Maisha Microfinance Bank Seeks Ksh 1 Billion Capital Injection

Maisha Microfinance Bank is seeking for 1 billion shillings that will be used as a capital injection that will cushion it from the new accounting system.

According to a statement from the lender, the new capital will be set aside for “anticipating risky loans” as well as investing in technology and funding growth in the business.

Microfinance businesses in Kenya are currently facing stiff competition from digital lenders who have taken up a big number of Kenyans in search of instant loans.

“The Bank requires adequate capital to roll out an expansive portfolio of innovative and customer-led products and services. To this end, the Bank initiated a standard regulatory procedure with the intent to recapitalize the bank,” said Mr. Iraneus Gichana, the CEO of the financial institution.

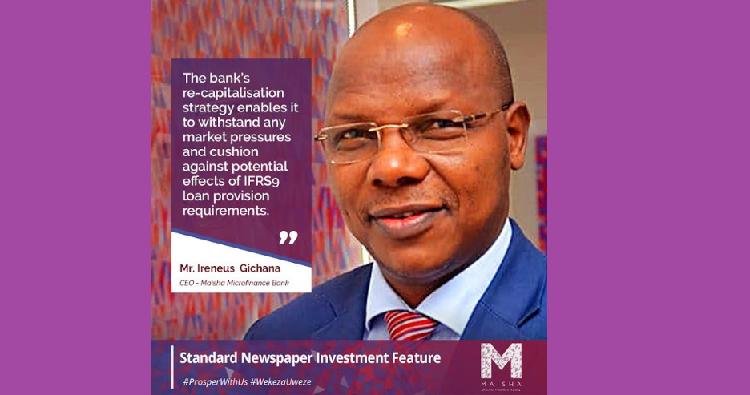

The lender plans to recapitalize in a strategy that will enable it to withstand any market pressures and “cushion against potential effects of IFRS9 loan provision requirements.”

“The Bank has been in operation for less than three years. During this infancy period, Maisha Microfinance Bank focused on laying the foundation for future growth prospects. All the bank’s existing shareholders have supported the bank continually with the injection of additional capital. With this capital, the bank will be able to build a resilient business model capable of addressing the huge demand for financial services. The Bank’s re-capitalization strategy enables it to withstand any market pressures and cushion against potential effects of IFRS9 loan provision requirements,” added Mr. Gichana.

According to the 2006 Microfinance Act section 19 (1), “No person shall hold, directly or indirectly or otherwise have a beneficial interest in, more than twenty-five percent of the shares of an institution.”

The Act further provides in section 19 (3b) for “exemption by the Treasury Cabinet Secretary on the recommendation of the Central Bank of Kenya,” to exceed the 25% single shareholder threshold for a specific period

Once the exemption request is received and evaluated by Central Bank, it is then submitted to Treasury, for consideration and approval by the Cabinet Secretary. If granted, the institution is expected to have in place a divestiture plan within a specific period to ensure the single shareholder limits are observed back to a maximum of 25 percent.

Maisha Microfinance Bank sought an approval to allow one of its shareholders, KAMU Limited, to hold in excess of 25 percent of the Bank’s issued share capital.

After a rigorous review process, the Cabinet Secretary for the National Treasury considered and granted approval to the bank’s request for exemption from the provisions of section 19(1) of the Microfinance Act. This allows Kamu Limited to hold in excess of 25 percent of Maisha Microfinance Bank’s issued share capital for the period specified in the Gazette notice.

The exemption granted is for a period not exceeding four years with effect from March 1, 2019. Details of this exemption are contained in Kenya Gazette Supplement No. 41 dated April 5, 2019.

This is a major milestone for the bank as it enables it to pursue its growth strategies. This is neither a buy-out nor a sale transaction; it is merely an injection of additional capital to support the bank’s growth strategies.

Kamu Limited is one of the CBK-approved shareholders of Maisha Microfinance Bank. KAMU is a strategic investment vehicle, which over the years has diversified its investment portfolio. It is owned by the Kangwana family which has investments in the financial, insurance, hospitality, and real estate sectors.

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory