PayPal’s Africa Problem Is No Longer A Support Issue. It Is A Strategic Deliberate Failure To Frustrate African Entrepreneurs

PayPal has spent more than two decades selling the world a simple promise: money should move safely, quickly and fairly across borders. That promise helped build one of the most recognisable names in digital finance. It also helped PayPal process about $1.79 trillion in total payment volume in 2025, serve 439 million active accounts across roughly 200 markets, and remain a default rail for online work, e-commerce, donations, digital services and creator income. Yet for many African users, especially in markets such as Kenya, the PayPal experience too often feels like a two-tier system: trusted enough to receive African value, strict enough to lock African users out of their own money, and slow enough in customer resolution to make global finance feel like a gated club rather than a public utility.

The latest anger in Kenya should therefore not be dismissed as ordinary platform friction. Reports that PayPal froze funds, blocked accounts and demanded work contracts and proof of residence from Kenyan users under anti-money-laundering checks strike at the heart of a larger question: does PayPal apply risk controls with equal fairness, transparency and urgency across all markets, or does it treat African customers as permanently suspicious by default? No serious person argues that PayPal should ignore fraud, sanctions, money laundering, identity theft or consumer protection. Compliance is not optional in payments. But compliance without proportionality becomes punishment. Risk management without clear communication becomes institutional arrogance. A platform that can take a customer’s money instantly but cannot explain, review and resolve a restriction quickly has failed the basic test of financial dignity.

PayPal must show equal treatment to all its customers, not as a slogan, but as an operating standard. If a user in Nairobi, Lagos, Accra, Kigali, Johannesburg or Addis Ababa is asked to provide documents, the process must be as clear, timely and appealable as it is for a user in London, New York, Berlin or Toronto. If funds are held, PayPal must state the reason in plain language, specify what evidence is required, provide a human escalation path, give realistic resolution timelines, and publish market-level transparency data showing how many accounts were limited, why they were limited, how long reviews took, and how many decisions were reversed. The company cannot keep hiding behind generic compliance language while users lose school fees, supplier payments, rent, wages, freelance income and business working capital.

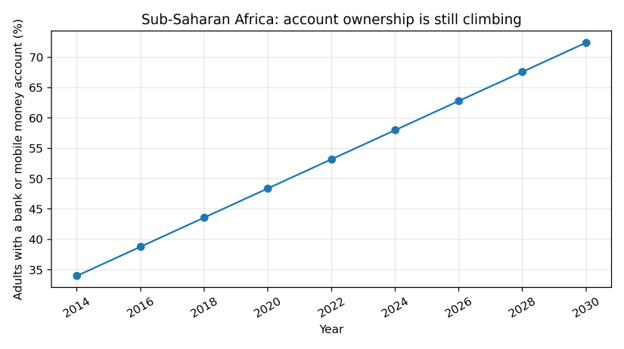

The issue is sharper because Africa is not a marginal payments story. It is one of the most important payments laboratories on earth. Sub-Saharan Africa is the global centre of mobile money. GSMA reported that mobile money accounted for $2 trillion in global transactions in 2025, while Sub-Saharan Africa represented about two-thirds of global mobile-money transaction value, meaning roughly $1.3 trillion to $1.4 trillion moved through mobile-money rails in the region. AfricaNenda’s SIIPS 2025 work shows that African instant payment systems processed about 64 billion transactions worth nearly $2 trillion in 2024, rising from about $775.5 billion in 2020. World Bank Global Findex-linked analysis shows account ownership in Sub-Saharan Africa rose from 34 per cent of adults in 2014 to 58 per cent in 2024, and mobile money accounts reached around 40 per cent of adults. Mastercard-commissioned research has projected Africa’s digital payments economy at about $1.5 trillion by 2030. This is not a continent waiting to be taught payments. This is a continent already doing payments at scale, in real time, under difficult infrastructure conditions, and often with more creativity than the markets that lecture it.

Chart 1: World Bank/AfricaNenda-reported account-ownership trend, with a simple linear opportunity scenario to 2030. The point is not prediction; it is direction. Africa’s formal and mobile-enabled financial base is still expanding.