Special Funds: Kenya’s Quiet Hidden Investment Options

For decades, Kenya’s investment landscape has been dominated by familiar names—unit trusts, money market funds, fixed deposits, and equities. Treasury bills, stock tickers, and property deals have defined what it meant to “invest.” Yet beneath this traditional noise, a quiet revolution has taken root: the rise of special funds.

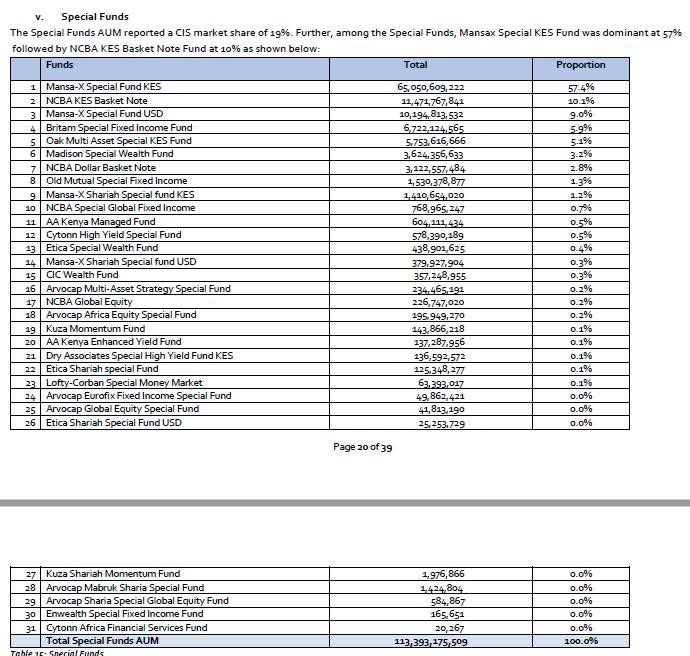

Today, special funds command 19% of the Collective Investment Schemes (CIS) market, making them impossible to ignore. At the heart of this transformation stands one fund that has reshaped investor confidence—Mansa-X Special Fund KES, which alone controls a staggering 57.4% of the special funds market.

Mansa-X is not just a leader; it is a fortress of trust. With an asset base of more than KES 65 billion, it dwarfs its competitors. The reason is straightforward: performance, consistency, and reliability. Investors in Kenya crave stability, but they also crave growth. Mansa-X provides both in equal measure.

