Most businesses do not collapse because the founder lacked ambition. They collapse because ambition moved faster than financial discipline, operational visibility and the ability to repeat good decisions. A business may have customers, social attention, energetic employees and rising sales, yet remain dangerously fragile beneath the surface. Success is therefore not simply the act of selling more. It is the construction of an enterprise that can absorb shocks, meet obligations, learn from mistakes and continue delivering value when conditions become difficult.

Scale does not repair weak foundations; it magnifies them. When a small business has poor records, confused pricing, uncontrolled withdrawals or inconsistent service, expansion multiplies each weakness across more customers, more stock, more employees and more debt. The business becomes larger, but not stronger. The central lesson from the Soko Directory Research framework is that sustainable growth is a consequence of ten connected disciplines. None operates in isolation, and neglecting one eventually weakens the rest.

The first discipline is cash-flow control because cash, not accounting profit, pays salaries, suppliers, rent, taxes and lenders. A company can report a healthy profit and still fail when its customers pay after ninety days while its own obligations fall due every week. This timing mismatch is one of the most common and least understood causes of business distress. The entrepreneur must therefore know not only how much the company has sold, but when the money will actually arrive and what must be paid before then.

A serious enterprise prepares a rolling cash-flow forecast that looks ahead by at least thirteen weeks. It tracks expected collections, payroll, rent, loan instalments, stock purchases, taxes and all major commitments. The forecast is updated with reality rather than hope. Delayed invoices are moved to their probable collection dates, uncertain sales are discounted, and known obligations are recorded in full. This gives management enough warning to reduce costs, negotiate terms or accelerate collections before a shortage becomes an emergency.

Cash-flow discipline also requires a clear collection policy. Invoices should be issued immediately, payment terms should be agreed before work begins, and overdue accounts should be followed up consistently. Deposits, milestone billing and incentives for early payment can reduce the amount of working capital trapped in receivables. At the same time, a reserve should be built gradually. Even one month of essential operating costs can protect a business from panic borrowing, distressed stock sales and damaging decisions made under pressure.

The second discipline is accurate record keeping. Records are the institutional memory of the business. Without them, the owner is forced to manage by emotion, selective memory and the balance displayed on a mobile banking screen. That is not management; it is guesswork. Every sale, expense, purchase, debt, inventory movement, customer payment and owner withdrawal must be captured in a consistent system that can be reviewed and reconciled.

Good records transform daily activity into decision-making intelligence. They reveal which products carry the best margins, which customers delay payment, which branches consume cash, which expenses are rising and where stock is disappearing. They also improve tax compliance, reduce fraud and make the company more credible to banks, investors and strategic partners. A business asking for capital without reliable records is effectively asking outsiders to trust what its own management cannot demonstrate.

The third discipline is understanding margins and unit economics. Revenue is an important signal, but it is not proof of value creation. A business can sell more and become poorer when the selling price does not adequately cover materials, labour, transport, commissions, financing, wastage and overheads. Each product or service must therefore be evaluated according to its real contribution after all direct costs have been considered.

Pricing should never be based only on what competitors charge or what customers say they can afford. It must begin with the full cost of delivering the product, the risks assumed, the value created and the margin required to keep the enterprise healthy. When costs change, prices and operating methods must be reviewed. A company that is afraid to correct unsustainable pricing may preserve sales in the short term while quietly financing customers from its own shrinking cash reserves.

The fourth discipline is intelligent debt management. Debt is neither automatically good nor automatically bad. It is productive when it finances an asset, stock cycle or expansion that generates more cash than the total cost of borrowing. It is destructive when it covers recurring losses, uncontrolled lifestyle spending or obligations that the business has no realistic capacity to repay. The purpose of the borrowing matters as much as the interest rate.

Before accepting a loan, management should test repayment under conservative assumptions. What happens if sales fall by twenty per cent, customers delay payment by thirty days, a key machine fails or a major contract is lost? The business should calculate the debt-service coverage available in each scenario and understand every fee, penalty, security requirement and personal guarantee. Debt taken on optimistic projections can become a permanent claim on future cash flow long after the original growth plan has failed.

