Market Review: 2016 in Focus And Projections for 2017

The year 2016 was characterized by uneven global economic growth, with the US and China economies proving resilient with expected growth of 2.2 percent and 6.9 percent, respectively in the year while the United Kingdom and the Eurozone recorded reduced economic growth at 1.6 percent and 2.1 percent for the year, respectively according to a report released by Cytonn Investments.

The sluggish start of the year coupled with the Brexit led to increased uncertainty facing the global growth leading to the International Monetary Fund (IMF) reducing the world projected growth in their October issue by 0.1 percent to 3.1 percent from an earlier projection of 3.2 percent at the start of the 2016. Economic growth was largely supported by accommodative Central Banks policies in the advanced economies.

Growth in emerging markets, in particular the South-East Asian regions, is proving resilient owing to recent stability in commodity prices, leading to the region contributing 1.8percent to overall 3.1 percent global GDP growth, a higher contribution than advanced economies contribution of 1.6 percent.

In terms of trade, the World Trade Organization (WTO) downgraded their outlook for world trade growth in 2016 to 1.7 percent from 2.8 percent in April 2016, citing a slowdown in China and falling import levels in the United States.

This was the first time in 15 years that international commerce is seen to lag GDP growth of the world economy, having grown 1.5x faster than GDP over the 35-year period from 1981 to 2016, and 2.0x faster since globalization picked up in the 1990s.

There is increased anti-globalization campaign aimed at preserving the various local economies but from the past it is clear that open markets are good in helping both developed and developing countries attain maximum productivity leading to high GDP growth and increased job creation and hence economic prosperity.

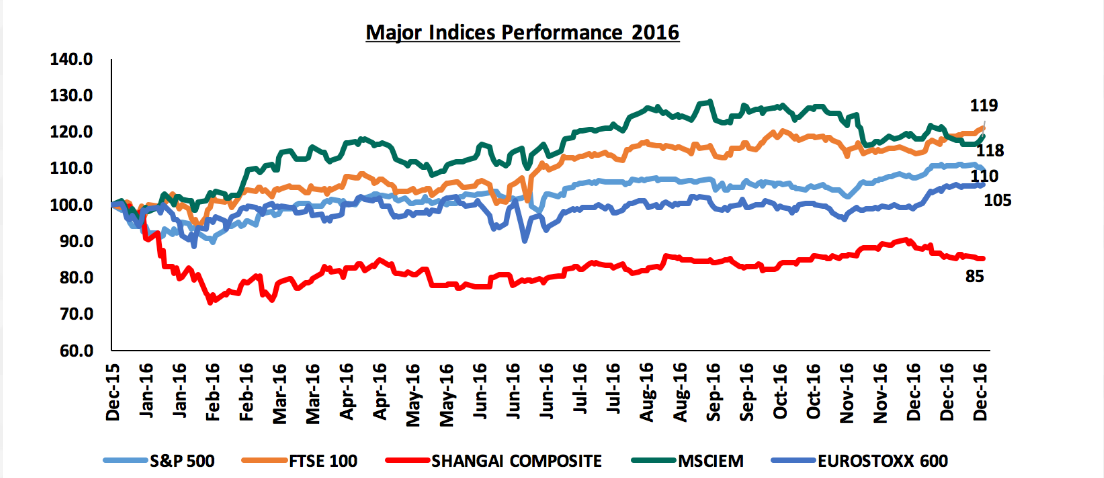

Global equity markets registered mixed performance, with investor sentiment mixed throughout the year on the back of a slowdown in China and Central Banks’ policy divergence as the Fed raised rates and the European Central Bank extended its quantitative easing program.

The S&P 500 index performed better than other global indices, rising 9.9 percent, followed by the MSCI emerging markets index that rose 8.1 percent. The Shanghai Composite was the worst performer having declined by 12.3 percent. The strong performance of the US stock was driven by the positive economic growth better than expectations, recording an annualized growth rate of 3.5 percent for period ending September 2016 while Shanghai composite loss was attributed to negative investor sentiment due to rising levels of debt towards the end of the year.

About Juma

Juma is an enthusiastic journalist who believes that journalism has power to change the world either negatively or positively depending on how one uses it.(020) 528 0222 or Email: info@sokodirectory.com