Kenya’s money market sent a calm but powerful signal this week: liquidity was not in panic, investors were still willing to fund the government, and the front end of the yield curve remained the most attractive hiding place for capital seeking safety, speed, and return. The Kenya Shilling Overnight Interbank Average closed at an average of 8.75%, underlining a stable liquidity environment even as actual interbank activity cooled sharply.

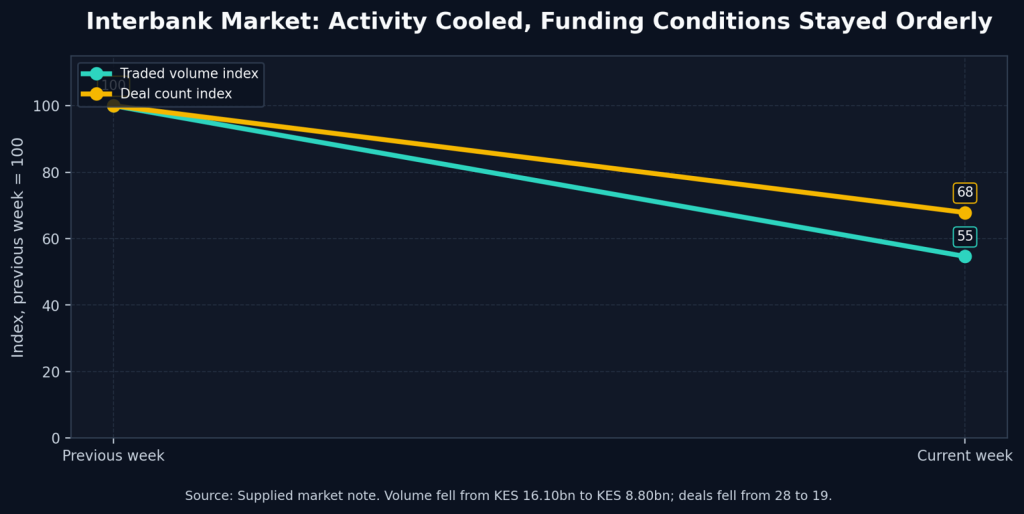

That cooling was visible in the numbers. Average interbank traded volumes fell by 45% to KES 8.80 billion from KES 16.10 billion, while the number of interbank deals dropped by 32% to 19 from 28. On the surface, that looks like a quieter market. In substance, it suggests that funding pressure remained contained: fewer banks had to chase liquidity aggressively overnight, and the market was able to settle into a more orderly rhythm without forcing KESONIA into disorderly movement.

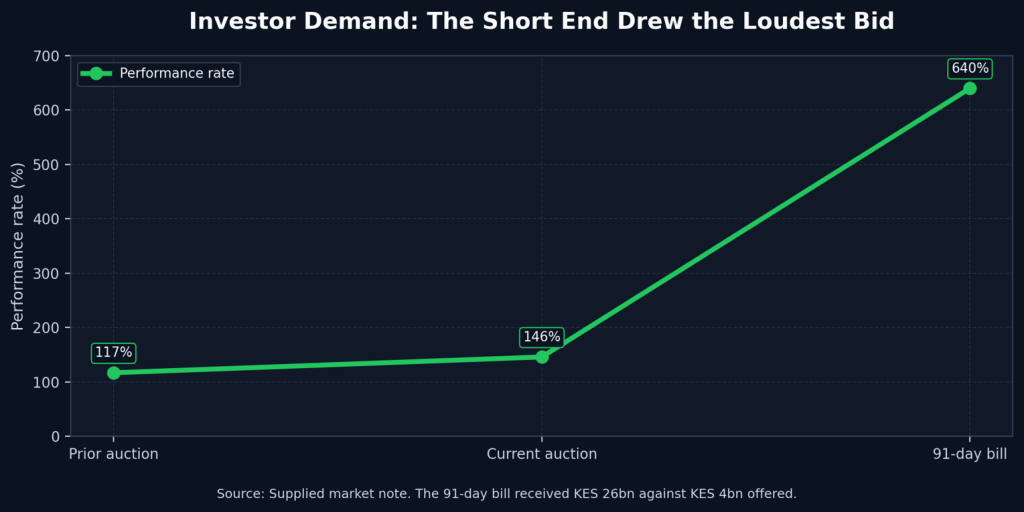

The bigger story, however, was in Treasury bills. Demand remained steady, with investors submitting KES 35.19 billion in bids, out of which KES 24.73 billion was accepted. The auction delivered a performance rate of 146%, improving from 117% in the previous week, while the 91-day Treasury bill stood out as the strongest magnet for investor money. Against an offer size of KES 4.0 billion, the 91-day paper attracted KES 26.0 billion in bids, producing a massive performance rate of 640%.