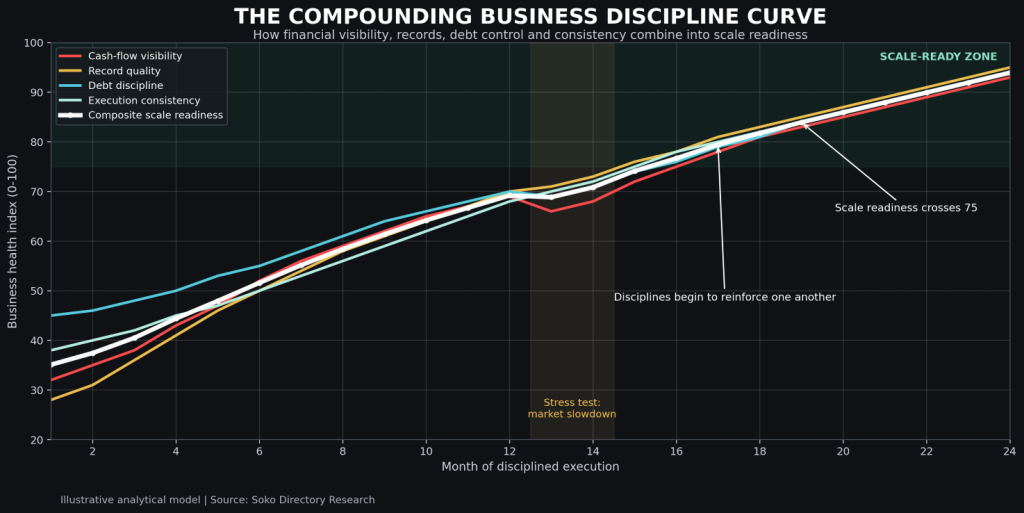

These first four disciplines begin to reinforce one another. Better records improve cash forecasts. Better cash forecasts expose weak margins. Better margin analysis improves pricing. Better pricing strengthens the ability to service productive debt. As the first graph shows, scale readiness is not created by one dramatic decision. It emerges as financial visibility and operating discipline compound over time, including during periods of market stress.

Figure 1: The compounding business discipline curve. Indices are an illustrative analytical model developed by Soko Directory Research; they are not survey observations.

| “Scale readiness is not created by one dramatic decision. It emerges when disciplined decisions reinforce one another over time.” |

The fifth discipline is the ability to learn from failure without allowing failure to define the enterprise. A failed product, delayed expansion, lost client or poor hiring decision should not be treated merely as humiliation. It is evidence that an assumption, process or decision was wrong. The entrepreneur’s responsibility is to identify exactly what failed, why it failed and what must change before the business commits more money to the same path.

A useful failure review separates facts from excuses. Was demand overestimated? Was the offer poorly positioned? Did the business underestimate costs, choose the wrong channel, hire without clear accountability or expand before systems were ready? The answer should lead to a written correction, a new measurable test and a limit on further losses. Failure becomes truly expensive when the founder protects pride, repeats the same assumptions and calls persistence what is actually refusal to learn.

The sixth discipline is consistency. Markets reward enterprises that can be trusted to deliver the promised quality, at the promised time, through a repeatable customer experience. Occasional brilliance does not compensate for chronic unreliability. A customer who receives excellent service once and poor service twice will remember the uncertainty, not the exceptional moment. Consistency therefore converts competence into reputation and reputation into recurring revenue.

Consistency is built through cadence rather than motivation. The company must have daily, weekly and monthly routines for sales follow-up, customer service, stock checks, collections, quality control and financial review. Important tasks should have named owners, deadlines and visible measures. When execution depends entirely on the founder’s mood or physical presence, the business has not yet developed an operating system. It has only developed a hardworking individual surrounded by activity.

This discipline also applies to communication. Customers should know when orders will be delivered, employees should know what success looks like, and suppliers should receive honest information when payments are delayed. Reliable communication preserves trust even when a problem occurs. Silence, avoidance and changing explanations often damage a relationship more deeply than the original operational failure.

The seventh discipline is separating business money from personal money. Mixing the two makes it impossible to know whether the enterprise is profitable, whether the owner is over-withdrawing or whether working capital is being consumed by household needs. The business should operate through dedicated accounts, and every owner withdrawal should be recorded. The founder should receive a defined salary or documented draw that the company can genuinely afford.

This separation is not only an accounting preference; it is a governance boundary. It forces the owner to recognise that revenue belongs first to the enterprise until suppliers, employees, taxes, debt and reinvestment requirements have been addressed. Treating every customer payment as personal income produces the illusion of wealth while gradually starving the business of stock, maintenance, marketing and reserves.

The eighth discipline is detecting warning signs early. Businesses rarely fail in a single day. Distress normally appears through patterns: sales begin to slow, gross margins narrow, overdue invoices increase, suppliers demand cash, stock remains unsold, complaints rise, key employees leave and ordinary expenses are financed through repeated borrowing. Each sign may appear manageable on its own, but together they indicate that the business model is losing stability.

Read Also: Kenya’s Most Expensive Lie: Performing Prosperity While Living One Emergency from Ruin

Management should hold a weekly business-health review built around a limited set of numbers: cash available, cash expected, receivables overdue, gross margin, stock movement, payroll obligations, debt instalments, customer complaints and sales pipeline. The purpose is not to produce a beautiful report. It is to identify deviations early enough to act. A difficult decision made when the warning first appears is usually cheaper than the same decision made after cash has run out.

The ninth discipline is controlled growth. Expansion should follow proof that the existing operation is profitable, repeatable and sufficiently funded. New branches, larger orders and more employees all require working capital before they generate returns. When a company expands faster than its ability to finance stock, supervise quality and collect cash, growth becomes a source of distress rather than strength.

