Sub-Saharan Economic Growth Projected To Rise To 4.0%

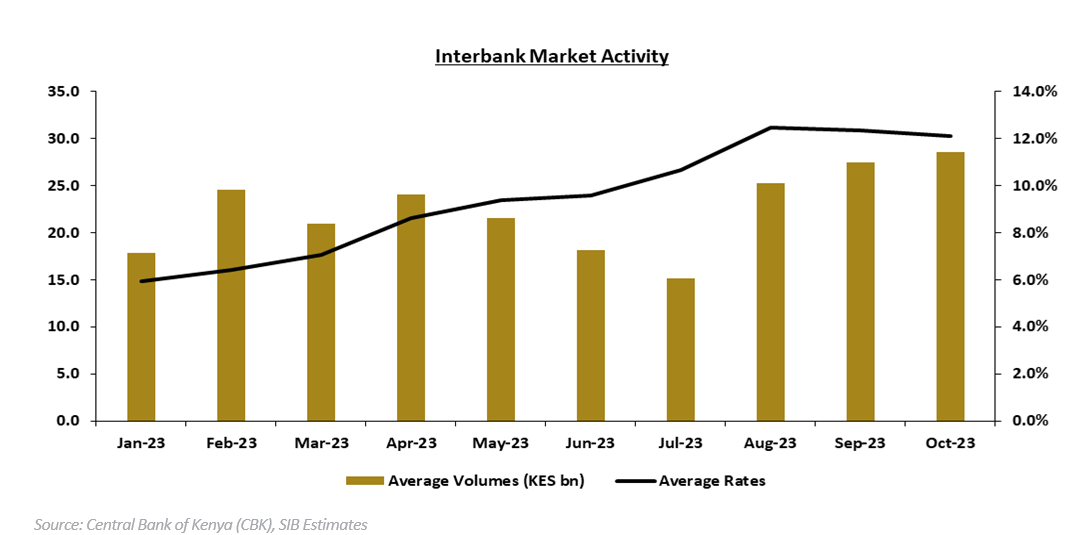

During the week, liquidity in the money market exhibited stability, as the average interbank rate remained predominantly constant at 12.10%. In parallel, the average traded volumes witnessed an increase of 16.36%, ascending to KES 31.0bn, from the previous week’s KES 26.65bn.

The Central Bank remained supportive of liquidity-strapped entities, injecting KES 40.0bn worth of liquidity through a 7-day reverse repo purchase at a rate of 12.79%.

The chart below depicts interbank rates and traded volumes, providing a snapshot of the state of the interbank market. We observe that the interbank rates have been highly volatile over the past months, fluctuating within a band of 5.0% and 17.0%.

Read Also: Fueling The Economy’s Engine: The Revenue Authority’s Impact

Fueling The Economy’s Engine: The Revenue Authority’s Impact

While there has been a noticeable decrease in trading activity in July, it appears to have revived in the last three months to October:

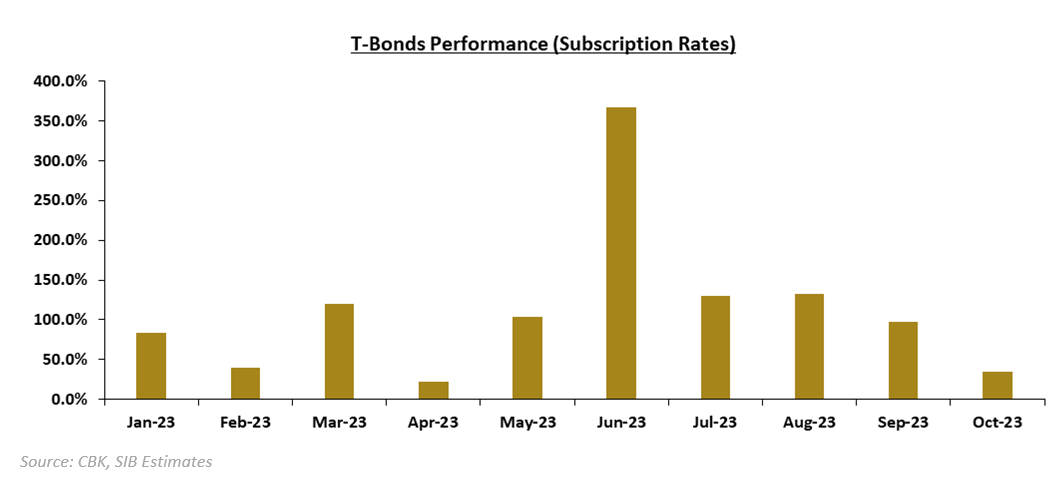

Also during the week, demand for Treasury bills surged, with the Central Bank receiving an impressive total of KES 43.24bn in bids. This exceeded the projected weekly target of KES 24.0bn, resulting in an overall subscription rate of 180.15%, up from 138.11% the previous week.

