Kenya’s Money Market Is Calm, But The Real Economy Is Coughing

Standard Investment Bank’s latest fixed income report tells a story of two Kenyas. In the financial markets, the surface looks fairly calm: overnight money is priced steadily, the shilling is holding up against major global currencies, and investors are still buying short-term Treasury Bills. But underneath that calm, the real economy is under pressure. Inflation has jumped, household budgets are being squeezed, and private-sector activity has slipped deeper into contraction territory.

For ordinary readers, the report matters because fixed income is not just a market story. It affects the cost of government borrowing, the rates banks use to price loans, the returns savers receive on Treasury Bills and bonds, and the pressure that eventually lands on households through taxes, prices, and reduced private-sector activity.

Money market: liquidity cooled, but the price of overnight money did not move

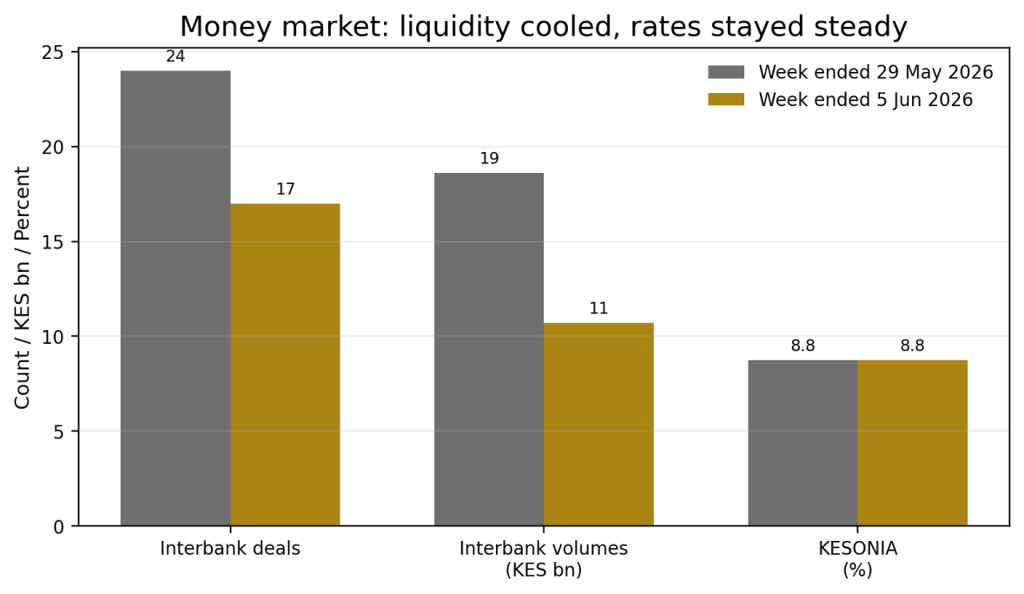

Liquidity conditions remained stable during the week. The Kenya Shilling Overnight Interbank Average, commonly referred to as KESONIA, closed at an average of 8.75%. That stability is important because KESONIA is a practical signal of how much banks are paying when they lend money to each other overnight. When it is stable and close to the Central Bank Rate, it suggests monetary policy is being transmitted cleanly through the banking system.

The bigger change was in volumes. Interbank lending fell by 42.35%, from KES 18.60 billion to KES 10.72 billion. The number of deals also dropped from 24 to 17, a 29.17% decline. In simple terms, banks were still lending to one another at the same average rate, but they were doing less of it. That points to a quieter money market rather than a panic-driven one.

Read Also: Money Market Funds Are Not Investments — CMA Should Classify Them As Saving Products

Figure 1: Interbank activity fell sharply, while KESONIA remained unchanged at 8.75%.

Treasury Bills: investors rushed to the 91-day paper

The Treasury Bill auction was fully covered, with investors submitting KES 54.58 billion in bids. The fiscal agent accepted KES 54.55 billion, giving the auction an almost complete subscription rate and a strong overall performance rate of 227.42%.

The standout instrument was the 91-day Treasury Bill. It received KES 32.83 billion in bids against only KES 4.00 billion on offer, giving it a performance rate of 820.68%. That kind of demand says something clear: in an uncertain environment, many investors prefer short-term paper. They want to earn a return, but they also want to avoid locking money for too long when inflation, interest rates and government borrowing needs are still shifting.

The accepted yields were tightly clustered: 8.56% for the 91-day, 8.53% for the 182-day and 8.76% for the 364-day. With inflation at 6.7%, SIB estimates real returns of 1.9%, 1.8% and 2.1% respectively. The returns are positive, but not wide enough to make investors relaxed about inflation.

Figure 2: The 91-day T-Bill was massively oversubscribed, signalling a strong preference for short-dated government paper.

Treasury Bonds: demand remained weak, and the government accepted almost everything

The bond market gave a very different signal from the T-Bill market. Ahead of the 2026/27 budget reading, the June Treasury Bond auction for FXD1/2020/015 and FXD1/2018/025 fell short of the KES 40 billion target. Total bids came in at KES 34.4 billion and the Treasury accepted almost the entire amount.

That 86% subscription rate shows that demand was weaker than the government wanted. The 99% acceptance rate also suggests the Treasury had to be flexible enough to take what the market offered. For readers, this matters because when the government needs money and investors are cautious, yields tend to face upward pressure. Higher government yields can eventually pull up borrowing cos