Key Themes That Shaped The Banking Sector Performance In Q1’2022

KEY POINTS

Kenya still remains overbanked as the number of banks remains relatively high compared to the population. To bring the ratio to 5.5x, we need to reduce the number of banks from the current 38 banks to 30 banks.

KEY TAKEAWAYS

The listed banks’ management quality also improved, with the Cost to Income ratio improving by 10.4% points to 53.1%, from 63.5% recorded in Q1’2021, as banks continued to reduce their provisioning levels following the improvement business environment during the period.

The Core Earnings per Share (EPS) for the listed banks recorded a weighted growth of 37.9% in Q1’2022, from a weighted growth of 28.4% recorded in Q1’2021, mainly attributable to a 21.4% growth in non-funded income coupled with a 17.7% growth in net interest income.

Additionally, the Asset Quality for the listed banks improved in Q1’2022, with the gross NPL ratio declining by 1.0% point to 12.5%, from 13.5% in Q1’2021. Despite this improvement in the asset quality, the NPL ratio remains higher than the 10-year average of 8.1%.

The listed banks’ management quality also improved, with the Cost to Income ratio improving by 10.4% points to 53.1%, from 63.5% recorded in Q1’2021, as banks continued to reduce their provisioning levels following the improvement business environment during the period.

The themes that shaped the sector include:

Regulation of Digital Lenders

The Central Bank of Kenya (CBK) enacted the law to regulate digital lenders, granting the bank the authority to license and oversee previously unregulated digital credit providers.

The regulations were published on 18th March 2022 and allowed digital lenders a period of six months to acquire licenses from CBK. The regulations are aimed at protecting borrowers against the predatory practices of unregulated digital credit providers, particularly their high costs, unethical debt collection practices, and misuse of personal information.

“We expect the move to streamline the digital lending services sector and weed out unscrupulous digital lenders who have taken advantage of the unregulated space to violate various consumer rights and privacy,” said Cytonn.

Regional Expansion through Mergers and Acquisitions

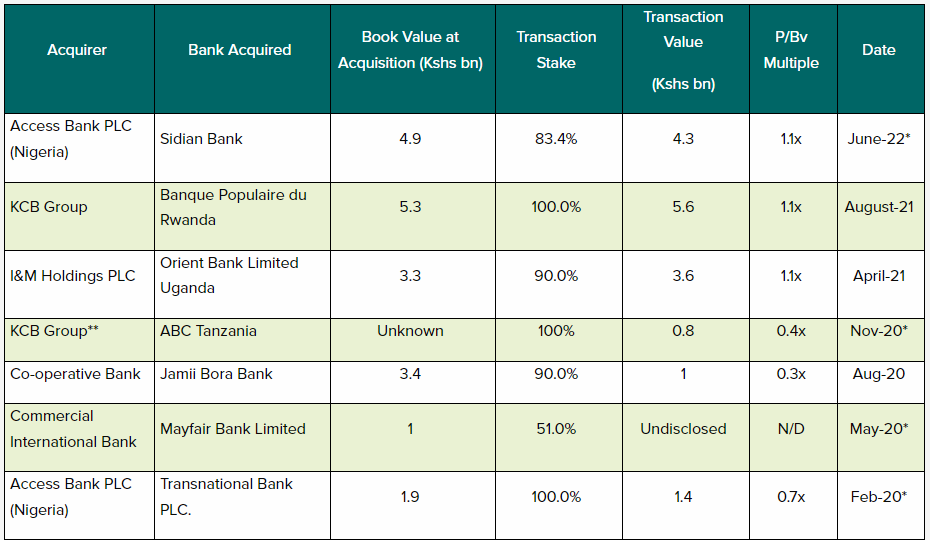

Kenyan banks are looking at having an extensive regional reach. On 8th June 2022, Centum Investment Company PLC announced that it had entered into a binding agreement to sell its 83.4% shareholding in Sidian Bank to Access Bank PLC, for consideration of Kshs 4.3 bn subject to relevant approval from the Central bank of Kenya and the Competition Authority of Kenya.