Read Also: The Role Of Digital Transformation In Creating An Economy On Supersonics

On the contrary, the performance of October bonds in the primary market was relatively subdued, attracting limited interest with a subscription rate of 35.1%.

The auction raised a total of KES 6.31bn with the shorter-tenor FXD1/2023/02 recording the highest acceptance rate of 74.16%. The papers’ coupon rates are 16.97% and 16.84% for FXD1/2023/02 and FXD1/2023/05, respectively.

We observe that October’s primary market bond performance is the lowest since April, reflecting the tightened liquidity in the money market.

Read Also: Safaricom PLC: The Pulse Of the Kenyan Economy And The Ideal Stock For Retail Investors

Furthermore, investors have exhibited a discernible shift towards Treasury Bills, primarily driven by their offering of attractive real returns relative to their tenor. See the chart below for a visual representation;

The International Monetary Fund (IMF), published the October 2023 Sub-Saharan Regional Economic Outlook, dubbed ‘Light on the Horizon?’. One of the key highlights is that the Sub-Saharan African (SSA) economic growth is projected to decline for the second consecutive year, dropping to 3.3% in 2023 from the 4.0% recorded in 2022.

There is optimism for a rebound in 2024, with growth anticipated to reach 4.0%, largely driven by strong economic performances in countries that are not heavily reliant on natural resources. Nonetheless, various risks persist, including the possibility of growth deceleration due to a slowdown in reform efforts, increasing political instability within the region, and external risks, notably stemming from China’s economic deceleration.

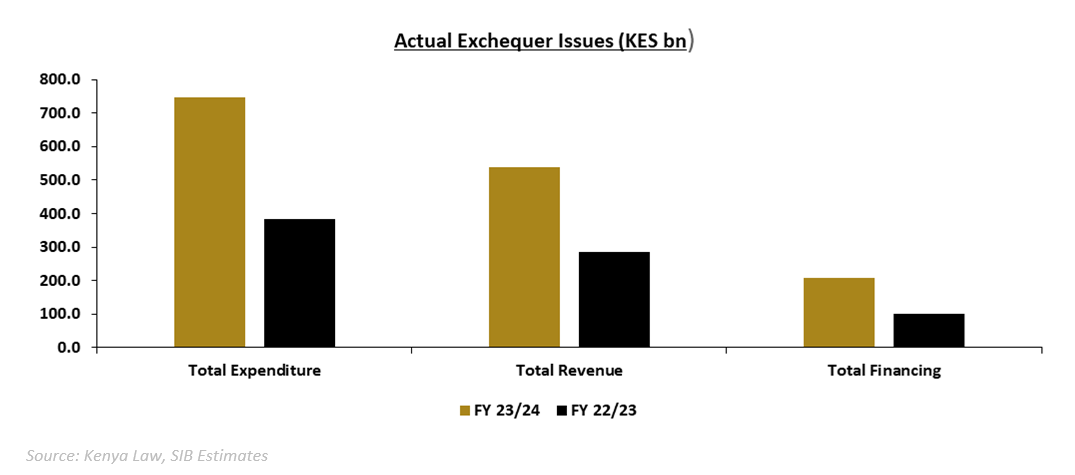

In addition, the National Treasury released the exchequer issues for the first quarter of FY 2023/24 highlighting that the total revenues collected increased by 10.70% to KES 537.35bn, from KES 485.40 bn over a similar period in FY 22/23. Tax revenues came in at KES 514.26bn, a 10.55% increase from KES 465.20bn for the first three months of FY 22/23.

Read Also: Kenyan Economy Expanded By 5.4% In 2Q23 Thanks To Agriculture

On the other hand, expenditure increased at a slower rate of 9.79% to KES 745.80bn, from KES 679.29bn over the review period. The deficit was funded by external and domestic borrowings of KES 208.01bn, which also increased by 6.52% from KES 195.28bn in FY 22/23. See the chart below for a summary of the y/y growth;

Read Also: Kenya’s Private Sector Economy Signals An Improvement On Increased Purchasing Activity

- January 2026 (220)

- February 2026 (246)

- March 2026 (286)

- April 2026 (207)

- May 2026 (32)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (219)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (293)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)