The story begins far from the ceremony of a stock-exchange listing. It began in 1995, in a modest office at Rehani House on Koinange Street, where Standard Stocks Limited opened its doors with five employees and a conviction that a Kenyan-owned financial institution could compete through discipline, relationships, and trust. There was no grand headquarters, no billion-shilling fund and no long list of landmark transactions. There was only a small team trying to earn the confidence of one client at a time.

James Wangunyu, the firm’s founder, had come into the venture carrying lessons from commercial banking: how to read a balance sheet, structure credit, measure risk and remain patient when money and ambition pull in opposite directions. Those lessons became part of SIB’s institutional character. The firm would move quickly, but it would not treat finance as theatre. It understood that behind every transaction stood people whose savings, companies, jobs and legacies were being placed in professional hands.

By 2000, the young brokerage had risen to the top of Kenya’s stockbroking market by trading volume. That early achievement mattered because it established a pattern that would define SIB’s development: begin with a narrow capability, master it, build trust around it and then expand without abandoning the discipline that created the first success.

The 2003 investment-banking licence transformed the firm from a successful broker into a broader capital-markets institution. The establishment of its Corporate Finance desk followed, giving SIB the capacity to sit with boards, founders, shareholders and management teams before a transaction reached the public eye. This is where the quiet work of investment banking happens: the valuation models that must withstand challenge, the capital structures that must remain viable after the headlines, the disclosures that must be accurate, and the competing interests that must be aligned without damaging the institution at the centre of the deal.

Family Bank encountered that competence long before the current listing. In 2014, SIB served as a Joint Lead Transaction Advisor on a private rights issue valued at approximately KES 3.1 billion. Family Bank’s own annual report recorded a 100 per cent uptake that brought in about KES 3 billion of additional capital and helped lift shareholders’ funds by 78 per cent, from KES 5.97 billion to KES 10.62 billion. That capital was not an abstract figure. It expanded the bank’s ability to lend, strengthened its regulatory position and increased the size of the businesses it could support.

The significance of that shared history is easy to miss. SIB is not approaching Family Bank as a stranger learning the institution during a compressed transaction timetable. It has previously helped the bank value itself, speak to shareholders, structure a capital raise and convert confidence into balance-sheet strength. It has seen Family Bank not only as an issuer, but as a living institution with customers, employees, ambitions and obligations. Twelve years later, the assignment is different, but the underlying responsibility is familiar: help the bank move into its next stage without losing the substance that brought it this far.

“SIB is not approaching Family Bank as a stranger. It has already helped the bank convert shareholder confidence into balance-sheet strength.”

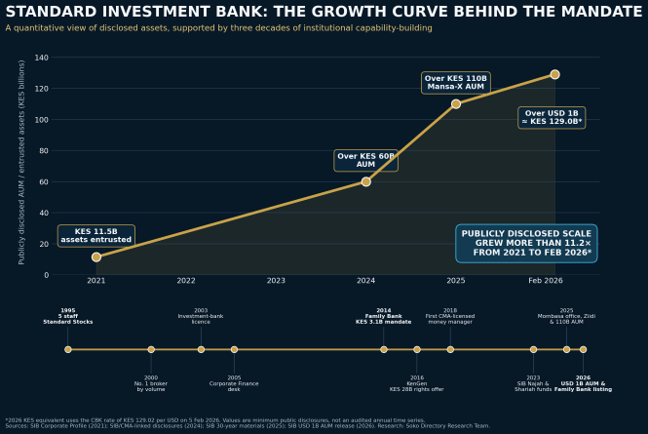

Figure 1: SIB’s growth is visible in both the scale of assets entrusted to it and the steady widening of its institutional capabilities. Public disclosures are used because SIB is privately held and does not publish a continuous annual revenue series.

The growth curve above is important because competence is not proved by age alone. A firm can exist for decades and remain unchanged. SIB’s story is different: its years have been converted into capability. By 2007, its equities desk was trading more than KES 20 billion. In 2016, it advised on KenGen’s approximately KES 28 billion rights offer, one of the largest and most demanding equity-capital transactions undertaken in the Kenyan market. That assignment required the same qualities Family Bank now needs—regulatory fluency, detailed coordination, credible valuation work, shareholder communication and the discipline to carry a transaction across the finish line.

In 2018, SIB became the first institution licensed by the Capital Markets Authority as an online foreign-exchange money manager in Kenya, opening a new chapter through Mansa-X. The move revealed another part of SIB’s substance: it was not content to survive on the reputation of old transactions. It was prepared to build new investment products, enter unfamiliar regulatory territory and create pathways through which Kenyan investors could reach global assets.

That product line expanded rather than stagnated. A United States dollar fund was introduced for diaspora investors and clients with dollar income. SIB Najah and Shariah-compliant Mansa-X funds followed in 2023, extending investment access to clients whose faith and ethical requirements had often been treated as an afterthought by conventional finance. In 2024, SIB secured a Retirement Benefits Authority licence and became fund manager for the Taifa Pension Fund. In 2025, it partnered with Safaricom as a fund manager for Ziidi, opened its first regional office in Mombasa and broke ground on a 32-storey international centre intended to house its next generation of trading, advisory and wealth-management operations.

