How SIB Guided Family Bank’s Decade-Long Turnaround To The NSE

On 23 June 2026, Family Bank is scheduled to cross one of the most consequential thresholds in its four-decade history. Up to 1,662,654,760 ordinary shares will be admitted to the Main Investment Market Segment of the Nairobi Securities Exchange at an introduction price of KES 18 per share, placing an opening reference value of about KES 29.9 billion on the lender. The moment deserves precision: this is not an initial public offering and no fresh capital is being raised through the listing itself. It is a Listing by Introduction, a transaction that takes shares already in existence and moves them into a regulated, visible and continuously tradable public market.

That distinction does not make the transaction less important. It makes its purpose clearer. For years, Family Bank’s shares have changed hands away from the main exchange, where finding a buyer, agreeing a price and completing a transfer could be slower and less transparent. Once the shares begin trading on the NSE, existing shareholders gain a recognised route to liquidity, prospective investors gain a more accessible entry point, and the bank gains something that every serious institution eventually needs: a public mechanism through which the market can express, day after day, what it believes the business is worth.

At the centre of that transition is Standard Investment Bank Limited, the Transaction Advisor. SIB’s task is not ceremonial and it is not simply to escort Family Bank to the bell-ringing moment. A listing by introduction requires the careful alignment of shareholder approvals, regulatory requirements, valuation work, disclosures, legal documentation, reporting-accountant inputs, share dematerialisation, market-readiness processes and communication to investors. The transaction advisor is the institution that keeps those moving parts attached to one timetable and one standard of accountability.

That is why SIB’s appointment matters. Family Bank is placing a defining corporate transition in the hands of an investment bank with more than three decades in Kenya’s capital markets and a corporate-finance record spanning more than 60 mandates valued at over KES 270 billion. SIB has worked on transactions that helped build the architecture of the market itself, including the KenGen rights issue, the Kenya Re public offer, the Nairobi Securities Exchange’s demutualisation and listing, Kenya Power’s balance-sheet restructuring and the privatisation of KWAL Holdings. These are not merely names on a credentials page. They represent experience in coordinating regulators, boards, shareholders, lawyers, accountants, brokers and investors when the cost of error is measured in both money and institutional trust.

The relationship with Family Bank also has history. In 2014, SIB served as a Joint Lead Transaction Advisor on Family Bank’s KES 3.1 billion private rights issue, helping the lender value the business and raise growth capital from shareholders. Twelve years later, SIB is again alongside the bank, but the assignment has evolved. The earlier mandate helped strengthen the balance sheet; the current one helps establish a public market for the ownership of that balance sheet. It is a progression from raising capital inside a relatively closed shareholder structure to opening the bank’s value to wider scrutiny, liquidity and price discovery.

Read Also: Family Bank’s Profits Up 55.4% For The Year 2025

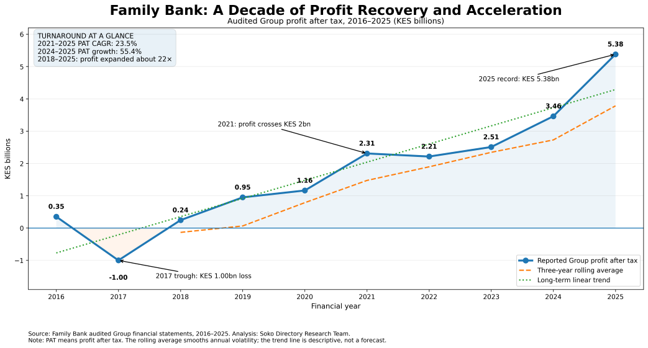

Family Bank does not arrive at this point as a speculative promise. It arrives carrying the evidence of a difficult but increasingly convincing financial recovery. In 2016, the Group reported KES 352 million in profit after tax. A year later it fell into a KES 1.00 billion loss, a trough that could have defined the institution had management failed to rebuild earnings, strengthen controls and restore confidence. Instead, profit returned to KES 244 million in 2018, rose to KES 950 million in 2019 and reached KES 1.16 billion in 2020. The decisive break came in 2021, when Group profit after tax moved above KES 2.3 billion.

The line is not perfectly smooth, and that is precisely why it is credible. Profit softened slightly to KES 2.21 billion in 2022 before recovering to KES 2.51 billion in 2023, climbing to KES 3.46 billion in 2024 and then accelerating to KES 5.38 billion in 2025. Between 2021 and 2025, Group profit after tax grew at a compound annual rate of about 23.5 per cent. The 2025 result alone was approximately 55 per cent above the previous year. Measured from the fragile recovery recorded in 2018, annual profit expanded about twenty-two times by 2025.