The price consideration from Access Bank translates to a Price to Book Value (P/B) of 1.1x, which is lower than the 8-year acquisitions average P/B of 1.3x, but higher than the current average P/B of the listed banking stocks of 0.9x.

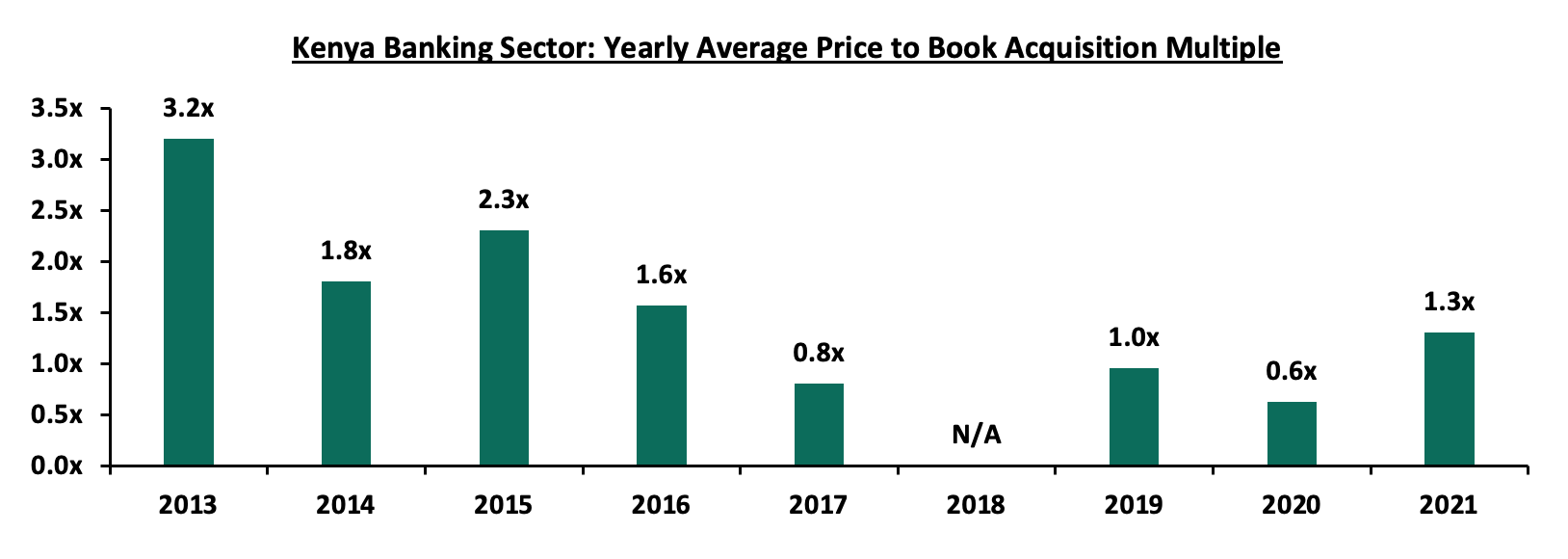

The acquisition valuations for banks have been recovering, with the valuations increasing from an average of 0.6x in 2020 to 1.3x in 2021. This however still remains low compared to historical prices paid as highlighted in the chart below;

