Mansa-X H1 2026: The Fund Turning Market Discipline Into Double-Digit Investor Returns

Markets reward discipline long before they reward noise. In the first half of 2026, Mansa-X Special Fund delivered a performance profile that speaks to exactly that discipline: positive quarterly returns, a stronger second quarter, and a half-year run-rate that gives serious investors a reason to look more closely. The KES fund delivered a net return of 5.95% in Q2 2026, lifting H1 2026 performance to 10.97% net and translating into a compounded annualized net return of 23.15%. The USD fund delivered a net return of 3.56% in Q2 2026, lifting H1 2026 performance to 6.54% net and translating into a compounded annualized net return of 13.51%.

In plain language, the shilling strategy showed strong local-currency compounding, while the dollar strategy gave investors a hard-currency return profile that is difficult to ignore. That combination matters because investors are not all looking for the same thing. Some want to grow Kenya shilling capital with speed and discipline. Others want dollar exposure, purchasing-power protection, and a return profile that can sit beside global cash or near-cash alternatives. Mansa-X is speaking to both conversations at once.

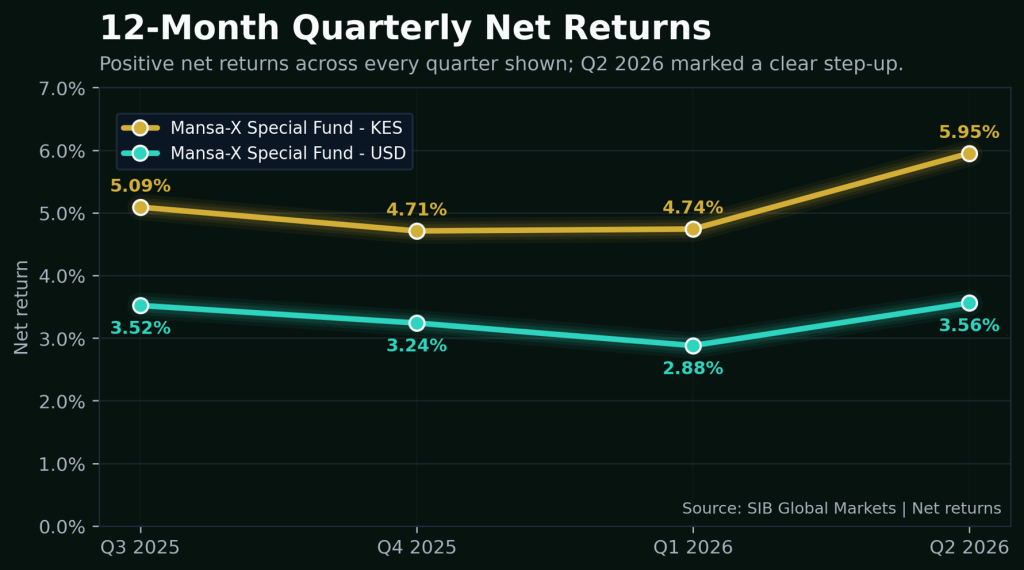

The strongest investment stories are rarely built on one isolated spike. They are built on repeatability. The twelve-month quarterly data presented by SIB Global Markets shows the KES fund posting 5.09% in Q3 2025, 4.71% in Q4 2025, 4.74% in Q1 2026 and 5.95% in Q2 2026. The USD fund posted 3.52%, 3.24%, 2.88% and 3.56% over the same reported quarters. Every quarter shown remained positive. For investors, that is the part that deserves attention: the story is not merely that Q2 was strong, but that Q2 came after an already positive sequence.

Read Also: Mansa-X Special Funds Cross USD 1 Billion Mark, Post Returns of Up to 20.74% in 2025

Figure 1: The quarterly line shows the KES fund stepping up sharply in Q2 2026, while the USD fund also rebounded from Q1. The key investor signal is consistency: all four reported quarters are positive.

What stands out in the line is the acceleration. The KES fund moved from 4.74% in Q1 2026 to 5.95% in Q2 2026, adding velocity to an already positive half-year. The USD fund moved from 2.88% to 3.56% over the same period. That matters because a strong H1 is more persuasive when the second quarter improves rather than fades. It tells investors that the period did not close on weakness; it closed with momentum.