That level of appetite says something important about investor psychology. Investors are not simply buying government paper; they are choosing duration carefully. The 91-day bill is short enough to protect capital from long-term uncertainty and attractive enough to satisfy the demand for yield. In a market where inflation is sitting at 6.7% and geopolitical risks can quickly push fuel costs higher, the short end offers a rare balance: liquidity, visibility, and return without locking investors into unnecessary duration risk.

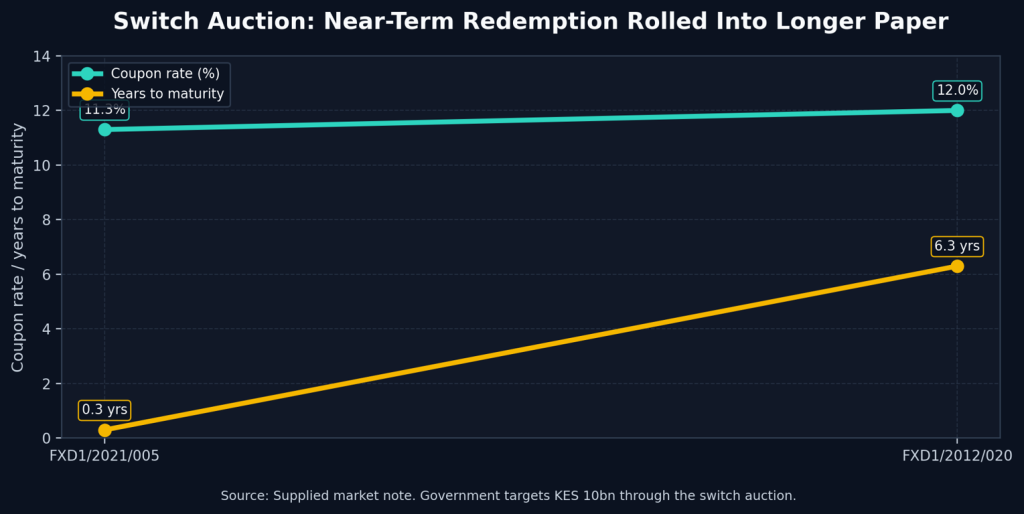

In the primary bond market, the Central Bank of Kenya announced a KES 70 billion domestic borrowing programme for July 2026 through reopened papers FXD1/2022/010, FXD1/2021/020, and FXD1/2026/030. The government is also seeking KES 10 billion through a switch auction from FXD1/2021/005 to FXD1/2012/020, moving investors from a bond with only 0.3 years to maturity and an 11.3% fixed coupon into a longer 6.3-year paper carrying a 12.0% fixed coupon. This is not just borrowing; it is liability management. It is an attempt to smooth the redemption wall and extend the debt maturity profile at a time when domestic refinancing needs remain heavy.

