How Standard Investment Bank Earned Its Place Beside Family Bank At The Gates Of The NSE

The story begins far from the ceremony of a stock-exchange listing. It began in 1995, in a modest office at Rehani House on Koinange Street, where Standard Stocks Limited opened its doors with five employees and a conviction that a Kenyan-owned financial institution could compete through discipline, relationships, and trust. There was no grand headquarters, no billion-shilling fund and no long list of landmark transactions. There was only a small team trying to earn the confidence of one client at a time.

James Wangunyu, the firm’s founder, had come into the venture carrying lessons from commercial banking: how to read a balance sheet, structure credit, measure risk and remain patient when money and ambition pull in opposite directions. Those lessons became part of SIB’s institutional character. The firm would move quickly, but it would not treat finance as theatre. It understood that behind every transaction stood people whose savings, companies, jobs and legacies were being placed in professional hands.

By 2000, the young brokerage had risen to the top of Kenya’s stockbroking market by trading volume. That early achievement mattered because it established a pattern that would define SIB’s development: begin with a narrow capability, master it, build trust around it and then expand without abandoning the discipline that created the first success.

The 2003 investment-banking licence transformed the firm from a successful broker into a broader capital-markets institution. The establishment of its Corporate Finance desk followed, giving SIB the capacity to sit with boards, founders, shareholders and management teams before a transaction reached the public eye. This is where the quiet work of investment banking happens: the valuation models that must withstand challenge, the capital structures that must remain viable after the headlines, the disclosures that must be accurate, and the competing interests that must be aligned without damaging the institution at the centre of the deal.

Family Bank encountered that competence long before the current listing. In 2014, SIB served as a Joint Lead Transaction Advisor on a private rights issue valued at approximately KES 3.1 billion. Family Bank’s own annual report recorded a 100 per cent uptake that brought in about KES 3 billion of additional capital and helped lift shareholders’ funds by 78 per cent, from KES 5.97 billion to KES 10.62 billion. That capital was not an abstract figure. It expanded the bank’s ability to lend, strengthened its regulatory position and increased the size of the businesses it could support.

The significance of that shared history is easy to miss. SIB is not approaching Family Bank as a stranger learning the institution during a compressed transaction timetable. It has previously helped the bank value itself, speak to shareholders, structure a capital raise and convert confidence into balance-sheet strength. It has seen Family Bank not only as an issuer, but as a living institution with customers, employees, ambitions and obligations. Twelve years later, the assignment is different, but the underlying responsibility is familiar: help the bank move into its next stage without losing the substance that brought it this far.

“SIB is not approaching Family Bank as a stranger. It has already helped the bank convert shareholder confidence into balance-sheet strength.”

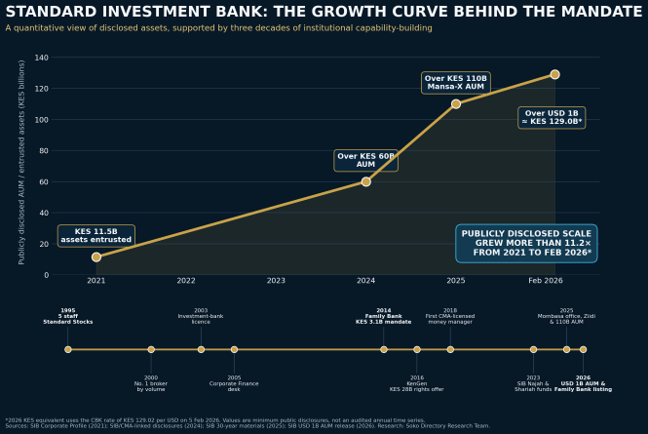

Figure 1: SIB’s growth is visible in both the scale of assets entrusted to it and the steady widening of its institutional capabilities. Public disclosures are used because SIB is privately held and does not publish a continuous annual revenue series.

The growth curve above is important because competence is not proved by age alone. A firm can exist for decades and remain unchanged. SIB’s story is different: its years have been converted into capability. By 2007, its equities desk was trading more than KES 20 billion. In 2016, it advised on KenGen’s approximately KES 28 billion rights offer, one of the largest and most demanding equity-capital transactions undertaken in the Kenyan market. That assignment required the same qualities Family Bank now needs—regulatory fluency, detailed coordination, credible valuation work, shareholder communication and the discipline to car