PayPal has spent more than two decades selling the world a simple promise: money should move safely, quickly and fairly across borders. That promise helped build one of the most recognisable names in digital finance. It also helped PayPal process about $1.79 trillion in total payment volume in 2025, serve 439 million active accounts across roughly 200 markets, and remain a default rail for online work, e-commerce, donations, digital services and creator income. Yet for many African users, especially in markets such as Kenya, the PayPal experience too often feels like a two-tier system: trusted enough to receive African value, strict enough to lock African users out of their own money, and slow enough in customer resolution to make global finance feel like a gated club rather than a public utility.

The latest anger in Kenya should therefore not be dismissed as ordinary platform friction. Reports that PayPal froze funds, blocked accounts and demanded work contracts and proof of residence from Kenyan users under anti-money-laundering checks strike at the heart of a larger question: does PayPal apply risk controls with equal fairness, transparency and urgency across all markets, or does it treat African customers as permanently suspicious by default? No serious person argues that PayPal should ignore fraud, sanctions, money laundering, identity theft or consumer protection. Compliance is not optional in payments. But compliance without proportionality becomes punishment. Risk management without clear communication becomes institutional arrogance. A platform that can take a customer’s money instantly but cannot explain, review and resolve a restriction quickly has failed the basic test of financial dignity.

PayPal must show equal treatment to all its customers, not as a slogan, but as an operating standard. If a user in Nairobi, Lagos, Accra, Kigali, Johannesburg or Addis Ababa is asked to provide documents, the process must be as clear, timely and appealable as it is for a user in London, New York, Berlin or Toronto. If funds are held, PayPal must state the reason in plain language, specify what evidence is required, provide a human escalation path, give realistic resolution timelines, and publish market-level transparency data showing how many accounts were limited, why they were limited, how long reviews took, and how many decisions were reversed. The company cannot keep hiding behind generic compliance language while users lose school fees, supplier payments, rent, wages, freelance income and business working capital.

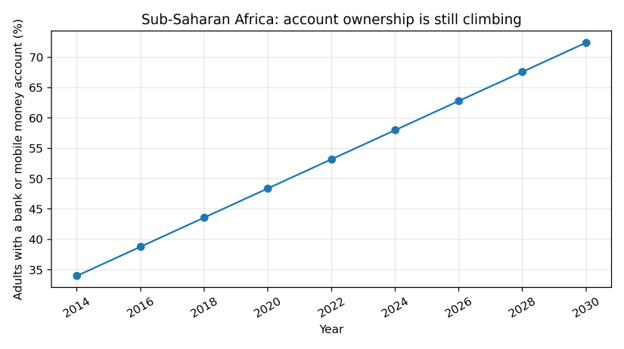

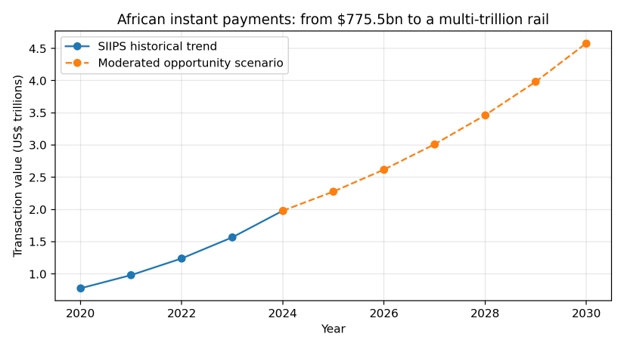

The issue is sharper because Africa is not a marginal payments story. It is one of the most important payments laboratories on earth. Sub-Saharan Africa is the global centre of mobile money. GSMA reported that mobile money accounted for $2 trillion in global transactions in 2025, while Sub-Saharan Africa represented about two-thirds of global mobile-money transaction value, meaning roughly $1.3 trillion to $1.4 trillion moved through mobile-money rails in the region. AfricaNenda’s SIIPS 2025 work shows that African instant payment systems processed about 64 billion transactions worth nearly $2 trillion in 2024, rising from about $775.5 billion in 2020. World Bank Global Findex-linked analysis shows account ownership in Sub-Saharan Africa rose from 34 per cent of adults in 2014 to 58 per cent in 2024, and mobile money accounts reached around 40 per cent of adults. Mastercard-commissioned research has projected Africa’s digital payments economy at about $1.5 trillion by 2030. This is not a continent waiting to be taught payments. This is a continent already doing payments at scale, in real time, under difficult infrastructure conditions, and often with more creativity than the markets that lecture it.

Chart 1: World Bank/AfricaNenda-reported account-ownership trend, with a simple linear opportunity scenario to 2030. The point is not prediction; it is direction. Africa’s formal and mobile-enabled financial base is still expanding.