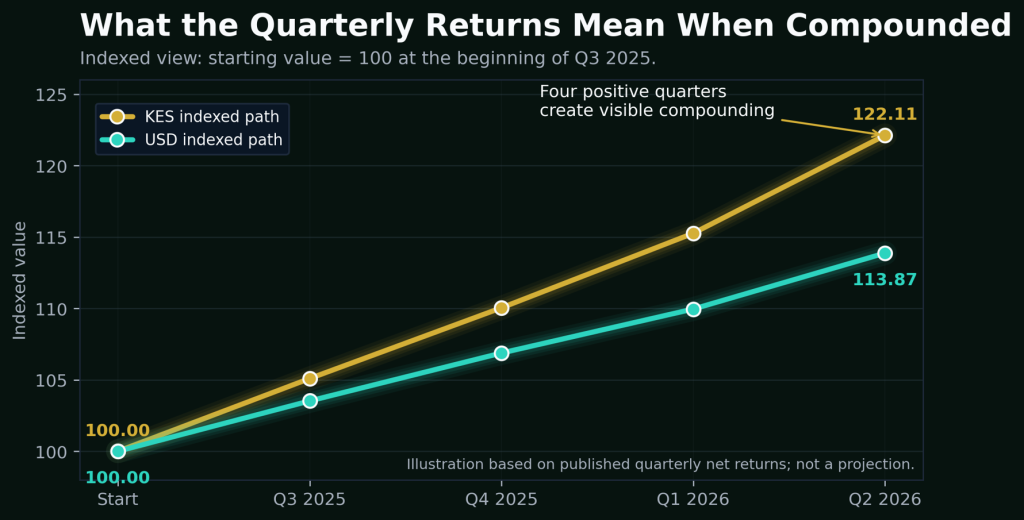

To make the numbers easier to feel, imagine an indexed value of 100 at the beginning of Q3 2025 and then apply only the quarterly net returns shown on the performance cards. By the end of Q2 2026, the KES index would stand at about 122.11, while the USD index would stand at about 113.87. This is not a projection and it is not a promise. It is a visual translation of the published quarterly returns into the language investors understand best: compounding.

Figure 2: An indexed view turns the quarterly percentages into a simple capital path. Starting at 100, the published quarterly returns compound to 122.11 for KES and 113.87 for USD over the four quarters shown.

This is the core of the Mansa-X investment argument. A return is not just a number on a marketing card. When it is preserved and extended across time, it becomes a force. A 5.95% quarterly net return on the KES fund is powerful because it builds on prior positive quarters. A 3.56% quarterly net return on the USD fund is powerful because it adds to a hard-currency track record in a period when investors are increasingly alert to currency, inflation and liquidity risk.

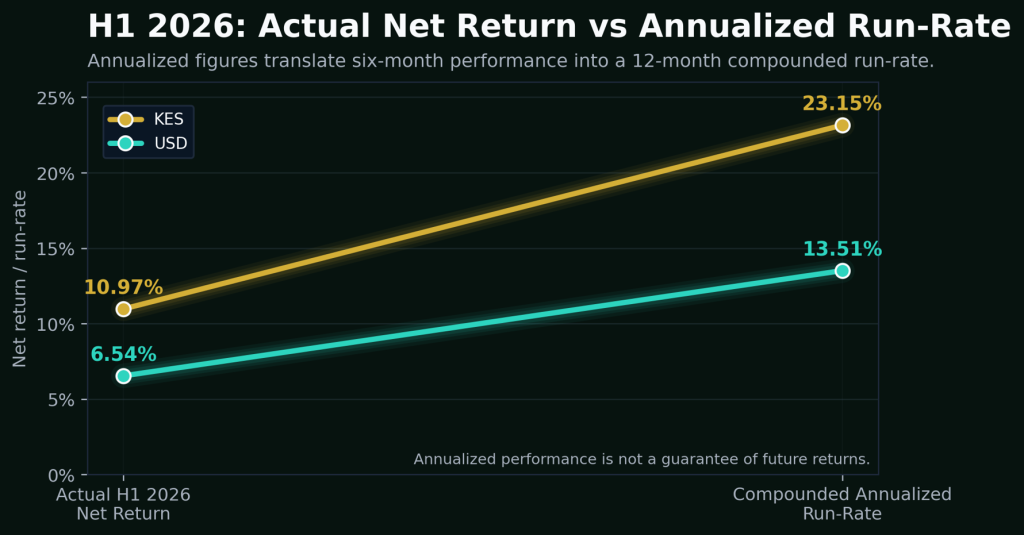

The annualized numbers also need to be understood correctly. Annualization does not say the future is guaranteed. It simply converts the actual half-year performance into a full-year compounded run-rate. That is why the KES fund’s 10.97% actual H1 net return becomes 23.15% annualized, and the USD fund’s 6.54% actual H1 net return becomes 13.51% annualized. For a serious investor, the point is not blind excitement. The point is that the reported first-half performance has created a return conversation that deserves due diligence.

