Investing, just like keeping fit, is not an event. It is not a January resolution, a passing burst of motivation or something to be attempted only when money is abundant and the economy feels safe. It is a lifestyle built around a difficult but liberating decision: to deny some of today’s comfort so that tomorrow does not become a prison of dependence, debt and regret.

Anyone can begin when excitement is high. The real test is whether you can continue when the excitement disappears. In fitness, the first days are powered by motivation, but the transformation is produced by the ordinary mornings when the body is tired, the weather is unfriendly and no visible result has appeared. Investing follows the same law. The first deposit may feel inspiring, but wealth is built by the deposits made after the novelty has died.

The difficult path is rarely glamorous. It may mean driving the same car while your income rises. It may mean refusing to increase your rent simply because your friends have moved to a more fashionable neighbourhood. It may mean investing a bonus instead of using it to manufacture an image of success. It may mean being misunderstood by people who can see what you are refusing to buy but cannot yet see the freedom you are building.

That is why investing is fundamentally an identity before it becomes a portfolio. A serious investor does not ask, “Will I invest this month?” The question is already settled. They ask, “How much can I invest without weakening the stability of my household?” Investing is no longer what happens after spending. It becomes one of the first assignments given to income.

Most people are waiting for surplus money. Unfortunately, surplus money is a mirage for anyone whose lifestyle expands at the same speed as their earnings. A salary increases, and within weeks a larger house, a newer car, more expensive entertainment and additional debt arrive to consume it. The problem was never only the size of the income. The problem was the absence of a system.

A financially disciplined life reverses that order. Income arrives, the future is funded first, essential obligations are met next, and lifestyle is forced to fit what remains. This can feel restrictive in the beginning, but so does every meaningful form of training. Discipline feels like punishment only until the results begin to protect you.

Keeping fit requires repeated stress followed by recovery. Muscles grow because they are challenged consistently, not because they are comfortable. Financial strength is also created through controlled discomfort. Every time you resist an unnecessary purchase, increase a monthly contribution or continue investing during uncertainty, you are training your financial muscles to carry more weight.

The early stages can be deeply discouraging. You may invest KSh 5,000 or KSh 10,000 a month and feel that the account is not moving. The returns appear small. A single emergency can seem larger than everything you have accumulated. Meanwhile, social media displays people eating in expensive restaurants, travelling, upgrading vehicles and appearing to enjoy life without restraint.

But appearances do not reveal balance sheets. A polished lifestyle can be supported by debt, delayed bills, family pressure and an empty investment account. The person who looks behind may actually be building the only thing that matters: resilience. Financial progress is often silent long before it becomes visible.

Wealth is not built because every contribution is large. It is built because enough contributions are allowed to survive long enough to compound. At first, your money depends almost entirely on you. Later, the returns begin adding meaningful weight. Eventually, the portfolio starts producing growth that would have taken you months or years to save manually.

Time is the hidden partner in every sound investment plan. It cannot rescue a reckless asset, but it can magnify disciplined contributions into something powerful. This is why delaying the journey is so expensive. The person who starts late may contribute more aggressively, yet still struggle to catch the investor who gave smaller amounts more time to work.

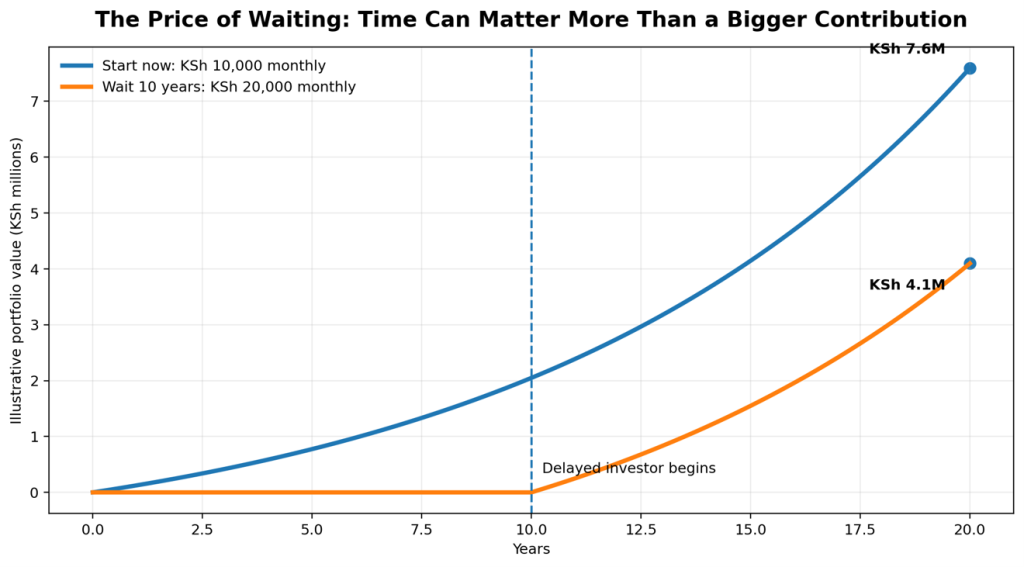

Figure 1: Starting earlier can produce more wealth even when the late starter contributes twice as much.