That is why PayPal’s African posture is so strategically confused. The company appears to see African markets as useful enough for transaction flows, remittances, merchant activity and digital labour, but not important enough for first-class customer experience. PayPal’s own Kenya pages market the ability to receive money, manage funds and transfer balances. That creates a legitimate expectation. A Kenyan freelancer who designs logos for a German client, a Ugandan developer maintaining code for a US start-up, a Nigerian creator receiving subscription income, or a South African merchant selling digital goods is not asking for charity. They are asking for the same predictability that PayPal’s brand implies elsewhere. The product cannot be global in marketing and colonial in treatment.

Enrique Lores, PayPal’s new president and chief executive from March 1, 2026, has inherited a company with scale, brand recognition and deep infrastructure, but also a trust deficit in markets where trust is everything. His appointment came after PayPal’s board replaced Alex Chriss, signalling that the pace of change and execution was not meeting expectations. That matters because Africa should be one of the places where Lores proves PayPal can still reinvent itself. He should not begin his tenure by treating the continent as a compliance nuisance. He should make Africa a test of whether PayPal can become a fairer, faster and more transparent network. A new chief executive who wants to be taken seriously should order a public review of account limitations in African markets, publish customer-protection metrics, invest in localised support, create verified business tiers for freelancers and SMEs, and build integrations that respect mobile money as infrastructure rather than treating it as an exotic afterthought.

The challenge to Lores is simple: do not merely optimise PayPal for Wall Street; repair it for the workers, merchants and creators whose small transactions compound into the company’s global relevance. In 2025, PayPal’s transaction volume was larger than the GDP of most countries. That scale gives it power, and power requires discipline. A payments company cannot be judged only by the volume it processes when things go right. It must be judged by how it behaves when it suspects something has gone wrong. Does it investigate quickly? Does it communicate clearly? Does it respect the customer? Does it avoid collective suspicion? Does it separate fraudsters from legitimate users? Does it give people a route back into the system? These are not soft questions. They are the core governance questions of the platform economy.

The African technology community should also stop waiting for foreign platforms to become benevolent. PayPal’s failures should be read as a product brief. Africa needs a better alternative for cross-border digital work, merchant checkout, creator monetisation, diaspora remittances, subscriptions, escrow, dispute resolution and instant settlement into local wallets and bank accounts. It should support multiple currencies, stable-value settlement where legally permitted, strong identity verification, transparent risk scoring, fast appeals, open APIs, low fees, and interoperability with mobile money, banks, card schemes, PAPSS, national instant payment systems and regional settlement rails. It should be built with compliance from day one, not as a slogan but as a competitive advantage. The winning African alternative will not be the one that ignores regulation. It will be the one that makes compliance humane, legible and fast.

Chart 2: AfricaNenda SIIPS 2025 says African instant payment values rose from $775.5bn in 2020 to about $1.98tn in 2024. The dotted line is a moderated scenario, not a formal forecast, showing how quickly the addressable payments rail could compound even if growth slows.

The African Development Bank should be challenged directly here. AfDB has supported digital financial inclusion through the Africa Digital Financial Inclusion Facility, and that work is important. But the continent now needs more than pilots, conferences, policy papers and donor-friendly language. It needs patient capital for payment infrastructure, pan-African risk-sharing, compliance utilities, identity rails, merchant-verification systems, fraud-data collaboration, cybersecurity capacity, and a serious fund for African-owned cross-border payment networks. If AfDB can speak about mobilising capital for roads, power, climate and industrialisation, it should speak just as boldly about payment sovereignty. Money movement is economic infrastructure. If African exporters cannot receive small payments reliably, if digital workers cannot access earnings predictably, if creators are trapped by foreign platforms, and if SMEs cannot trade across borders without punitive friction, then the promise of AfCFTA remains partly rhetorical.

AfDB should convene central banks, PAPSS, AfricaNenda, telecom operators, commercial banks, fintechs, diaspora organisations and development partners around a practical objective: make it possible for an African business to receive, hold, dispute, convert and settle legitimate cross-border digital payments with the same confidence that a business in Europe or North America expects. That objective requires regulation, but also architecture. It requires consumer protection, but also speed. It requires anti-money-laundering discipline, but also an end to lazy derisking that treats entire countries as suspect. The bank should not only finance infrastructure after it exists. It should help create the conditions for African infrastructure to win.