Figure 3: The chart separates actual H1 performance from the annualized run-rate. The KES fund delivered 10.97% net in six months, while the USD fund delivered 6.54% net in six months.

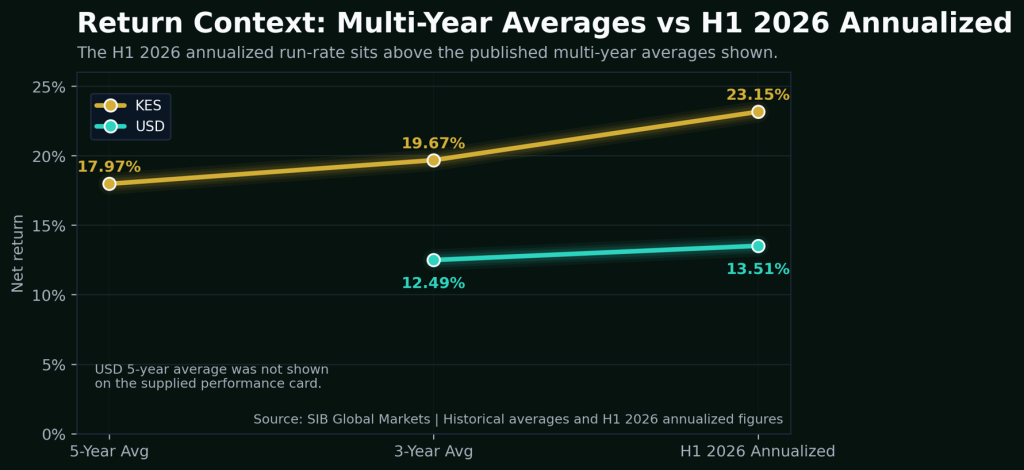

Even more importantly, the H1 2026 run-rate sits in a wider return context. The KES performance card shows a 3-year average net return of 19.67% and a 5-year average net return of 17.97%. Against that backdrop, the 23.15% annualized H1 2026 run-rate is not just a headline; it is above the published multi-year averages shown. On the USD side, the 13.51% annualized H1 2026 run-rate is also above the published 3-year average net return of 12.49%. This gives investors a more useful lens: the current half-year performance is strong, but it is also connected to a broader record presented by SIB Global Markets.

Figure 4: The KES annualized H1 2026 run-rate is above the published 3-year and 5-year averages; the USD annualized H1 2026 run-rate is above the published 3-year average.

For individuals, companies, SACCOs, family offices, diaspora investors and institutions holding idle cash, the message is direct: capital that sits still is not neutral. It is quietly tested by inflation, currency movement, opportunity cost and time. Mansa-X offers investors a regulated fund structure through which they can evaluate whether part of that capital should be put to work. The KES option speaks to investors who want local-currency growth with a strong reported H1 2026 profile. The USD option speaks to investors who want dollar-denominated exposure with a documented hard-currency return record.

That does not mean every investor should rush in emotionally. It means investors should ask sharper questions. What role should Mansa-X play in a diversified portfolio? How much liquidity does the investor need? What currency should the investor hold? What redemption terms, fees, risks and mandate details apply? Strong performance is the beginning of a serious conversation, not the end of it. The investor who treats performance as a due-diligence trigger, rather than a slogan, is the investor who allocates capital with maturity.

Mansa-X’s H1 2026 performance is therefore more than a fund update. It is a signal. It says that disciplined capital can still find growth. It says that both Kenya shilling and US dollar investors have a product worth studying. It says that in a market where many people complain about uncertainty, serious investors can still choose structure, process and compounding. In the end, wealth is rarely built by money that merely waits. It is built by capital that is placed deliberately, monitored carefully and allowed to work.

To invest in Mansa-X or learn more, visit https://sib.co.ke/mansa-x/

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (278)

- August 2026 (38)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)