Illustrative model: 10% nominal annual return compounded monthly, before fees and taxes. One investor contributes KSh 10,000 monthly for 20 years; the other waits 10 years, then contributes KSh 20,000 monthly for 10 years. This is not a forecast.

The lesson is not that investment returns are guaranteed. They are not. The lesson is that time lost cannot be purchased cheaply. A delayed investor must fight two battles at once: contributing more money and compensating for years in which compounding was absent. Starting small is therefore not embarrassing. Starting small is often the most intelligent way to begin.

Consistency also matters more than occasional intensity. One person may invest KSh 100,000 once and disappear for three years. Another may invest KSh 5,000 every month, increase it gradually and continue for decades. The second investor is not merely accumulating money. They are building a behaviour that can survive changes in income, mood and economic conditions.

Motivation cannot carry a twenty-year plan. Systems can. Standing orders, payroll deductions and scheduled transfers reduce the number of emotional decisions required. They make the correct action automatic. When investing depends on whatever is left in the account at the end of the month, consumption will usually win. When investing happens first, the lifestyle is forced to negotiate with reality.

However, discipline does not mean investing without protection. A person who has no emergency fund may be forced to sell a good investment at the worst possible time. A household drowning in expensive debt may be contributing to an investment while losing more money through interest elsewhere. The lifestyle of investing therefore includes budgeting, insurance, manageable debt, adequate liquidity and honest record-keeping.

It also requires diversification. Fitness is not built by training one muscle and neglecting the rest of the body. In the same way, financial security should not depend entirely on one company, one property, one customer, one currency or one source of income. Concentration can create extraordinary gains, but it can also create extraordinary damage. A durable life is built with enough balance to survive being wrong.

The hardest moments arrive when markets fall. A portfolio that looked intelligent during a rally suddenly appears foolish. Headlines become dramatic. Friends who never studied the investment begin issuing confident warnings. Fear convinces people that selling will end the discomfort.

Yet selling does not merely remove volatility. It can convert a temporary decline into a permanent loss. The investor then faces a second impossible decision: when to return. Most people do not re-enter when prices are still low and fear is high. They wait for reassuring headlines, by which time a significant part of the recovery may already have happened.

Holding through thick and thin does not mean holding blindly. Patience is not denial. A disciplined investor must keep asking whether the original investment case remains sound. Has the business lost its competitive advantage? Has debt become dangerous? Has governance deteriorated? Has the investment become too expensive relative to its likely future cash flows? If the facts have changed materially, changing the decision is wisdom, not weakness.

But when the fundamentals remain intact and the only thing that has changed is the market’s mood, panic is often the most expensive strategy available. The market can recover before confidence does. That is why emotional control is not an optional quality. It is part of the return.

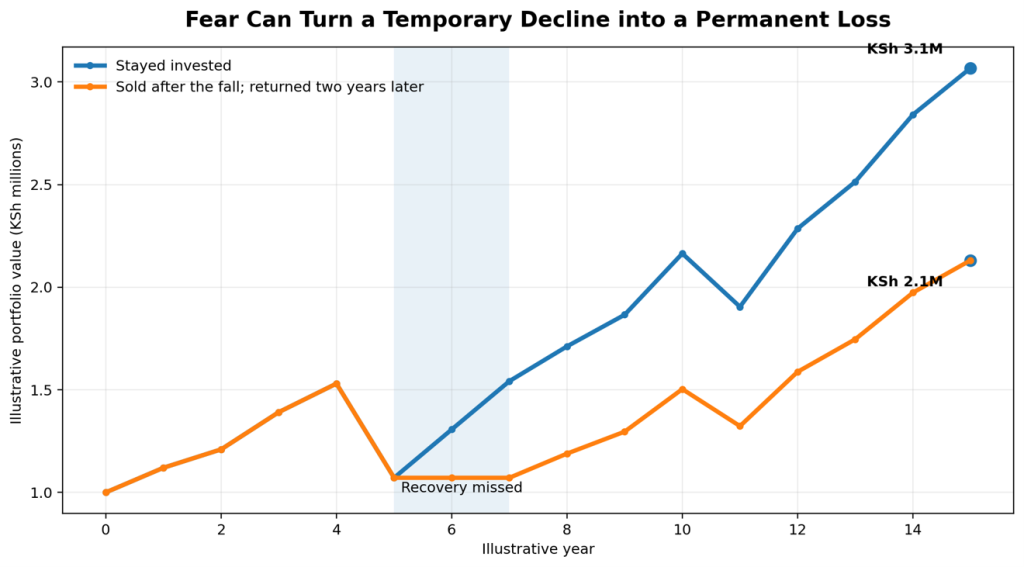

Figure 2: Missing the recovery can leave a permanent gap between the patient investor and the panic seller.