The numbers followed the widening capability. SIB’s 2021 corporate profile disclosed approximately KES 11.5 billion in assets entrusted to the institution. By late 2024, the firm was reporting assets under management above KES 60 billion. Its 30-year materials placed Mansa-X assets above KES 110 billion in 2025, while a February 2026 announcement said the Mansa-X Special Funds had crossed USD 1 billion in assets under management. Using the Central Bank of Kenya’s exchange rate of KES 129.02 to the dollar on 5 February 2026, that threshold was equivalent to more than KES 129 billion. These are not simply larger numbers. They are repeated votes of confidence from investors who can withdraw their money if the institution fails to justify their trust.

By the time Family Bank prepared to enter the Main Investment Market Segment of the Nairobi Securities Exchange, SIB had therefore become more than a transaction shop. It had developed securities trading, fixed income, research, global markets, asset management, Islamic investment banking, pension-fund management and corporate finance within one institution. Its campaign brief records more than 60 corporate-finance mandates with an aggregate value above KES 270 billion, including public offers, rights issues, restructurings, privatisations, valuations, acquisitions and debt-capital-market assignments.

That breadth explains why SIB is the right partner for Family Bank’s Listing by Introduction. The transaction is not an IPO and it is not raising fresh money on the listing date. It is taking up to 1,662,654,760 existing ordinary shares into public trading on the NSE at an introduction price of KES 18 per share. The achievement lies in creating liquidity, public price discovery, stronger visibility and a platform from which the bank may pursue future capital-market opportunities.

A Listing by Introduction can look simple from the outside because there is no public subscription form and no dramatic countdown to a capital-raising target. Inside the process, however, the work is exacting. Shareholder approvals, regulatory reviews, legal documentation, reporting-accountant work, share dematerialisation, disclosure standards, valuation context, investor education and market readiness must all move in the right sequence. A weakness in one workstream can delay or damage the whole transaction.

The Transaction Advisor must therefore do more than complete a checklist. It must understand how regulators think, how investors read risk, how boards make decisions and how the market may interpret every number placed in the public domain. It must know when to move quickly and when precision is more valuable than speed. It must be able to challenge the issuer without losing the issuer’s trust. SIB has earned that judgement through repeated exposure to complex transactions, not through slogans.

Its position beside Family Bank also carries symbolic weight for Kenya’s capital markets. Both institutions are homegrown. Both began as smaller Kenyan enterprises competing in fields where scale and legacy could easily have excluded them. Both expanded by building relationships beyond Nairobi’s traditional corporate elite. Family Bank grew from a building society into a national commercial bank; SIB grew from a five-person brokerage into an investment house managing billions and advising some of the region’s most consequential institutions.

Their reunion at the NSE is therefore not accidental. In 2014, SIB helped Family Bank ask its existing owners to provide the capital needed for growth. In 2026, it is helping those owners bring their shares into a transparent public market where value can be tested through trading. The first assignment strengthened the bank from within. The current assignment opens the bank outward—to analysts, institutions, pension funds, retail investors and the daily judgement of the market.

This is where SIB’s relationship-first culture becomes commercially important. A transaction advisor may leave after a listing, but the consequences remain with the issuer for years. SIB’s own corporate profile says its growth has been strategic and intentional because it makes relationships a priority. The Family Bank relationship demonstrates that philosophy in practice: the firm that helped on a capital raise during one phase of the bank’s life has been trusted to advise its entry into the public market during another.

SIB has earned its place because it has repeatedly done the work that institutions only entrust to advisors when the stakes are high. It has raised capital, valued businesses, restructured balance sheets, supported listings, participated in privatisations and built investment products under evolving regulation. It has also shown the capacity to reinvent itself: from stockbroker to investment bank, from local equities to global multi-asset management, from conventional products to Shariah-compliant solutions, and from a Nairobi office to a wider national footprint.

None of this means the Family Bank listing is free of risk or that SIB’s involvement guarantees a particular market price. Capital markets do not offer certainty; they offer a disciplined arena in which information, confidence and competing expectations meet. The value of a capable advisor is not that it can control the market. It is that it can ensure the issuer arrives before that market prepared, accurately presented and structurally ready for scrutiny.

When Family Bank’s shares begin trading, the cameras will focus on the bell, the board and the first price. The more important achievement will be less visible: years of preparation condensed into a functioning public security. Behind it will stand the legal documents, regulatory engagements, valuation decisions, shareholder work and market coordination that allowed a privately traded bank to become a listed institution.

SIB will have earned its place in that moment long before the opening bell. It earned it in the five-person office where reputation was the only meaningful capital. It earned it when it became Kenya’s leading broker by volume, when it accepted the higher obligations of an investment-bank licence, when it built a corporate-finance practice, when it helped Family Bank raise capital, when it carried the KenGen rights offer, when it pioneered a regulated money-management model and when tens of thousands of investors entrusted it with their wealth.

The substance of Standard Investment Bank is therefore not found in one transaction. It is found in the accumulation of judgement. It is the ability to remain local without thinking small, to innovate without abandoning controls, and to treat a client relationship as something that may outlive the immediate deal. Family Bank needs that combination precisely as it steps into the visibility and discipline of the NSE.

This is not simply a bank choosing an advisor. It is one Kenyan growth story recognising another—and trusting it to help carry the next chapter.

Read Also: How SIB Guided Family Bank’s Decade-Long Turnaround To The NSE