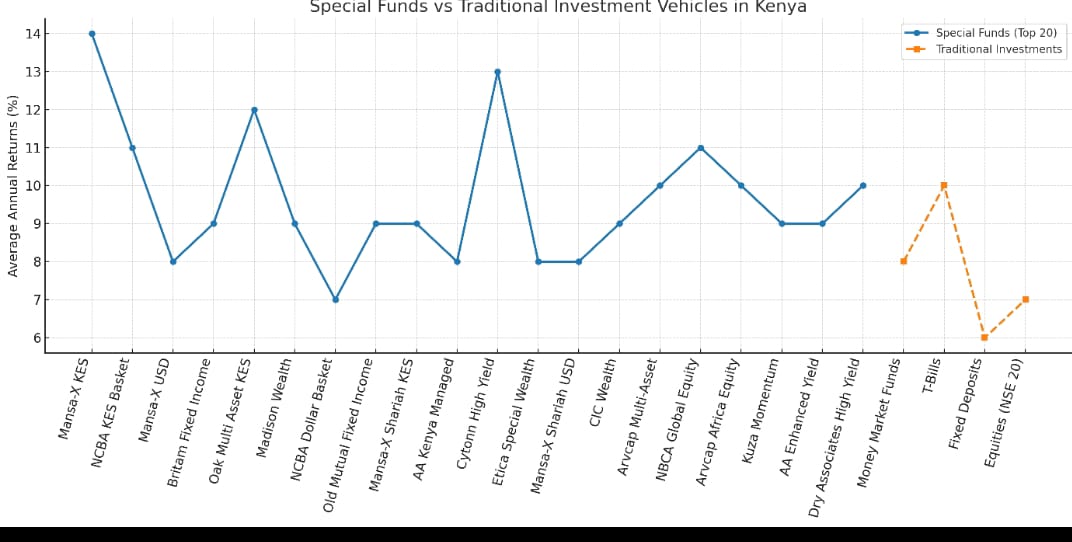

Unlike funds that simply mirror market movements, Mansa-X has carved out a track record of delivering annualized returns that consistently beat both inflation and treasury yields. Over the last three years, returns have averaged 12–15% annually, depending on market cycles. That is higher than fixed deposits, safer than equities, and more dependable than speculative instruments.

But Mansa-X is only part of the story. Close behind is the NCBA KES Basket Note Fund, which holds a 10.1% share of the special funds market. With an asset base of around KES 11.4 billion, it takes a unique “basket” approach, spreading risk across multiple fixed-income strategies. Its 10–11% annualized returns make it especially attractive to middle-class savers and corporate treasurers seeking liquidity with steady growth.

Beyond shilling-denominated products, the Mansa-X Special Fund USD has carved out an essential niche for dollar investors. With KES 10 billion in assets (9% share), it shields investors from shilling depreciation and delivers returns of 7–9% in USD terms. In a country where currency weakness is relentless, this fund doubles as both a hedge and a growth vehicle.

Read Also: Unlocking Wealth Investment Options In Kenya: Discover The Investment Haven of Kenya

Other players add depth to this ecosystem. The Britam Special Fixed Income Fund (5.9% share) appeals to conservative investors, delivering 9–10% annually—a haven for pension funds and retirees seeking predictable cash flows. The Oak Multi Asset Special KES Fund (5.1% share) mixes equities, bonds, and alternatives, generating 11–13% average returns over five years and attracting risk-tolerant investors.

Meanwhile, the Madison Special Wealth Fund (3.1% share) targets high-net-worth individuals with steady 9% returns, while the NCBA Dollar Basket Note Fund (2.8% share) provides a second dollar option averaging 7% annually. Old Mutual Special Fixed Income Fund (1.7% share) mirrors Britam’s model with 8–9% returns, preserving Old Mutual’s place among conservative investors.

Equally significant is the Mansa-X Shariah Special Fund KES, which caters to Muslim investors seeking Shariah-compliant products. With a 1.2% market share and 8–10% returns, it proves that ethical investing can compete head-to-head with conventional funds.

Together, the top 10 special funds control more than 96% of the market. Yet beneath them lies an expanding ecosystem of niche players—Cytonn High Yield, CIC Wealth, AA Kenya, Etica Special Wealth, Arvcap Multi Asset Strategy, Kuza Momentum, and others—each experimenting with unique strategies and investor profiles.

These smaller funds, while commanding tiny market shares, still play a critical role. Cytonn High Yield, for instance, targets high-risk investors with returns of 13–14%, albeit with volatility. CIC Wealth Fund delivers a safe 9%, while Etica Special Wealth Fund focuses on ethical investing. AA Kenya’s Enhanced Yield Fund, despite holding just 0.1% share, offers 9% returns and an innovative structure. Even the smallest, like Enwealth Special Fixed Income Fund, expand investor choice and foster market maturity.

The strength of special funds lies in their design. Where money market funds plateau at 8–9%, and equities swing unpredictably, special funds blend strategies to balance risk and maximize growth. In a climate of inflation, currency weakness, and rising taxes, they deliver what few others can: 10–15% structured annual returns with safety nets.

This is why Mansa-X thrives. It taps into Kenya’s psychology—deep distrust of government, hunger for growth, and demand for liquidity—and packages all three in one product. NCBA’s basket note appeals to cautious corporates, while Shariah-compliant funds serve a previously underserved market. Each product is tailored, and together they form an ecosystem of resilience.

