If I were leading Safaricom, I would convene every serious source of domestic liquidity in the country — banks, SACCOs and well-run microfinance institutions — and put one proposition on the table: allocate a defined portion of deposits into a disciplined, data-driven lending pool that can be deployed through Fuliza and M-Shwari. Kenya does not have a shortage of hustle. Kenya has a shortage of affordable, predictable working capital. That is the gap these products have helped to close, and the numbers already show the scale of the opportunity.

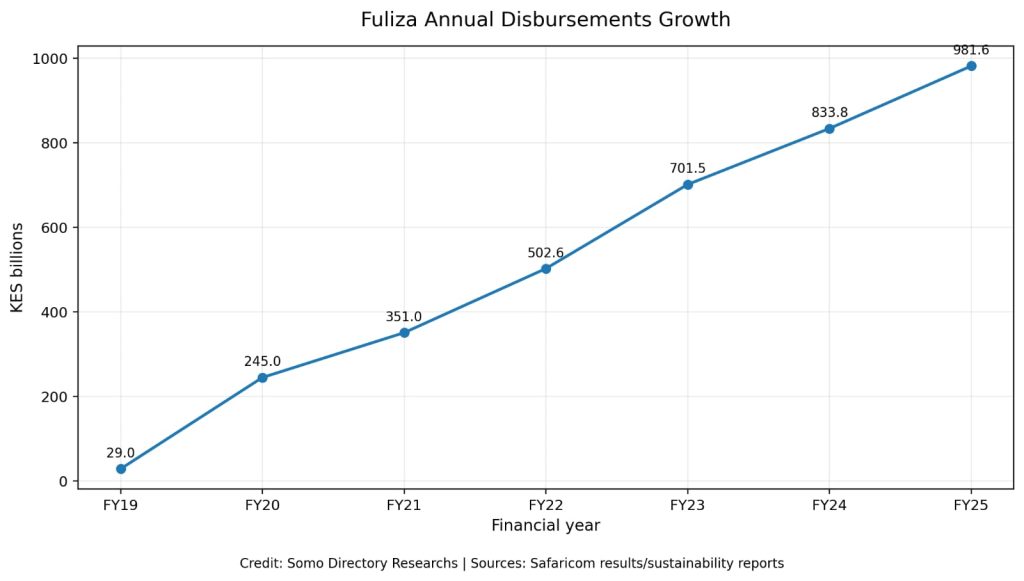

Fuliza is no longer a side product. It is a cash-flow engine embedded in the daily life of millions of Kenyans. Safaricom’s latest full-year disclosures show Fuliza disbursements at about KSh 981.6 billion in a year. That works out to roughly KSh 2.69 billion every day, KSh 18.88 billion every week, and about KSh 81.8 billion every month. NCBA’s 2024 annual report adds the long-view: from inception to 31 December 2024, Fuliza had disbursed 7.54 billion loans with a cumulative value of about USD 22.4 billion. That is not a fringe facility. That is a national liquidity rail.

