Interest Capping Law Doing More Harm than Good

Despite the positive intention behind the Banking (Amendment) Act, private sector credit growth declined to an 8-year low of 1.4 percent in July 2017 according to a report released by Cytonn Investments Limited.

The decline of the credit was attributed to the fact that banks preferred, and justifiably so, not to lend to consumers or businesses but invest in risk-free Treasuries, which offer better returns on a risk-adjusted basis.

“Following the capping of the interest rates, which excludes the extra charges, most commercial banks have taken advantage of the loophole allowing them to charge extra fees on the loans issued to increase the cost of credit well above the statutory ceiling of 14.0 percent, averaging 18.0 percent, which is 3.5 percent above the 14.0 percent cap,” said the report.

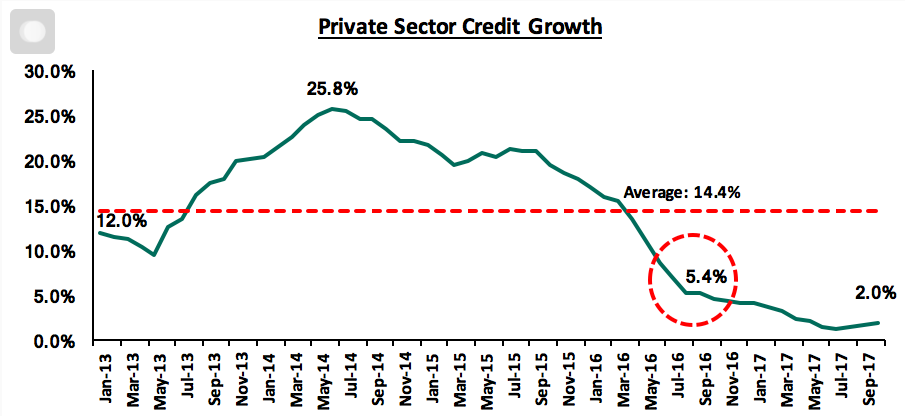

The Interest capping law appears to be doing more harm to consumers than it was previously thought. The negative impact of the introduction of interest rate caps has proved to outweigh its benefits, as credit growth has dipped compared to the pre-rate cap era, as illustrated in the graph below, which shows private sector credit growth over the last 4-years.

See the graph below:

According to the Kenya Bankers Association, loans with a 1-year duration, both secured and unsecured, should attract the maximum chargeable interest of 14.0 percent, but banks have managed to increase the true cost of credit with bank charges varying depending on the bank.

There are various costs associated with a loan in addition to the interest rate component, which ranges from bank fees and charges to third-party costs, such as insurance fees, legal fees, and government levies.

The total cost of credit is therefore defined as all costs related to the issue of credit, including interest and any fees tied to acquiring credit, usually expressed by the Annual Percentage Rate (APR), a metric that factors in additional costs and fees on the annual interest rate.

Moving to analyze the true cost of credit, below we have the ranking of the cheapest and most expensive banks, based on the APR, assuming an individual has taken up a personal secured loan, with the average APR in the sector under this category recorded at 16.7 percent, same as was recorded 6-months ago in July 2017. The two tables below show the Cheapest Banks having an average APR of 15.1 percent (same as in July 2017), with the Most Expensive Banks having an average APR of 18.7 percent (20 bps lower than 18.9% in July 2017)

According to Cytonn, these are the cheapest banks to secure a loan:

The following are the most expensive banks as far as credit is concerned:

Source: Cytonn Investments Limited weekly report

About Juma

Juma is an enthusiastic journalist who believes that journalism has power to change the world either negatively or positively depending on how one uses it.(020) 528 0222 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (243)

- March 2026 (72)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)