When benchmarked against alternatives, the contrast is stark. Treasury bills average 9–10%, barely beating inflation. Equities, once the darlings of wealth creation, have flatlined, with the NSE 20 index stagnant for over a decade. Fixed deposits, yielding 5–6%, are little more than capital graveyards. By comparison, special funds compound wealth year after year.

The real revolution is not just that these funds exist—it is that Kenyans are finally waking up to them. With KES 113 billion already under management, they are forcing banks, SACCOs, and traditional fund managers to rethink their strategies. For many savers, the choice is becoming clear: snooze with fixed deposits, gamble with equities, or build steadily with special funds.

Mansa-X in particular has changed the narrative. For decades, investors believed government securities were the safest path. But by harnessing alternative strategies in forex and commodities, Mansa-X proved higher returns could be achieved safely and within regulation. Its transparency, consistency, and payouts silenced skeptics who once dismissed it as a fad.

The NCBA Basket Note Fund illustrates another evolution—the rise of structured products in Kenya. With its built-in hedges, it cushions investors against market downturns while still beating inflation. In comparison, most money market funds, though useful for short-term liquidity, fall flat for long-term growth. A million shillings parked in a top money market fund in 2015 would have grown to KES 1.9 million today. In Mansa-X, the same investment would now exceed KES 3 million.

Fixed deposits, on the other hand, remain an illusion of safety. At 5–6% returns, inflation silently erodes capital, while banks lend the same funds at 13% or more. Equities fare little better—the NSE has slumped under governance issues, foreign exits, and poor performance. Against this backdrop, special funds have emerged as the smarter, more consistent bet.

Of course, the market has not been without cautionary tales. Cytonn’s collapse, after promising 18–20% returns, left investors stranded and served as a painful reminder that governance and regulation matter more than promises. That failure, ironically, strengthened regulated players like Mansa-X and NCBA, which now wear compliance as a badge of legitimacy.

Special funds also extend Kenya’s reach globally. Offshore-linked products tied to U.S. tech stocks, oil prices, and dollar strength allow Kenyan investors to tap into cycles far beyond Nairobi. Pension schemes, once rigidly tied to government bonds, are beginning to diversify into these vehicles, outperforming peers and prompting regulatory shifts.

Read Also: As The Economy Goes Through The Doldrums; Here Are 20 Investment Options Kenyans Have In 2023

Technology has amplified this momentum. Digital platforms now allow investors to track performance in real time, withdraw instantly, and compare products transparently. This accessibility has attracted cautious professionals who once avoided financial products altogether.

Risks remain. Mansa-X is vulnerable to forex volatility, while structured products rely on derivative models that can misfire under extreme stress. Taxation is another looming concern, as the Kenya Revenue Authority eyes investment income for future levies. But unlike scams, these risks are disclosed openly, giving investors clarity before committing capital.

Despite such challenges, the momentum is irreversible. Special funds are attracting billions in new inflows every year—from middle-class savers, corporates, high-net-worth individuals, and even diaspora investors. Kenyans abroad, wary of wasted remittances, increasingly channel funds directly into these products for accountability and growth.

Perhaps the most profound shift is cultural. For decades, investment in Kenya meant land, plots, and rental apartments. But with land prices stagnating and rental yields disappointing, investors are waking up to the fact that paper assets—funds, securities, structured products—can deliver cleaner, higher, and hassle-free returns.

Ironically, real estate’s struggles have become special funds’ blessing. Every landlord frustrated by rent arrears and every plot buyer scammed by double sales becomes a potential recruit for structured products. One sector’s weakness fuels another’s rise.

In the end, the top 20 special funds are not just outperforming traditional investments—they are reshaping Kenya’s financial culture. They are forcing banks to innovate, regulators to adapt, and investors to evolve. This is not just growth—it is a financial revolution.

The sleeping giant has awakened. Kenya’s investment future belongs to special funds.

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (246)

- March 2026 (285)

- April 2026 (2)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)