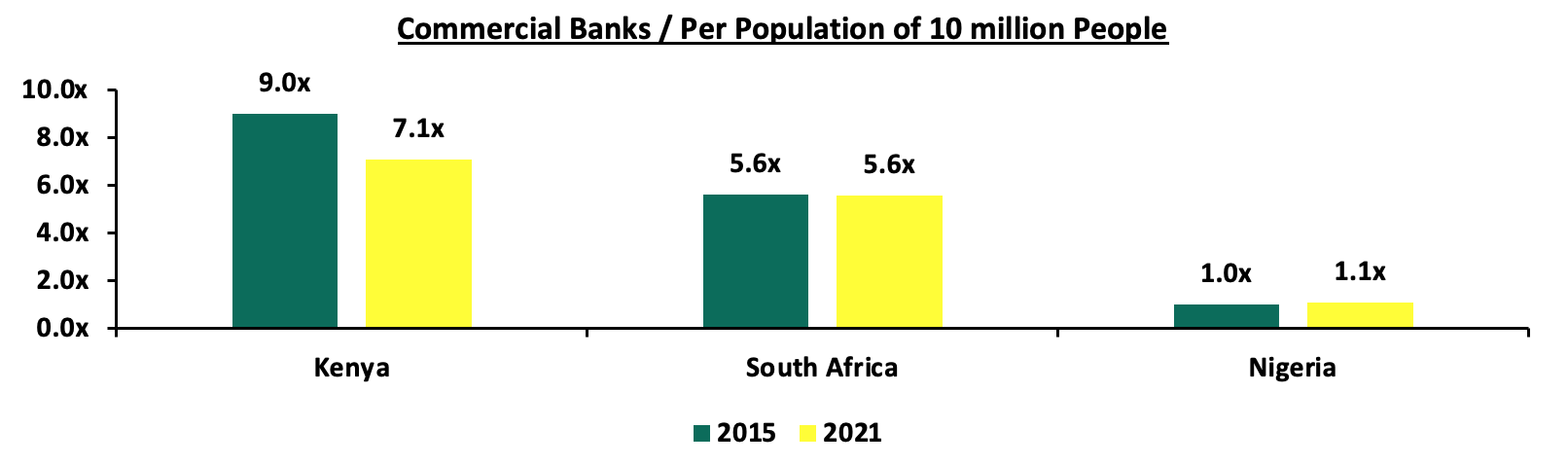

The number of commercial banks in Kenya currently stands at 38, the same as in Q1’2022 but lower than the 43 licensed banks in FY’2015.

The ratio of the number of banks per 10 million population in Kenya now stands at 7.1x, which is a reduction from 9.0x in FY’2015 demonstrating continued consolidation of the banking sector.

However, despite the ratio improving, Kenya still remains overbanked as the number of banks remains relatively high compared to the population. To bring the ratio to 5.5x, we need to reduce the number of banks from the current 38 banks to 30 banks. For more on this see our topical.

Asset Quality

Asset quality for listed banks improved in Q1’2022, with the Gross NPL ratio declining by 1.0% points to 12.5%, from 13.5% in Q1’2021.

According to the May 2022 MPC Press Release, the NPL ratio for the entire banking sector stood at 14.1% as of April 2022, relatively unchanged from April 2021, with the majority of the non-performing loans stemming from sectors like the building and construction sector, manufacturing as well as the transport and communication sectors.

Notably, the NPL ratio increased from the 13.1% recorded in December 2022 signaling a deteriorating business environment occasioned by the increased cost of living.

“We expect credit risk to remain elevated in the short term given the resurgence of COVID-19 infections as well as persistent supply constraints which are expected to continue to weigh on the business environment,” added Cytonn.

The chart below highlights the asset quality trend for the listed banks:

The table below highlights the asset quality for the listed banking sector:

Capital Raising

In Q1’2022, listed banks continued to borrow from international institutions to not only strengthen their capital position but also boost their ability to lend to the perceived riskier Micro Small and Medium-Sized Enterprises (MSMEs) segment in order to support the small businesses in the tough operating environment occasioned by the COVID-19 pandemic.

In the period under review, Equity Group received USD 165.0 mn (Kshs 18.6 bn) facility from the International Finance Corporation (IFC) to Equity Bank Kenya in January 2022 in a bid to raise capital and for onward lending to climate-smart projects and Small and Medium Enterprises (SMEs) in Kenya.

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory

- January 2026 (220)

- February 2026 (246)

- March 2026 (285)

- April 2026 (19)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)