Why Financial Literacy Is The Life Skill Every Kenyan Needs And Why Abojani Is A Practical Place To Begin

There is a quiet crisis in many homes, workplaces and businesses today. People are working, hustling, selling, borrowing, saving in small amounts, supporting families and trying to build a better life. Yet at the end of the month, many still ask the same painful question: where did the money go? That question is not a sign of laziness. It is often a sign that income has arrived without a system.

Financial literacy is the system. It is the ability to understand money in practical terms: how to earn it, budget it, save it, invest it, borrow it wisely, protect it, grow it and use it to support real life goals. It is not about sounding sophisticated. It is not about speaking difficult finance language. It is about making better decisions with the money already passing through your hands.

That is why financial literacy is no longer optional. In the modern economy, the financially literate person has an advantage. They understand that every shilling has a job. They know that debt can either build or destroy. They know that saving is not punishment, investing is not gambling, and planning is not something reserved for the rich. They know that financial confidence is built through repeated, informed decisions.

The tragedy is that many people are introduced to money only after they have already made expensive mistakes. They learn about interest after a loan has become a burden. They learn about budgeting after salaries have disappeared. They learn about investment after being misled by a scheme. They learn about emergency funds after a crisis has forced them into debt. Financial literacy helps people learn before mistakes become too costly.

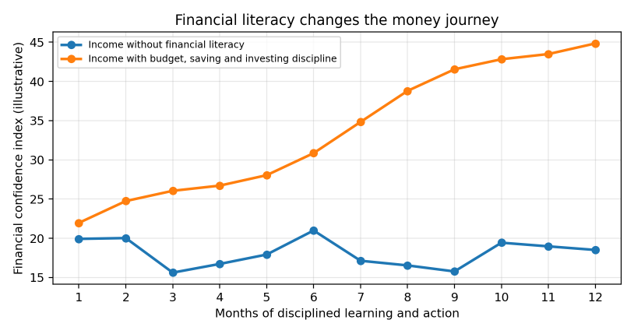

Illustrative chart: With financial literacy, discipline compounds. Without it, income can move in circles without creating progress.

The problem is not only income. It is direction.

Many people believe the only problem is that they do not earn enough. Sometimes that is true. Kenya has millions of hardworking people whose incomes are squeezed by the cost of living, school fees, rent, transport, food, medical bills and family responsibilities. But income alone cannot solve everything when money has no direction. A salary can grow and still disappear. A business can make sales and still remain broke. A household can receive money every week and still live under constant pressure.

Financial literacy teaches direction. It shows a person how to separate needs from wants, urgent costs from important goals, and productive debt from destructive debt. It teaches the discipline of writing down income, tracking expenses, building a reserve, planning purchases, and investing consistently instead of waiting for a perfect moment that may never come.

When people become financially literate, they stop treating money like an accident. They start treating it like a tool. That small shift changes everything. A tool can build a home. A tool can grow a business. A tool can educate children. A tool can create peace. But only when the person holding it knows what to do with it.

Why financial literacy must be practical, not theoretical

The best financial education is simple enough to use immediately. A person should leave a lesson knowing what to do with their next salary, their next business sale, their next loan offer, their next investment opportunity and their next emergency. That is why practical financial literacy matters more than complicated lectures.

A practical learner asks clear questions. How much do I earn? How much do I spend? What must I cut? What debt is draining me? What should I save first? Which investment matches my goal? How do I avoid fake opportunities? What is my plan for the next 12 months? What is my long-term wealth strategy? These are not academic questions. These are life questions.

This is also where a structured learning platform becomes valuable. Many people want to improve but do not know where to begin. They need someone to break down budgeting, debt management, emergency funds, taxes, money market funds, SACCOs, Treasury Bills, Treasury Bonds,