Kenya’s Insurance Sector Saturated with Low Penetration – Report

The insurance sector in Kenya is saturated and faces low penetration rates in one of the best-regulated markets. The insurance sector is fragmented and competition is tough according to Cytonn Investment Kenya Listed Insurance Companies FY’2015 Report.

“The number of insurance companies in Kenya amount to 49 firms, which equates to about 1.1 insurance company for every 1 million Kenyans, a similar ratio to Kenya’s banking sector. However penetration still remains low at 3.0 percent, lower than the average of 3.8 percent in Africa, having remained at this figure for a number of years,” reads the report.

The report themed, “Given turbulence in banking, is all well in insurance?”, says the sector grapples with low penetration, slowing premium growth, increased cases of fraudulent claims and the required increase in capital following adoption of a risk based capital adequacy framework.

Analysts emphasise that a sustained influx of capital will prove crucial, and insurance companies will need to build capital quickly. This will be through investing in technology to stay competitive.

“We are of the view that insurance companies have a lot they can do in order to register considerable growth and improve penetration in the country. Foremost, we expect an uptick in relationships between banks and insurance companies to introduce bancassurance as well as the integration of mobile money payments to allow for policy payments through this increasingly preferred transaction medium.”

“The core issue we see is to innovate into more relevant products to improve uptake. Significant opportunities remain in the Kenyan insurance market, with growth areas identified especially in commercial lines such as oil, real estate and infrastructure.”

In contrast to the Kenya National Bureau of Statistics (KNBS) 2016 Economic Outlook that said growth in 2015 was supported by a stable macroeconomic environment, and improvement in the agriculture, finance and insurance sectors, Cytonn notes the Insurance sector, “With an industry combined ratio average at 113.8 per cent, insurance companies are not profitable from their core business and diversification of their revenues is key to profitability “ besides experiencing robust growth over the years, with the financial services sector in Kenya currently contributing 10.1 percent to Kenya’s GDP growth, from a 3.5 per cent contribution 10-years ago.

This is as a result of:

- Convenience and efficiency through insurance firms adopting alternative channels for both distribution and premium collection such as bancassurance and improved agency networks,

- Advancement in technology and innovation making it possible to make premium payments through mobile phones, and

- A demographic boost in Kenya, such as a growing middle class, which has led to increased disposable income, thereby increasing demand for insurance products and services.

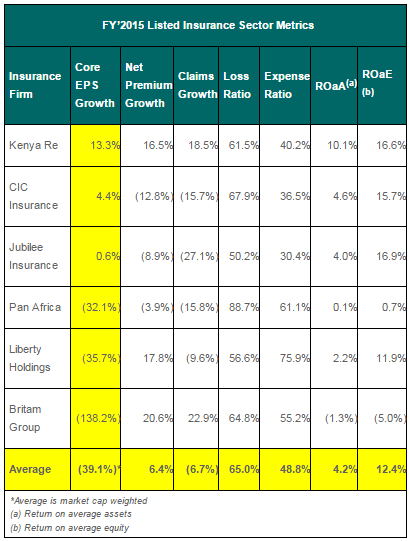

Thus, the insurance sector sector recorded a decline in core EPS growth of 39.1 percent, which was lower than the 7.6 per cent core EPS growth recorded in 2014.

FY’2015 Listed Insurance Sector Metrics

From the table above:

- While core EPS growth was negative at (39.1%), Kenya Re still managed to report respectable double digit EPS growth as it being the national reinsurer, insurance companies are required by law to cede to Kenya Re, guaranteeing top-line growth, while keeping costs low. CIC Insurance and Jubilee’s growth was relatively flat attributed to negative growth in the underwriting business, while being cushioned by investment income growth and decline in expenses. Pan Africa, Liberty Holdings and Britam all registered significant downside growth attributed to high expense growths as they acquired new business,

- Only Liberty Holdings registered a growth in net premiums accompanied by a decline in net claims. Kenya Re and Britam both reported an increase in premiums, however their growth in claims outpaced their growth in premiums. CI C, Jubilee and Pan Africa each registered a decline in premiums and claims from the previous year, and,

- Britam was the only insurer to report a negative return on equity of negative 5%, compared to an industry average of positive 12.4%.

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory

- January 2026 (220)

- February 2026 (243)

- March 2026 (195)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)