Why Tax Securitisation Must Be Stopped Before It Becomes The Next Debt Trap

The numbers Kenyans must not ignore

| Item | Number | Why it matters |

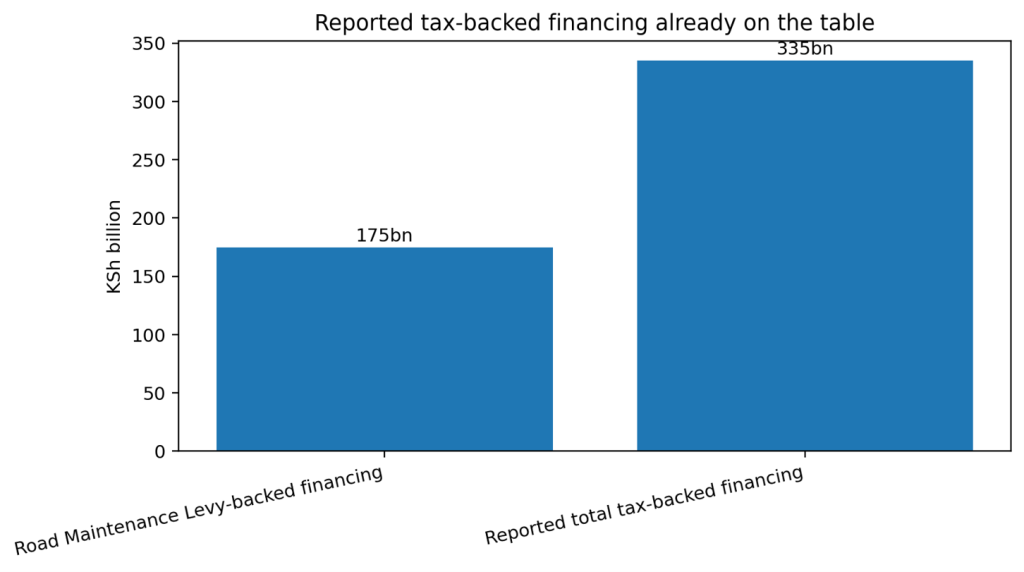

| Road Maintenance Levy-backed financing | KSh 175 billion | Reported financing raised or targeted using part of the fuel/road levy stream. |

| Road levy stream reportedly committed | KSh 7 out of every KSh 25 | About 28% of the levy stream is tied to investors before future budgets are written. |

| Reported total tax-backed financing | At least KSh 335 billion | Reported across fuel levy, sports levy, import duties and airport passenger charges. |

| FY2025/26 fiscal deficit | KSh 940 billion | Tax-backed financing equal to KSh335bn would be about 35.6% of this gap. |

| Public debt, June 2025 | KSh 11.814 trillion | Treasury data shows debt at 67.8% of GDP, before any hidden liabilities are debated. |

| Domestic maturities, June 2026 | KSh 189 billion | SIB data shows the cash pressure Treasury already faces in the domestic market. |

A government that securitises taxes is not simply borrowing money. It is doing something more dangerous: it is pledging tomorrow’s public revenue to solve today’s cash crisis. It is taking taxes that future citizens have not yet paid, assigning them to financiers today, and then pretending this is innovation. It is not innovation. It is fiscal surrender dressed in technical language.

In plain English, tax securitisation means the State identifies a future revenue stream – for example the fuel levy, a sports levy, import duty, or passenger charges – and uses that expected income to raise money upfront. Investors are paid from that future stream. The danger is that the next budget, the next Parliament, the next county allocation, and the next government may find that money already spoken for before elected leaders even debate national priorities.

That is why Kenyans must say no. Taxes are not private assets. They are not political property. They are not Treasury’s family inheritance. Taxes are public money collected under the Constitution to finance public services, equal development, social protection and national obligations. Once future taxes are pledged away, the country loses budget flexibility. Hospitals, schools, road maintenance, counties and youth programmes begin competing against contracts already signed in the shadows of previous fiscal decisions.

Chart 1: The KSh175bn road levy transaction is not additive to the wider KSh335bn figure; the larger figure is reported as total tax-backed financing across several revenue streams. Sources: Reuters, Kenyan Wall Street/BondBloX and IEA Kenya.

What has already been securitised or pledged?

The clearest public example is the Road Maintenance Levy-linked structure. Reuters reported that Kenya secured USD 600 million in short-term financing from commercial banks for road construction, backed by fuel levy collections. Reuters also reported that the government was pursuing a bigger transaction of up to USD 1.5 billion. Separately, Kenyan Wall Street reported that Roads and Transport Cabinet Secretary Davis Chirchir confirmed the government securitised part of the fuel levy to raise KSh 175 billion for road bills and projects.

The structure matters because the fuel levy is not a luxury tax sitting idle. It is money collected from motorists to maintain and develop roads. IEA Kenya noted that the Kenya Roads Board securitised a portion of the Road Maintenance Levy Fund, committing KSh 7 out of every KSh 25 collected. That is roughly 28% of the levy stream tied to financing commitments before normal public budgeting can freely allocate it.

Chart 2: If KSh7 out of every KSh25 is committed, nearly one-third of the stream is effectively pre-allocated.