Commodity Prices in East Africa Stable as Most Countries Harvest Produce

Staple commodity prices in the East African region, especially for maize, are expected to remain above last year and five-year average prices despite the current average harvest

This, in turn, is expected to hence the prospects and actual imports of maize from different countries in the region into Kenya so as to moderate the expected rise in staple grain commodity

In the month of November, regional cross-border trade in maize declined typically from the previous second quarter as fresh supplies started entering most markets across the region.

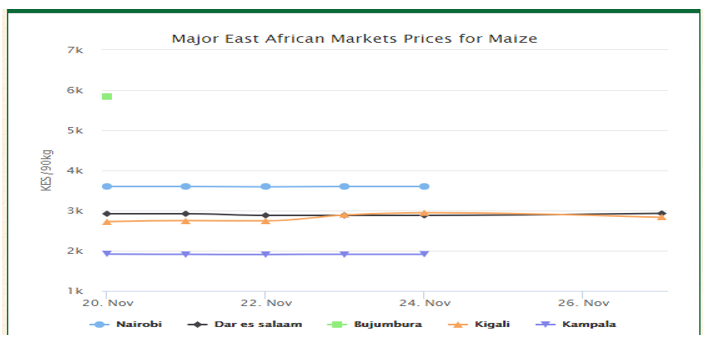

On Monday, different towns in the East African countries showcased different retail and wholesale market prices for a 90-kilogram bag of maize.

In Kenya, the prices are as follows: 3.500 shillings in Malindi, 3,400 shillings in Nairobi, 3,000 shillings in Mombasa, 3,200 shillings in Kisumu, 2,500 shillings in Nakuru and Eldoret respectively and 2,400 shillings in Kitale.

The table below gives maize prices for different towns in some of the East Africa countries:

Availability of sorghum in the region is still high because of high carryover stocks from the previous above average harvest in Uganda.

Sorghum prices in most of the reference East African markets declined or remained stable seasonably following increased supply from the recent harvest and or imminent start of the October to-January harvest.

In Kenya, the prices for a 90-kilogram bag of Sorghum are as follows: 7,200 shillings in Eldoret, 6,000 shillings in Malindi, 5,200 shillings in Nairobi, 4,800 shillings in Kisumu and 3,600 shillings in Mombasa and Nauru respectively.

Sorghum prices in Uganda and especially in Kampala, are the ones trending below the regional average which is attributed to a better harvest. The table below shows more for the same:

Ngozi, in Burundi has the highest retail market prices for a 90-kilogram bag of Wheat at 8,435 shillings with Mombasa, Kenya having the least market price of 2,700 shillings.

The whole sale prices were as follows in different towns of the East African countries: 7,447 shillings in Ngozi, Burundi, 6,208 shillings in Kimironko, Rwanda, 3,587 shillings in Mbeya, Tanzania.

Here is a summary of the same:

Local rice production in Tanzania is currently average, but the carryover stocks are low because of high consumption in the previous marketing year as maize prices increased exceptionally.

The prices are expected to trend seasonably but will likely be moderated by increased demand for maize flour has the price for this substitute commodity is trending lower than that of rice.

The total cross-border trade in dry beans (86,500 MT) was 31 percent above the four-average for the July-to-September third quarter because of good performance of the May-to-August rains at the beginning of the season which was enough for most of the short maturing dry bean crop, although the overall rainfall performance was poor for the long cycle grain crops especially in main producing Uganda, Rwanda, and Ethiopia.

Dry bean trade in the region has been enhanced by increased demand. Kenya has accounted for 64 percent of regional dry bean imports. Dry bean exports from Uganda and Ethiopia to other regional markets have been 24 and 27 percent above the third quarter average as a result of seasonal increased demand in the structural deficit countries of South Sudan and Kenya. The demand was heightened by poor rainfall performance in Kenya.

Dry bean prices have declined seasonably in the reference markets of Nairobi (Kenya), Kigali (Rwanda) and Dar es Salaam (Tanzania) because of increased domestic and regional supplies. In the source markets of Rwanda and Uganda, the prices are increasing gradually but typically in the third quarter attributed to increased domestic and regional demand.

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (278)

- August 2026 (38)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)