Why NCBA’s Visible Auctions Are Evidence of Scale and Transparency—Not a Broken Credit Model

A repossessed vehicle is never just metal in an auction yard. It may represent a transport business that lost a contract, a contractor who completed public work but was not paid, a family whose income collapsed, or an entrepreneur whose most ambitious investment met a harsher economy than the one described in the original business plan. The pain is real. The public anger that follows is understandable. What is not analytically sound is to turn that pain into a verdict against an entire bank without first examining the size of the lender’s portfolio, the quality of its loan book, the recovery process, and the economic conditions surrounding the borrower.

That distinction matters especially in the case of NCBA. The bank has built a public philosophy around what it calls “Banking on Belief”: the idea that a customer should not be judged only by the limitations of the present, but also by the ambition, enterprise and future potential that the customer carries. In practical banking terms, this is not charity and it is not blind optimism. It is a forward-looking credit posture that considers whether a business idea, an income-generating asset or an expansion plan can become viable when capital is placed behind it—while still applying normal underwriting, security, affordability and risk controls.

The philosophy is powerful because many Kenyan businesses would never grow if banks financed only what already existed. A truck, bus, delivery van, construction machine or manufacturing asset is often purchased before the future income it is expected to generate has fully materialised. Credit therefore converts a forecast into productive capacity. NCBA takes a view on that future and, where the case meets its lending standards, finances the belief into an asset that can work, employ people and generate cash.

|

The paradox is that the very willingness to back future potential can later be framed as a flaw when the expected cash flow fails to arrive. A borrower may have had a credible plan when the facility was approved. The bank may have financed a real asset for a real business. Yet taxes can rise, fuel and repair costs can accelerate, customers can delay payment, political uncertainty can freeze demand, or government pending bills can trap working capital for months. A loan that was reasonable at approval can become unaffordable after the operating environment changes.

Scale Creates Visibility—And Visibility Is Being Misread

The first rule of serious credit analysis is to look beyond the numerator. Thirty or fifty repossessed vehicles may appear alarming in isolation. But the figure is meaningless until it is compared with the total number and value of assets financed. A lender with a much larger portfolio can record more recoveries in absolute terms and still have a lower default ratio than a smaller competitor.

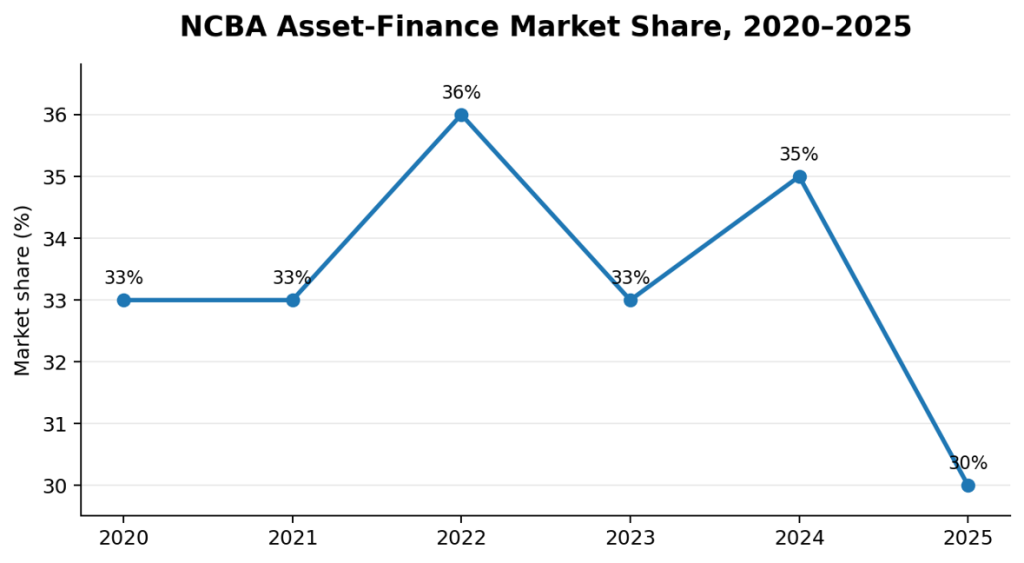

NCBA reported a 30 per cent share of Kenya’s asset-finance market in FY2025 and says it has maintained at least 30 per cent since 2020. Its disclosed share moved between 30 and 36 per cent over the six years to 2025. In plain language, about one in every three shillings deployed in Kenya’s asset-finance market is connected to NCBA. Its name will therefore appear frequently at the point of purchase, on financed logbooks, in dealership partnerships, across fleet transactions—and, inevitably, in the small proportion of cases that end in enforcement.

Figure 1: NCBA has remained Kenya’s asset-finance market leader, 2020–2025.

Source: NCBA Group FY2025 Investor Deck, March 2026. Chart: Soko Directory Research Team.

The value of the book makes the scale effect even clearer. NCBA’s asset-finance gross lending increased from KES 36 billion in 2020 to KES 52 billion in 2025, a rise of about 44 per cent in five years. That expansion represents more vehicles, machinery and equipment placed into productive use. It also means that when a fraction of borrowers fail, the absolute number of visible assets will be larger than at institutions that financed fewer assets in