The Explainer: Safaricom Valuation Is Neither Outdated Nor Undervalued

The assertion that the government’s proposed sale of a 15 per cent stake in Safaricom is based on an “outdated valuation” risks oversimplifying what was, in reality, a rigorous, multi-layered valuation process grounded in both market practice and financial fundamentals.

Appearing before the parliamentary committee, Treasury Cabinet Secretary John Mbadi made it clear that the KSh 34 per share price was not arbitrarily arrived at, nor was it anchored on historical data alone. Rather, it emerged from a comprehensive assessment conducted using a range of widely accepted valuation methodologies, precisely the kind used by investment banks and capital market practitioners globally.

At the centre of this process was the Kenya Commercial Bank Investment Bank, which acted as the Treasury’s valuation advisor. The institution prepared a detailed valuation report incorporating several metrics that collectively paint a holistic picture of Safaricom’s worth.

These included net asset value, earnings performance, dividend flows, and discounted cash flow (DCF) analysis. Importantly, Safaricom’s status as a listed company made price discovery more transparent, allowing the valuation to be benchmarked against observable market data rather than conjecture.

The results of these individual valuation approaches are instructive. Valuation based on earnings placed Safaricom’s share value at KSh26. The price-to-earnings method yielded KSh17 per share, while the discounted cash flow analysis came in at KSh18.51.

The discounted dividend model produced a valuation of KSh23.61, and the six-month weighted average trading price stood at KSh27.50 per share. Taken together, these figures underscore a consistent valuation range well below the proposed transaction price.

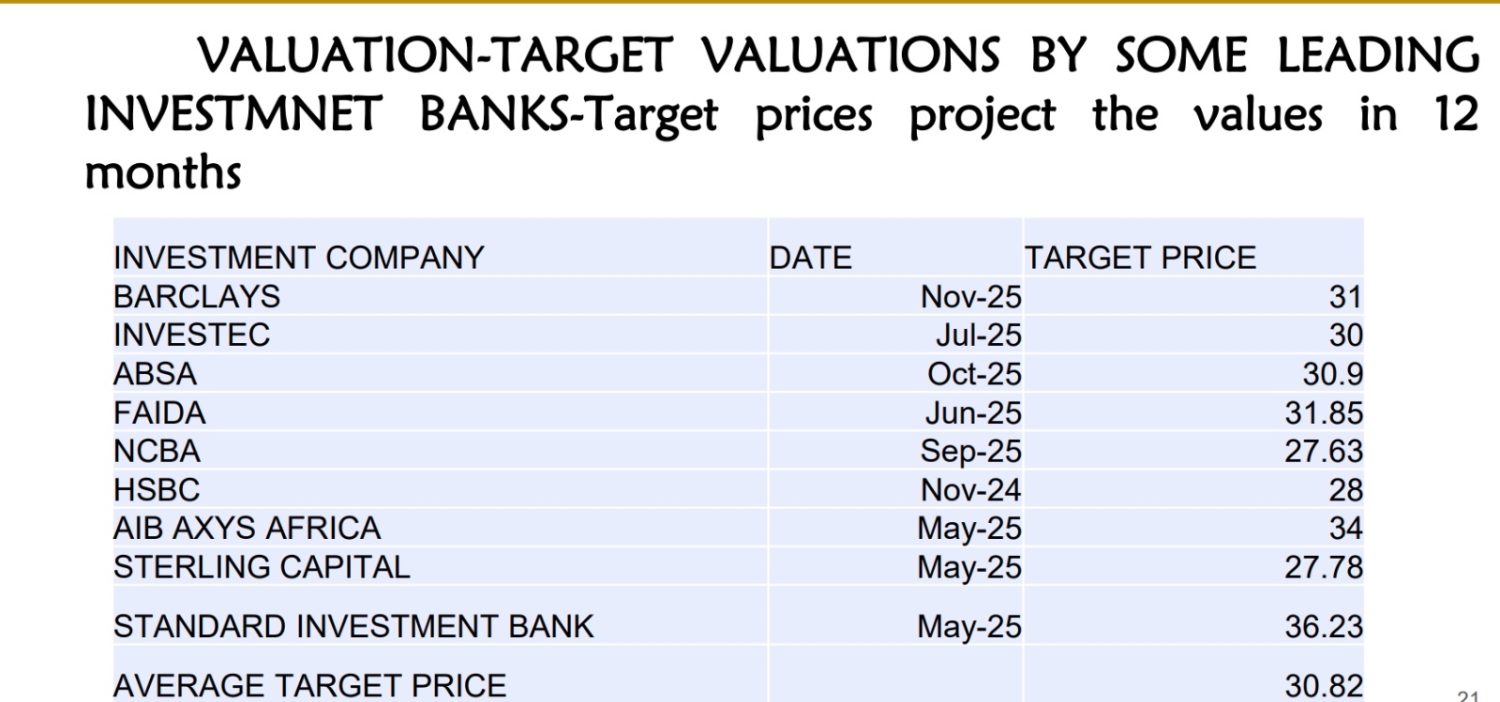

Crucially, the average valuation provided by leading investment banks, institutions whose core business is valuing, pricing, and trading equities, stood at KSh30.82 per share. These banks employ teams of highly qualified accountants, analysts, and financial modelers whose credibility rests on getting valuations right in real-market conditions. Against this backdrop, a transaction price of KSh34 per share represents not an undervaluation, but a clear premium over both market averages and fundamental valuation benchmarks.

This premium directly addresses concerns that the government is underselling a strategic national asset. Far from relying solely on historical trading data, the valuation process blended forward-looking methodologies with market-based indicators, ensuring that future earnings potential, dividend sustainability, and cash flow generation were factored into the final price.

It is also worth noting that in capital markets, valuation is not an exact science but a range-based exercise informed by assumptions, risk profiles, and prevailing market conditions. Expecting a single “perfect” price ignores the reality that even private sector transactions are concluded within negotiated ranges, often at premiums to prevailing market prices, especially where strategic stakes are involved.

In this context, the KSh34 per share price reflects a balance between market realities, professional valuation advice, and the government’s fiduciary duty to secure fair value for taxpayers. Rather than being anchored on outdated assumptions, the pricing appears firmly rooted in accepted valuation practice and supported by independent, market-facing institutions.

Ultimately, the debate should not be whether historical data was used—because all credible valuations use it- but whether it was used intelligently and in combination with forward-looking metrics. On the evidence presented to Parliament, it clearly was.

Read Also: Why Is Kenya selling 15% Stake In Safaricom To Vodacom?

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory

- January 2026 (220)

- February 2026 (243)

- March 2026 (95)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)