retire with dignity and make decisions from conviction rather than desperation.

|

7. A Practical Framework for Building Durable Wealth

- Know your cash flow: Track what comes in, what goes out, and which expenses are quietly consuming your investable surplus.

- Build a safety layer: Establish emergency liquidity and appropriate insurance before taking risks that could force distress sales.

- Eliminate destructive debt: Prioritise expensive consumer debt whose interest compounds against you.

- Invest in earning power: Develop skills, tools, networks and credentials that can expand future income.

- Acquire productive assets: Direct a consistent share of income toward diversified assets aligned with your horizon and risk capacity.

- Reinvest strategically: Allow dividends, profits and other returns to strengthen the capital base, especially during accumulation years.

- Review the thesis: Assess whether each asset still serves its purpose; change course when evidence changes, not merely when emotions change.

- Protect the structure: Use diversification, legal documentation, succession planning, tax compliance, and risk controls to preserve what you build.

The Final Truth: Wealth Is a Long Conversation With Time

Long-term wealth is rarely built by one spectacular decision. It is built by hundreds of ordinary decisions that point in the same direction. The decision to save before spending. To buy an asset instead of another symbol of success. To reinvest when consumption would feel better. To continue learning. To avoid reckless debt. To remain calm during volatility. To protect capital. To begin again after mistakes.

The process can feel unfairly slow in the beginning. That is because the first stage depends heavily on your labour and discipline. You are carrying the structure. But with enough time, quality ownership and consistent reinvestment, the balance can begin to change. Assets produce income. Returns produce returns. Systems reduce dependence on willpower. Capital starts carrying part of the weight.

This is why patience is not weakness, ownership is not greed, and disciplined investing is not deprivation. Together, they form the quiet architecture of financial freedom.

Ignore the pressure to look successful before your financial foundation is ready. Build privately. Invest consistently. Own productive assets. Reinvest intelligently. Manage risk. Give time permission to work. Shortcuts may create a dramatic story, but durable wealth is usually built by people who were willing to keep making sound decisions long after the excitement disappeared.

|

Graph Methodology and Important Notice

The graphs in this article are scenario models created to explain financial principles. They are not forecasts, guarantees, recommendations to buy a particular asset, or representations of historical market performance. Actual investment outcomes vary and may include loss of capital.

| FIGURE | CORE ASSUMPTION | WHAT IS EXCLUDED |

| Figure 1 | KES 10,000 monthly for 25 years; constant 6%, 10% or 14% annual return, compounded monthly. | Inflation, taxes, fees, missed contributions, variable returns and losses. |

| Figure 2 | KES 10,000 monthly from ages 25, 35 or 45 to age 60 at a constant 10% annual return. | Changing income, retirement withdrawals, fees, inflation, and market variability. |

| Figure 3 | KES 1 million initial capital plus KES 120,000 yearly at 10%; compares reinvested versus withdrawn gains. | Taxes, fees, variable returns, and the value of income already withdrawn. |

| Figure 4 | KES 500,000 initial capital plus KES 120,000 yearly through a hypothetical volatile return sequence. | Real security selection, transaction costs, taxes, and alternative re-entry decisions. |

Before making a material financial decision, consider your goals, income stability, obligations, time horizon, liquidity needs and capacity to absorb losses. Where appropriate, obtain advice from a licensed financial adviser, tax professional or other qualified specialist.

Read Also: Dear Entrepreneur, Is It True That Higher Return Equals Higher Risk?