Timiza Beats All Others To Emerge As The Cheapest Short-Term Loan Facility In Kenya

KEY POINTS

Before the 20 percent excise duty, Timiza would charge 6.083 percent as the total cost of credit. Vooma was charging 5.91 percent (they were the cheapest then), KCB M-Pesa was charging 7.35 percent while M-Shwari was charging 7.5 percent.

When shopping for a digital or mobile loan, most Kenyans would look at a litany of things among them; the interest rate, terms and conditions (accessibility), disbursement time, and convenience in terms of payment duration.

Most mobile loan providers in Kenya have been termed beyond reach for the majority of Kenya due to high-interest rates, and information needed that goes beyond the data protection requirements. Most take up to a month for one to pay back, while some require someone to pay back as soon as within seven days.

In what was described as making loans more expensive for Kenyans, an amendment to the Excise Duty Act contained in the 2021 Finance Act effected a 20 percent duty charge to fees and commissions on loans, a change which took effect on July 1.

The 20 percent excise duty on loans has sent millions of Kenyans back to the drawing board as they hunt for more affordable loans. This is because some service providers have decided to cash in using the excise duty as an excuse.

We have analyzed the top four mobile lenders in Kenya and what they are offering their customers in terms of the interest rates after the 20 percent excise duty took effect. Where should you shop for your next mobile loan?

Timiza mobile loan facility by Absa Bank Kenya is the cheapest short-term loan in Kenya right now compared to the peers with the excise duty included. The top position was initially held by Vooma that is under the KCB Bank.

Others running after Timiza in terms of affordability are KCB M-Pesa and M-Shwari. This piece will use these four players (Timiza, Vooma, KCB M-Pesa, and M-Shwari) to compare the rates but will leave the choice of judging to where to go to you.

Before the 20 percent excise duty, Timiza would charge 6.083 percent as the total cost of credit. Vooma was charging 5.91 percent (they were the cheapest then), KCB M-Pesa was charging 7.35 percent while M-Shwari was charging 7.5 percent.

After the effecting of 20 percent excise duty, Timiza overtook Vooma and now is charging 7.083 percent while Vooma is charging 7.91 percent for 30 days. KCB M-Pesa is now charging 8.64 percent while M-Shwari is charging 9 percent.

Assume you need a loan of 10,000 shillings. For Timiza, you will be charged 708.3 shillings, Vooma will charge you 791 shillings while KCB M-Pesa will charge you 864 shillings. M-Shwari will charge you 900 shillings. Where will you go for a loan?

Of the four players, why should you go to Timiza? I have gone through all the features offered by the four players and I dare say Timiza is worth giving it a shot and here is why:

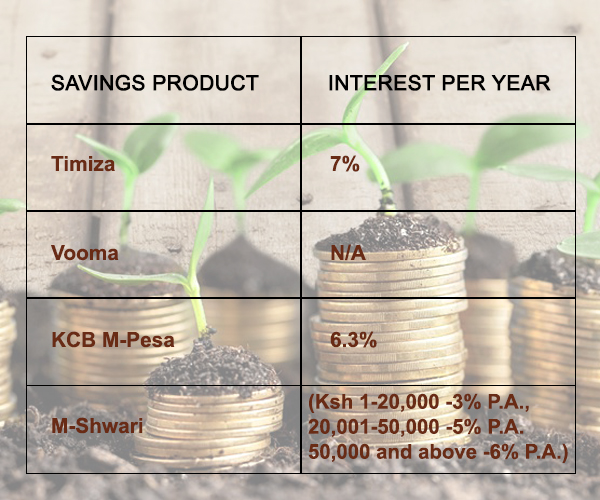

The rate. As explained above, their interest rate is currently the cheapest in the market. At 7.083 percent and you are home and dry. It also offers an exclusive savings account. Timiza is a great platform for saving, giving up to 7 percent on savings. This is higher than the other players.

Talking of interest you can earn on savings, here is a table of comparative interest rates between the major players:

Comparative limits also make Timiza the best platform to get the loan from. For Timiza, the average limit goes up to 10,000 shillings. M-Shwari, the average limit is about 4,500 shillings. With the comparative average limits, Timiza also comes with frequent lump-sum credit reviews based on a limit of consumption by the client.

The platform also comes with other auxiliary services such as bill payments that include and are not limited to DStv, KPLC, and Nairobi Water. It also enables cab services in partnership with Little Cab. Of importance, it provides insurances services for personal accidents among others.

About Juma

Juma is an enthusiastic journalist who believes that journalism has power to change the world either negatively or positively depending on how one uses it.(020) 528 0222 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (246)

- March 2026 (286)

- April 2026 (109)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)