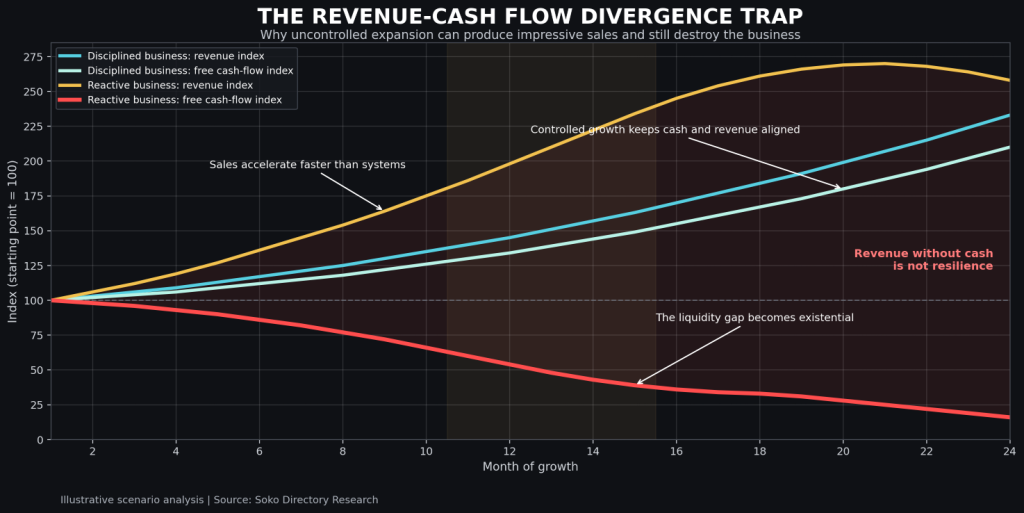

The second graph illustrates the central danger. A reactive business can record rapidly rising revenue while free cash flow collapses. More orders create more inventory needs, more receivables, more overtime, more transport costs and more borrowing. From the outside, the business appears successful. Internally, every additional sale increases the liquidity gap. A disciplined business grows more deliberately, keeping revenue and cash generation aligned so that expansion strengthens rather than consumes the enterprise.

Figure 2: The revenue-cash flow divergence trap. This scenario model shows how sales can rise while free cash flow falls when expansion is not matched by working capital and systems. Source: Soko Directory Research.

Before scaling, management should document the process that produces the result. It should know how a sale is generated, how an order is fulfilled, how quality is checked, how payment is collected and how exceptions are handled. The team must be trained, responsibilities must be delegated and controls must work without constant intervention from the founder. Scale is the multiplication of a system; where no system exists, expansion multiplies confusion.

The tenth discipline is patient consistency combined with intelligent adaptation. Entrepreneurship often requires years of effort before trust, distribution, brand recognition and operational competence become visible in the financial results. The founder must continue doing the essential work even when applause is absent. At the same time, patience must not become stubbornness. The goal can remain constant while products, prices, channels, staffing and strategy change in response to evidence.

This is why measurement matters. Consistency without measurement can repeat inefficiency, while adaptation without consistency produces endless experiments that never mature. The strongest businesses establish clear targets, review outcomes and improve one cycle at a time. They preserve what works, correct what does not and avoid abandoning a sound strategy simply because the results have not arrived as quickly as expected.

The ten disciplines form one operating system. Cash-flow control creates survival time. Records create visibility. Margin discipline creates economic value. Responsible debt creates productive leverage. Learning from failure improves judgement. Consistency creates trust. Financial separation protects working capital. Early-warning reviews protect management from surprise. Controlled growth protects quality and liquidity. Patient adaptation allows the company to compound these advantages over time.

An entrepreneur who wants to implement this framework should begin with a ninety-day reset. In the first month, clean the records, separate accounts, list all debts and prepare a thirteen-week cash-flow forecast. In the second month, review product margins, pricing, collections, stock and recurring expenses. In the third month, document core processes, establish weekly reviews and define the conditions that must be met before the next expansion. The objective is not perfection. It is visibility, control and a repeatable management rhythm.

Business success is frequently presented as a story of bold ideas, rapid expansion and fearless risk-taking. Those qualities have value, but they become dangerous when detached from discipline. The enterprise that lasts is usually the one that respects cash, records the truth, prices correctly, borrows carefully, learns quickly and delivers consistently. It grows when the foundations are ready, not when pressure or excitement makes expansion attractive.

The final test of a business is not how impressive it appears during favourable conditions. It is whether it can continue paying, producing, learning and serving when demand weakens, costs rise or a major assumption fails. That resilience is constructed long before the crisis arrives. It is built in the weekly forecast, the reconciled account, the corrected price, the difficult collection call, the controlled withdrawal and the disciplined decision to delay growth until the business is genuinely ready.

The discipline must therefore come before the scale. Entrepreneurs who master these ten issues do more than protect themselves from failure. They create companies that can attract capital, retain talent, earn customer trust, survive shocks and expand without losing control. That is the difference between a venture that is temporarily busy and an institution that is capable of becoming valuable, durable and great.