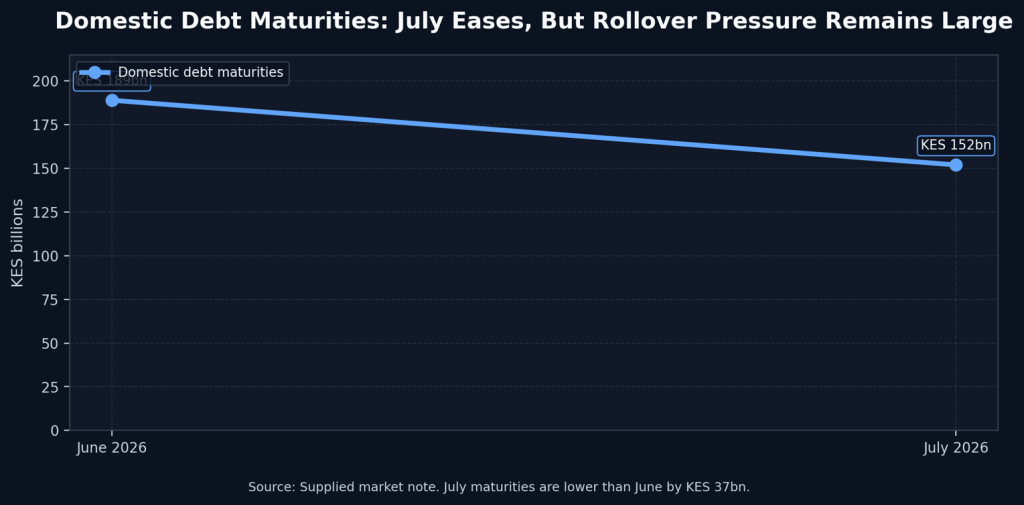

July maturities are lower than June, but they are still large. Domestic debt maturities stand at KES 152 billion in July 2026 compared to KES 189 billion in June 2026. That reduction gives the market breathing room, but not comfort. When a sovereign still needs to roll over such large sums while also funding new budgetary needs, investors retain bargaining power. If inflation pressure persists and the state leans harder on domestic borrowing, yields are likely to remain biased upward over the medium term.

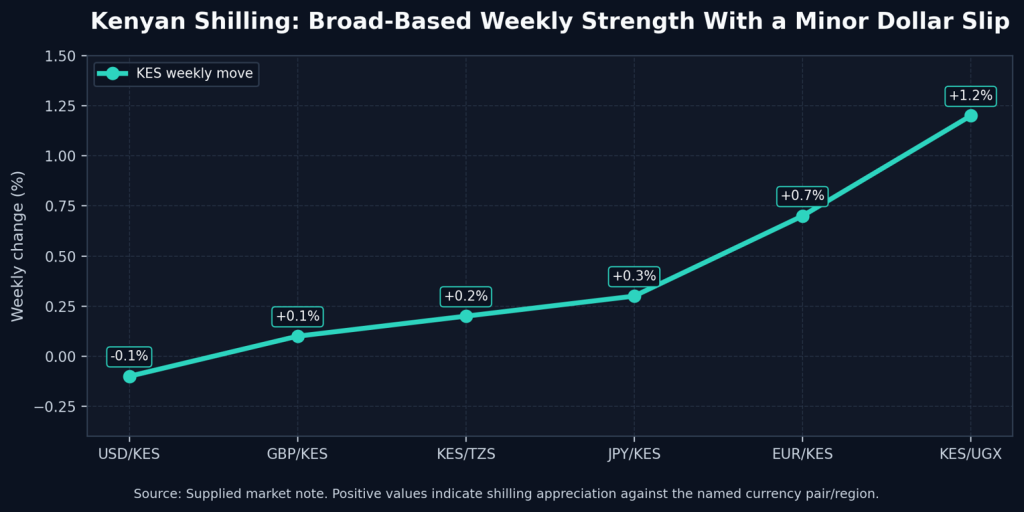

The foreign exchange market added another layer of support. The Kenyan shilling strengthened against most major currencies, gaining 0.7% against the euro, 0.3% against the Japanese yen, and 0.1% against the British pound, while weakening only slightly by 0.1% against the U.S. dollar. Regionally, the shilling appreciated by 1.2% against the Ugandan shilling and 0.2% against the Tanzanian shilling. The softer U.S. Dollar Index, down 0.2% during the week, helped reduce external pressure as safe-haven demand eased following signs of cooling tensions in the Middle East.

