When The AI Party Met the Interest-Rate Wall – The SIB Analysis

Global markets walked into the first week of June with the confidence of a rally that had been feeding on artificial intelligence optimism. By the end of the week, that confidence had been bruised. The story was not that investors suddenly stopped believing in technology. The deeper story was that markets were forced to remember an old truth: even the strongest narrative can be humbled by interest rates, oil prices, inflation fears and geopolitical uncertainty.

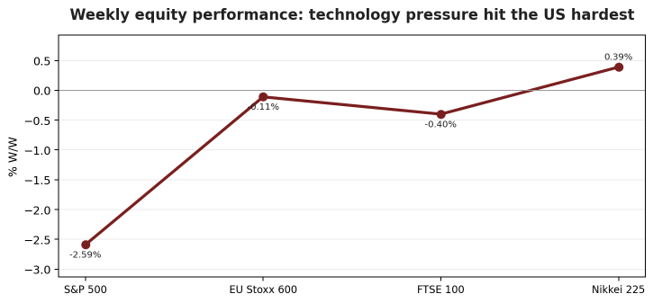

According to Standard Investment Bank’s Weekly Global Markets Brief, US equity markets ended the week lower, with the technology-heavy Nasdaq Composite posting the sharpest fall at 4.53%. The S&P 500 shed 2.59%, ending a strong nine-week winning streak, while the Dow Jones Industrial Average proved far more defensive, slipping only 0.21%. That contrast matters. It shows that the pressure was not evenly spread across the market; it was concentrated where expectations had become hottest – technology, semiconductors, and AI-linked counters.

The week began with optimism around artificial intelligence, but the optimism faded as investors confronted a cluster of risks. Oil prices remained volatile because of developments in the Middle East. Expectations for AI-related companies were already extremely high. More AI-focused equity offerings came to the market. Then the US labour data arrived stronger than expected, giving investors another reason to worry that the Federal Reserve may keep policy tighter for longer. In simple terms, the market looked at the same strong economy that normally supports shares and asked whether that strength would delay lower interest rates.

Figure 1: Weekly equity index performance from SIB data. Positive numbers show weekly gains; negative numbers show declines.

The labour market was the main macroeconomic trigger. The US economy added 172,000 jobs in May, far above forecasts that were around 80,000 to 85,000 in the brief. April payrolls were also revised upward to 179,000 from 115,000, while the unemployment rate remained unchanged at 4.3%. For households and workers, this points to an economy that has not cracked. For markets, however, it raises a different question: if jobs remain strong and price pressures remain alive, why should the Fed rush to cut rates?

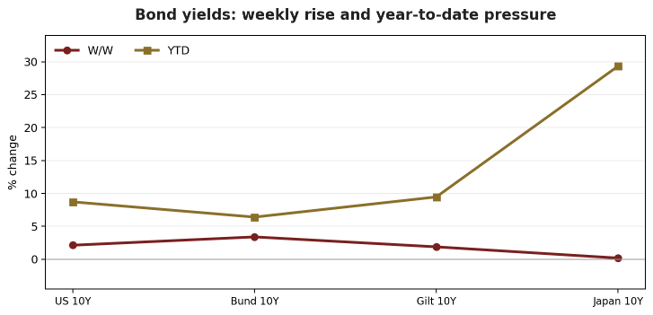

That is why bond yields moved higher. The US 10-year Treasury yield climbed to 4.53%, its highest level in weeks, while the UK 10-year gilt yield returned to 4.90%. These are not abstract numbers. Higher yields change the valuation mathematics of equities, especially growth and technology stocks whose profits are expected far into the future. When the discount rate rises, the present value of those future profits falls. That is why a higher-for-longer rates environment can quickly turn yesterday’s market darling into today’s source of volatility.

Figure 2: Bond yield movement across major markets, based on SIB-reported weekly and year-to-date changes.

Europe told a more mixed story. The pan-European STOXX 600 slipped by a modest 0.11%, while the Euro STOXX 50 edged 0.19% higher. That relative resilience did not mean Europe was free of pressure. Investors were weighing progress in US-Iran negotiations, possible ceasefire developments involving Israel and Lebanon, and the possibility of new US tariffs ranging from 10% to 12.5% on many countries. Meanwhile, eurozone data remained soft, with the economy contracting by 0.2% in the first quarter after a downward revision, while retail sales weakened across the region.

In the currency market, the US dollar regained authority. The Dollar Index rose to 100.07, gaining 1.14% for the week. The euro retreated to $1.1522, while the pound closed at $1.3342. The reason was straightforward: strong US jobs data, geopolitical uncertainty and expectations of restrictive Fed policy all supported the dollar. When the world becomes uncertain, and when US yields look attractive, capital often moves back toward the greenback.