Elon Musk also belongs in this conversation because PayPal is part of his origin story and because X has been openly pursuing payments through X Money, including a partnership with Visa. The provocative challenge is this: if Musk is still serious about building an everything app, he should either buy PayPal and reform it or build X Pay into the customer-respecting alternative that PayPal has failed to become for many emerging-market users. That does not mean importing Silicon Valley chaos into African finance. It means using distribution, engineering ambition and product urgency to build a payment layer that treats Nairobi, Lagos and Johannesburg as first-class markets from day one. If X Pay ever wants global credibility, it should solve the hard problem PayPal has avoided: trustworthy, low-cost, transparent, cross-border payments for the rest of the world, not only for the already banked and already privileged.

The same challenge applies to African founders. A better PayPal for Africa will not be a copy of PayPal with African colours. It will be something more native to African realities: mobile-first, identity-aware, compliance-heavy but customer-friendly, multilingual, API-rich, merchant-aware, diaspora-connected, and interoperable across wallets, banks and instant payment systems. It will understand that a $23 payment for a design gig may matter more urgently to a young freelancer than a $2,300 payment matters to a comfortable corporation. It will understand that small businesses run on cash flow, not slogans. It will price fairly, resolve disputes quickly, and publish transparency reports because trust will be its real currency.

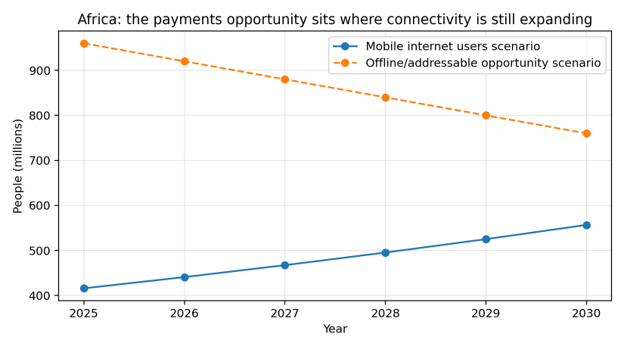

Chart 3: GSMA reports 416m people using mobile internet in Africa, while a much larger population remains addressable as connectivity improves. The future line is an opportunity scenario showing why payment platforms that ignore Africa are ignoring the next growth frontier.

The remittance context makes the case even stronger. World Bank remittance price data continues to show Sub-Saharan Africa as the most expensive region to send money to, with the total average cost recorded at 8.46 per cent in the third quarter of 2025. That is a tax on love, labour and survival. It is a tax paid by migrants supporting families, students paying fees, small traders importing stock, and communities absorbing shocks. Digital-only providers can reduce costs, but the market is still too fragmented, too dependent on foreign gatekeepers, and too slow to punish platforms that treat African users poorly. A fairer alternative would not merely compete with PayPal; it would attack one of the quietest forms of financial extraction in the global economy.

PayPal can still choose a better path. It can publish account-limitation data by region. It can create a dedicated Africa customer-rights charter. It can guarantee review timelines for frozen funds. It can partner more deeply with local banks, mobile money operators, national payment switches and regulators. It can design a proper African merchant passport for verified freelancers, creators and SMEs. It can stop forcing legitimate users to feel like defendants in a trial they cannot see. And it can admit, publicly, that equal treatment is not achieved when a platform applies the same automated suspicion to unequal realities. Fairness sometimes requires more local knowledge, not more generic automation.

But if PayPal refuses to reform, Africa should not beg. It should build. The continent has the users, the transaction behaviour, the mobile-money muscle, the instant-payment momentum, the developer talent, the diaspora flows and the political need. What it lacks is a sufficiently ambitious, well-capitalised, interoperable and trusted cross-border payments champion. That absence is not destiny. It is an opening. The next great payments company could be African, or at least Africa-first. It could be built in Nairobi, Lagos, Kigali, Cairo, Cape Town or Accra. It could begin with freelancers and merchants, then expand into trade, remittances, subscriptions, creator payments and settlement. It could turn the frustration of PayPal users into the founding energy of a new financial rail.

The deeper issue is dignity. A payment platform is not just software. It is a gate to economic participation. When it works, it lets talent travel faster than passports. When it fails, it traps people behind invisible walls. PayPal must decide whether it wants to be remembered in Africa as a bridge or a checkpoint. Enrique Lores must decide whether his leadership will be another corporate transition or the beginning of a serious repair. AfDB must decide whether digital payment sovereignty is infrastructure worthy of continental financing. Elon Musk must decide whether X Pay is theatre or a real attempt to rebuild the global money movement. And Africa’s technology community must decide whether it will keep complaining about locked accounts or build the rails that make such humiliation unnecessary.

The future of payments will not be won by the company that merely moves the most money. It will be won by the company that earns the most trust while moving money at scale. PayPal already has the scale. In Africa, it is the trust that is now on trial.

Read Also: Safaricom And PayPal Collaborate To Link Mobile Money With Online Payments