Hypothetical illustration using a KSh 1 million starting portfolio and a sequence of positive and negative annual returns. The panic seller exits after a 30% decline, remains in cash for two recovery years, then returns. It is an educational example, not historical market data or a forecast.

The difference shown above is not created by a magical stock pick. It is created by behaviour. Both investors experienced the same decline. Only one remained positioned for the recovery. The other escaped the pain but also abandoned the opportunity that normally follows fear.

This is why the greatest investment risk is sometimes not the market. It is the undisciplined version of ourselves: the version that buys because everyone is excited, sells because everyone is terrified, borrows to chase quick returns and abandons a long-term plan whenever progress becomes boring.

Financial strength is built in the boring seasons. It is built when there is no applause, no viral screenshot and no dramatic gain to display. It is built when you read, save, review, rebalance and continue. The public usually sees the result. It rarely sees the repetition that produced it.

There will be months when life interrupts the plan. A medical bill may arise. A business may lose a major client. School fees may increase. Employment may become uncertain. During a genuine crisis, reducing or pausing a contribution is not failure. The mistake is allowing a temporary interruption to become a permanent surrender.

A person who misses one workout has not lost their health. A person who misses one investment contribution has not destroyed their future. The danger begins when shame, discouragement or lifestyle expansion prevents them from returning. Resilience is not perfection. It is the ability to restart quickly and intelligently.

Investing should also grow with you. When income rises, the contribution should rise before lifestyle consumes the entire increase. When debt is cleared, part of the old repayment should be redirected into assets. When a business becomes profitable, a portion of those profits should leave the operating account and begin building long-term security.

The aim is not to become wealthy merely to display wealth. The aim is to acquire choice. Choice to leave an abusive workplace. Choice to finance a child’s education without humiliation. Choice to survive illness without selling everything. Choice to support ageing parents. Choice to start a business, retire with dignity, give generously and sleep without fearing every emergency.

That freedom is purchased gradually. It is purchased by thousands of decisions that may appear insignificant in isolation. A skipped impulse purchase. A contribution made during a difficult month. A bonus invested. A dividend reinvested. A loan rejected. A bad asset sold after careful analysis. A good asset held despite temporary noise.

Every shilling is a worker. Some are sent to serve today’s appetite and disappear immediately. Others are sent into productive assets where they can return with more workers. The wealthy are not simply people who earn money. They are people who repeatedly give money productive assignments.

This does not require worshipping money or postponing every joy. A sustainable investment lifestyle must leave room for living, generosity, family and rest. Extreme deprivation is difficult to maintain and can eventually trigger destructive spending. The goal is not misery. The goal is intentionality: spending on what genuinely matters and refusing to finance an image that weakens the future.

The difficult path is difficult because it requires saying no while others are saying yes. It requires patience in a culture of instant results. It requires humility in a culture of performance. It requires continuing when progress is invisible and courage when the crowd is afraid.

But the alternative is harder.

It is harder to reach middle age with a high income and nothing accumulated. It is harder to face retirement while still depending on the next salary. It is harder to explain to your children that every opportunity must be postponed because no financial cushion was built. It is harder to be one emergency away from collapse after decades of work.

Investing is therefore not just about return. It is about responsibility. It is an act of respect for the person you will become, the people who depend on you and the dreams that cannot be funded by hope alone.

Choose the difficult path while you still have time. Begin with what you have. Build an emergency fund. Eliminate destructive debt. Invest consistently. Diversify thoughtfully. Study what you own. Ignore noise, but never ignore facts. Increase your contribution as your capacity grows.

Do not wait to feel ready. Readiness often arrives after the first disciplined step, not before it. Do not wait for the perfect market. There will always be uncertainty. Do not wait for a perfect income. A larger income without stronger habits can simply finance a larger financial problem.

One day, the sacrifices that currently feel invisible will begin to speak. The account that once looked painfully small will become a buffer. The dividends that once appeared meaningless will begin paying real bills. The assets accumulated quietly will begin giving you options that income alone could never guarantee.

People may call it luck because they did not see the years when you kept going. They did not see the purchases you postponed, the market declines you endured, the mistakes you corrected or the consistency you protected.

But you will know the truth.

You chose temporary discomfort over permanent vulnerability. You stayed disciplined after motivation disappeared. You held on when the journey became heavy, and you adjusted when the facts genuinely changed.

That is how financial strength is built. Not in one dramatic moment, but one contribution, one sacrifice, one intelligent decision and one difficult season at a time.

The hard road does not merely lead to wealth. Walked wisely and consistently, it leads to freedom.