GA Insurance Will No Longer Insure Probox And Suzuki

KEY POINTS

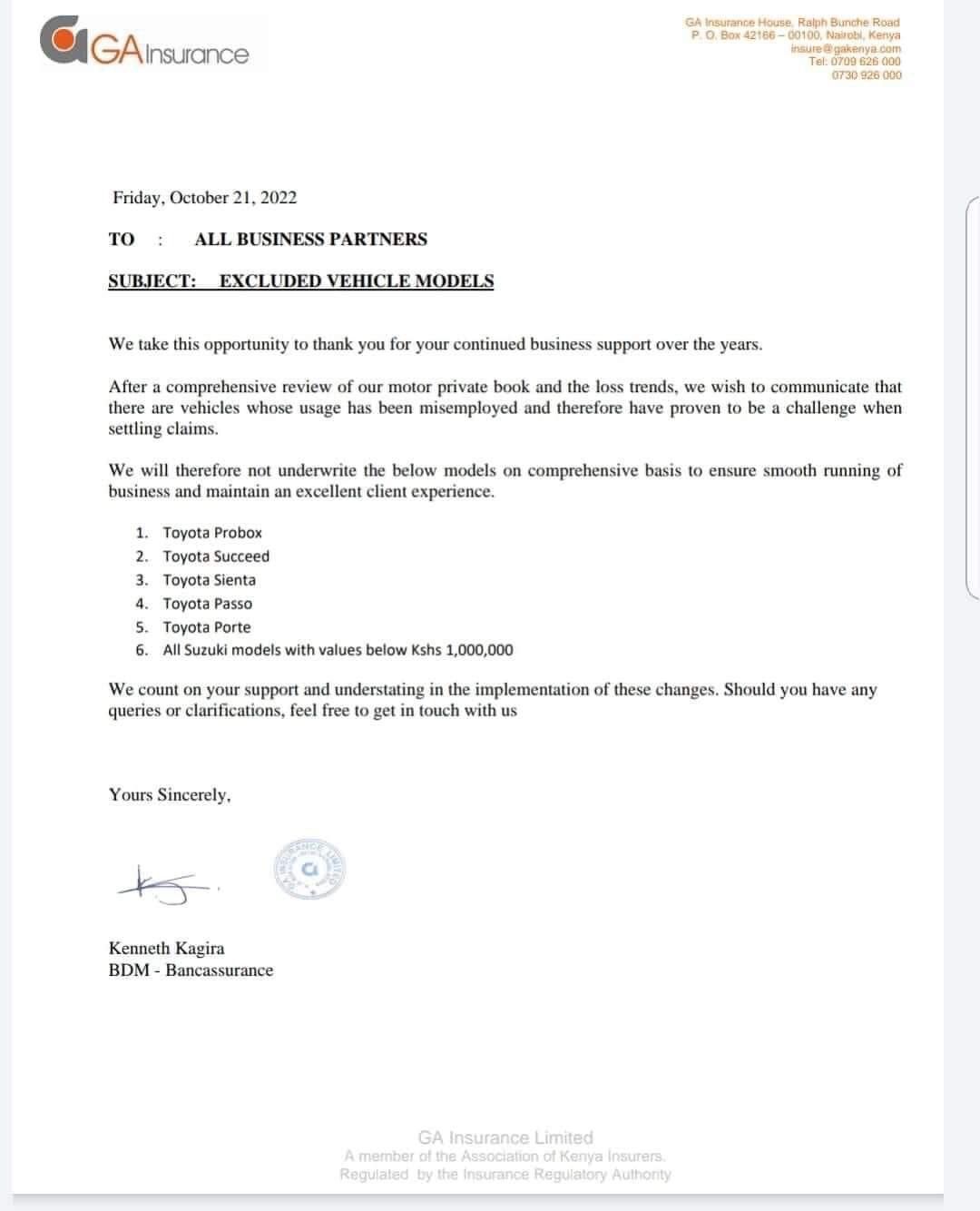

The 6 vehicle models blacklisted by the firm are Toyota Probox, Toyota Succeed, Toyota Sienta, Toyota Passo, Toyota Porte, and all Suzuki models with values below 1 million shillings.

KEY TAKEAWAYS

“Despite the constrained business environment arising from elevated inflation and global supply chain constraints, the insurance sector showcased resilience and recorded a 13.2% growth in gross premiums to Kshs 163.1 bn in H1’2022, from Kshs 144.0 bn in H1’2021."

The GA Insurance Limited has announced that moving forward it will not provide insurance services to at least 6 car models. This becomes the first insurance company in Kenya to make it clear the type of car model that it cannot cover.

The insurance company says the blacklisted vehicles are being misemployed, citing a challenge when settling claims involving them.

“After a comprehensive review of our motor private book, and the loss trends, we wish to communicate that there are vehicles whose usage has been misemployed and, therefore, have proven to be a challenge when settling claims,” said GA Insurance Business Development Manager Kenneth Kagira in a letter to all its business partners.

The 6 vehicle models blacklisted by the firm are Toyota Probox, Toyota Succeed, Toyota Sienta, Toyota Passo, Toyota Porte, and all Suzuki models with values below 1 million shillings.

Here is the statement from the insurance provider:

Insurance uptake in Kenya has remained low with the insurance penetration coming in at 2.2% as of December 2021, mainly attributable to the fact that insurance is still seen as a luxury and is mostly taken when it is necessary or a regulatory requirement.

“Despite the constrained business environment arising from elevated inflation and global supply chain constraints, the insurance sector showcased resilience and recorded a 13.2% growth in gross premiums to Kshs 163.1 bn in H1’2022, from Kshs 144.0 bn in H1’2021.

Loss and Expense Ratios across the sector eased, and consequently, the weighted average Combined Ratio improved to 126.8% in H1’2022, from 146.6% in H1’2021.

“We expect steady growth in premiums as underwriters leverage increased technology and digital distribution channels to target a larger reach. Claims are expected to grow in line with increased economic activity and insurers should leverage modern technology such as Artificial Intelligence to reduce insurance fraud and fictitious claims,” said Kevin Karobia, Investments Analyst at Cytonn Investments.

Related Content: Why Agriculture Insurance Is Vital To Kenyan Farmers

- January 2026 (220)

- February 2026 (241)

- March 2026 (36)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)