Behind those earnings is an institution with the scale to belong on the NSE’s main market. By the end of 2025, Family Bank had total assets of KES 208.7 billion, shareholders’ funds of KES 32.6 billion, more than 1.3 million customers and 96 branches spread across 32 counties. The bank’s 2025 private placement also raised KES 8 billion against a KES 6.09 billion target, an outcome that indicates substantial shareholder appetite before the shares reached the public exchange. The first quarter of 2026 added further momentum, with total assets rising to KES 230.2 billion, customer deposits reaching KES 168.9 billion and profit after tax growing to KES 1.65 billion.

These numbers do not eliminate risk, nor should a serious market article pretend that they do. Banking remains exposed to credit quality, interest-rate movements, regulation, capital requirements, competition and the health of the wider economy. A strong historical profit curve is not a guarantee of future returns. What the record does provide is a stronger basis for valuation. Investors will not be asked to price only an ambition; they will be able to examine a bank that has survived a loss-making period, rebuilt profitability, expanded its capital base and entered the market with a clearer growth strategy.

The announced KES 18 introduction price is therefore best understood as the opening reference point, not the final word on Family Bank’s value. Once trading begins, price will be shaped by the interaction of buyers and sellers, the quality and consistency of future earnings, dividend expectations, asset quality, governance, liquidity, market sentiment and confidence in management. That public contest of opinions is one of the market’s most useful disciplines. It does not produce an infallible ‘true price’, but it creates a more observable market-clearing price than an illiquid over-the-counter environment can ordinarily provide.

This is where the listing can attract a wider class of investors without promising them easy gains. Pension funds, asset managers, family offices, institutions and retail investors will have a quoted security they can analyse, buy or sell through established market infrastructure. Analysts will be able to compare Family Bank more directly with listed peers. Existing shareholders will no longer depend on a private search for counterparties when they need liquidity. Management, meanwhile, will operate under the sharper cadence of public disclosures, investor questions and continuous market judgement.

For Family Bank, this public visibility can become strategic capital even though no cash is raised on listing day. A liquid quoted share can strengthen future options: subsequent capital raising, strategic acquisitions, employee ownership programmes, institutional partnerships and more efficient shareholder transitions. The listing creates a platform from which the bank may approach future transactions with a market price already in existence and an investor community already familiar with its performance.

For SIB, the mandate is a statement about continuity and competence. The investment bank that previously helped Family Bank raise KES 3.1 billion is now helping it convert years of private value creation into public-market visibility. SIB’s wider record shows why it was selected: it understands not only how to raise money, but also how to structure the institutional journey around money — the valuation, documentation, regulation, stakeholder coordination and market narrative that determine whether a transaction earns confidence.

The significance extends beyond the two institutions. Kenya’s capital market has long needed more profitable, operating companies to widen investor choice and deepen trading. A bank with a national footprint, a broad SME and retail franchise, a decade-long earnings story and a sizeable shareholder base adds a different source of activity to the exchange. It also sends a message to other family-owned and privately held businesses: the public market is not merely an exit door. Properly used, it is an infrastructure for succession, liquidity, governance, visibility and long-term corporate life.

Family Bank is therefore a fitting candidate for this transition, not because every year has been easy, but because the decade reveals the institution’s capacity to recover. The fall into loss in 2017 makes the KES 5.38 billion profit of 2025 more meaningful. The value of the story is not a straight ascent; it is the proof that the bank could absorb pressure, regain its footing and build a stronger earnings engine. Markets often reward growth, but they also study resilience, and Family Bank is bringing both to the exchange for judgement.

When the shares start trading, the ceremony will last a morning. The consequences will last much longer. Family Bank will begin a new relationship with transparency, investors and price. Existing owners will see their holdings translated into a visible market value. New investors will decide whether the bank’s earnings, strategy and risks justify that value. SIB will have completed the delicate work of moving an established institution through the gates of a regulated public market.

Family Bank is not arriving at the NSE to become valuable. It is arriving so that the value built through customers, branches, capital, technology, recovery and profit can be seen, debated and exchanged. Standard Investment Bank’s role is to ensure that the bridge between private promise and public price is crossed with competence. That is why this listing matters: it turns a decade of reinvention into a market instrument, gives shareholders a clearer route to liquidity, and allows Kenya’s investing public to place its own price on the future of one of the country’s most consequential tier-two banks.

Read Also: Family Bank Posts Robust First Quarter Growth as Profit Hits KES 1.6 Billion Ahead of NSE Listing

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (279)

- August 2026 (58)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)