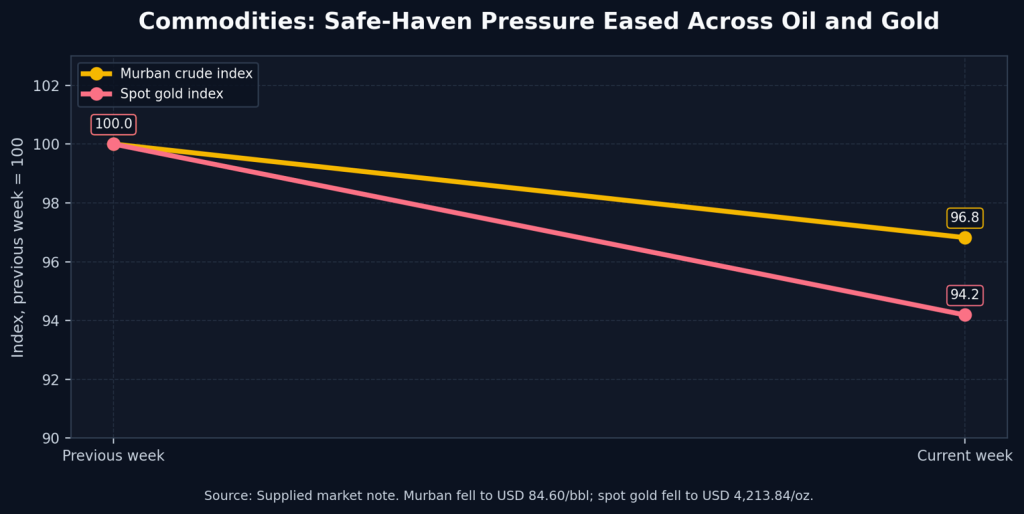

Commodity prices also worked in Kenya’s favour during the week. Murban crude fell to USD 84.60 per barrel from USD 87.38, while spot gold declined to USD 4,213.84 per ounce from USD 4,473.89 as safe-haven demand softened. For Kenya, lower oil prices matter more than market headlines: they can ease pressure on imports, reduce pass-through risk to inflation, and provide temporary relief to households and businesses already absorbing high transport and energy costs.

But the domestic real economy remains under pressure. The Stanbic Bank Kenya PMI rose to 50.0 in June, ending three consecutive months of contraction and signalling stabilisation in the private sector. Yet this was not a clean recovery. Selling prices rose at the fastest pace since January 2014 as firms passed through higher fuel levies and input costs. Production contracted for a fourth consecutive month because weak cash flows and high prices continued to restrain demand, while high transport costs created the worst supplier delivery delays since April 2020.

The encouraging counterweight was business confidence. Optimism about the coming year rose to its highest level since February 2023, with about 33% of respondents expecting higher output over the next twelve months and only 1% expecting a decline. Companies are preparing for expansion, new markets, more advertising, technology adoption, and eventual fuel price relief. Employment also rebounded, suggesting that businesses are not retreating completely; they are trying to survive the cost shock while positioning for the next cycle.

Globally, the week was shaped by cooling U.S. labour dynamics and fragile geopolitics. The June Nonfarm Payrolls report showed employment rising by only 57,000 jobs against a consensus forecast of 113,000, while a fall in active labour market participation helped push the unemployment rate down to 4.2%. The result cooled aggressive U.S. monetary-policy expectations, weakened the dollar, lifted short-term Treasuries, and reinforced the view that global capital will keep rotating quickly whenever the Federal Reserve path looks more dovish.

Energy markets remain the danger point. Threats around Middle Eastern maritime corridors, especially the strategic Strait of Hormuz, continue to keep global supply chains and oil markets on alert. Even without a full supply disruption, the risk premium matters. Any renewed shock to crude prices would land directly on Kenya’s fuel bill, transport costs, inflation path, fiscal subsidies, and consumer purchasing power. Japan’s suspected stealth intervention after the yen weakened beyond 162.80 against the U.S. dollar also reminded markets that currency stability is increasingly a policy battleground, not just a market outcome.

The investor conclusion is clear. Kenya’s money market is stable, but it is not risk-free. Liquidity is calm, short-term paper is commanding strong demand, the shilling has found support, and business confidence is rising from a low base. Yet inflation, fuel-price risk, fiscal strain, and heavy domestic borrowing remain the forces that will decide where yields go next. For now, the smart money is not running away from Kenya’s debt market; it is becoming more selective, more tactical, and more aggressive where the risk-reward is clearest.

Read Also: Mansa-X H1 2026: The Fund Turning Market Discipline Into Double-Digit Investor Returns

The charts below convert the week’s market signals into a clean visual trail for investors.

Interbank activity slowed materially, but KESONIA remained stable at an average of 8.75%.

The 91-day Treasury bill dominated demand as investors preferred short-tenor yield.

July maturities are lower than June, but the absolute refinancing load remains heavy.

The switch auction extends maturity exposure from near-redemption paper into longer fixed-coupon paper.

The shilling strengthened against most majors and regional peers, with only a slight slip against the dollar.

Oil and gold eased week-on-week as safe-haven pressure softened, lowering some external pressure on Kenya.

Read Also: Kenya’s Money Market Is Calm, But The Real Economy Is Coughing