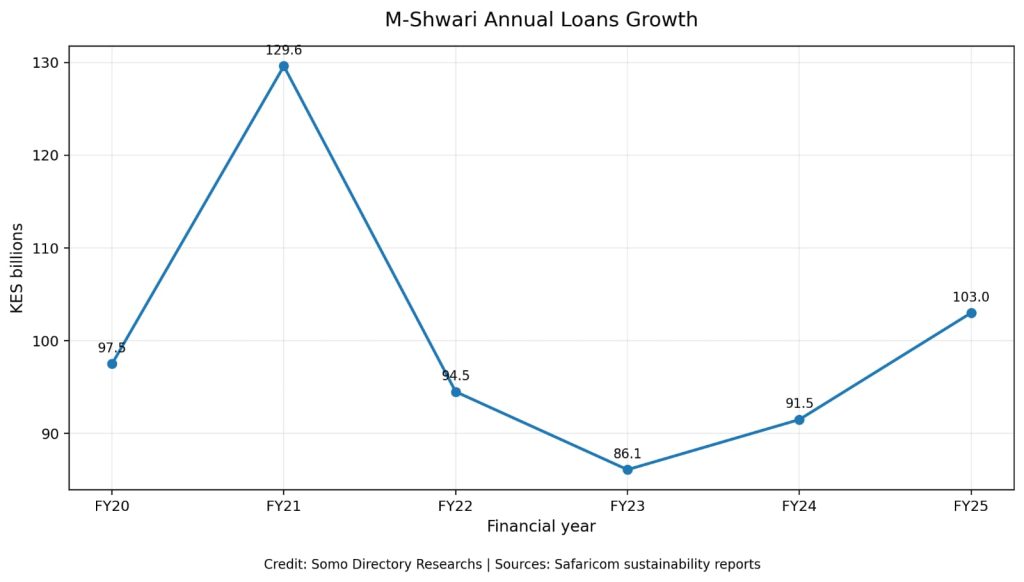

M-Shwari tells a different but equally important story. It has been one of the clearest proofs that digital finance can build both credit access and a savings culture at the same time. The latest disclosed annual loan value for M-Shwari stands at about KSh 103.0 billion. That translates to around KSh 282.2 million a day, KSh 1.98 billion a week, and about KSh 8.58 billion a month. Since inception to 31 December 2024, NCBA reports that M-Shwari had disbursed 210.7 million loans with a cumulative value of about USD 6.06 billion. Put simply, this is one of the most consequential retail financial products Kenya has produced in the mobile era.

That is why I would think bigger. Instead of leaving small-business liquidity to predatory digital lenders and shylocks, I would build a deeper, broader credit marketplace around the rails that already work. Safaricom, through M-PESA, sees the movement of money in real time. It sees income patterns, repayment behavior, merchant flows and cash cycle realities with a depth that most lenders can only dream of. That visibility does not eliminate risk, but it dramatically improves underwriting, pricing and collections.

The real crisis in Kenya is not that people hate debt. The real crisis is that too many people are borrowing from the wrong places, at the wrong price, under the wrong terms. A boda rider, kiosk owner, mama mboga, freelance technician or small trader usually does not need toxic money. They need timely money. They need stock money. Float money. School-fee bridge money. Emergency supplier money. Business continuity money. When cash flow is predictable, debt can be productive. When cash flow is starved, the entire economy starts borrowing just to survive.

Fuliza and M-Shwari have proved that small-ticket lending at scale can be done faster, cleaner and with more dignity than what millions of Kenyans face in the informal credit market. The next step is to industrialize that model responsibly. Let banks bring balance-sheet muscle. Let SACCOs bring community trust and member knowledge. Let MFIs bring customer segmentation and field experience. Let Safaricom bring the rails, the data signals, the user base and the collection architecture. Then structure the pool properly, price it responsibly and build consumer protections into the core.

The argument here is not for reckless lending. It is for smarter lending. It is for replacing panic borrowing with productive borrowing. It is for moving Kenya away from exploitative digital debt traps and toward credit that actually supports commerce. It is also for recognizing what the data is already suggesting: repayment discipline is stronger than many elites assume when the product matches the customer’s real cash cycle. Safaricom’s FY25 disclosures show Fuliza repayments of about KSh 996.7 billion against KSh 981.6 billion in disbursements during the year, a sign of powerful collection velocity within the ecosystem.

Kenya’s entrepreneurs are not asking for miracles. Most are asking for breathing room. They are asking for working capital that does not destroy them before it helps them. They are asking for a financial system that understands that the difference between collapse and growth is often just one week of cash flow. If the country is serious about supporting MSMEs, protecting households and expanding financial inclusion, then scaling responsible, affordable digital liquidity should be near the top of the agenda.

So yes, if I were the CEO of Safaricom, I would call that meeting. I would tell every bank, SACCO and MFI in the room that the country has already shown us the demand. Fuliza and M-Shwari have already shown us the rails. The only remaining question is whether Kenya’s financial system is bold enough to pool capital around what is already working — and disciplined enough to do it in a way that grows businesses instead of trapping them.

Read Also: The Fuliza Magic That Powers Kenya’s Kadogo Economy