Money Market Funds Should Be Marketed As Saving Products, NOT Investment Options

Money market funds in Kenya have quietly transformed from niche capital market products into the most powerful savings engines in the country, yet they are still largely marketed as “investments” rather than what they really are for most people: flexible, high-yield savings schemes that directly challenge banks for customer deposits. Framing them as savings, not speculation, is the missing narrative that will finally give banks a serious run for their money and unlock a genuine national savings revolution.

For the average Kenyan, the word “investment” carries images of risk, loss, and stories of friends who were wiped out in fake forex, crypto, and real estate schemes. By contrast, “savings” feels safe, familiar, and purposeful: money for school fees, emergencies, rent, and future projects. Kenyan money market funds (MMFs) sit squarely in the middle of these two worlds—technically investments, but operationally and psychologically better suited to be sold as upgraded savings accounts with superior returns, daily compounding, and near-instant liquidity.

The numbers already prove that Kenyans are voting with their wallets. According to CMA’s Q1 2025 data, total assets under management in Collective Investment Schemes hit about KES 496.2 billion, with money market funds accounting for roughly KES 319.7 billion—about 64.4 percent of the entire industry and around 2.0 percent of GDP. This is up from about KES 171.2 billion and 67.4 percent of CIS AUM as at June 2024, showing that MMFs are sucking in cash faster than any other formal savings vehicle in Kenya.

Drilling down into the top 20 MMFs by size makes the story even clearer. CMA data summarised by Nyongesa Sande shows CIC Money Market Fund leading with KES 68.4 billion, followed by Sanlam at KES 50.5 billion, ICEA Lion at KES 17.9 billion, Absa Shilling Fund at KES 13.0 billion, Old Mutual at KES 12.1 billion, Co-op at KES 12.0 billion, and then a long tail of Britam, KCB, Jubilee, Etica, Madison, Nabo, Dry Associates, Lofty Corban, Apollo, GenAfrica, Ziidi, Stanbic, Cytonn, and Kuza. This is not speculative equity money; this is salary money, rent money, cash-flow money.

When you look at those top 20 funds as a consolidated balance sheet, you are essentially staring at an alternative savings “megabank”, with hundreds of billions parked in short-term government securities and fixed deposits, earning returns and flowing in and out daily. In fact, Cytonn’s Q1 2025 report shows that while Unit Trust Funds AUM grew 27.5 percent quarter-on-quarter, listed banks’ deposits shrank by 0.2 percent over the same period. That is a quiet deposit migration from banks to MMFs that only makes sense if investors are treating them as better savings accounts, not speculative bets.

Read Also: Liquidity Conditions In The Money Market: A Stable Start To The Year

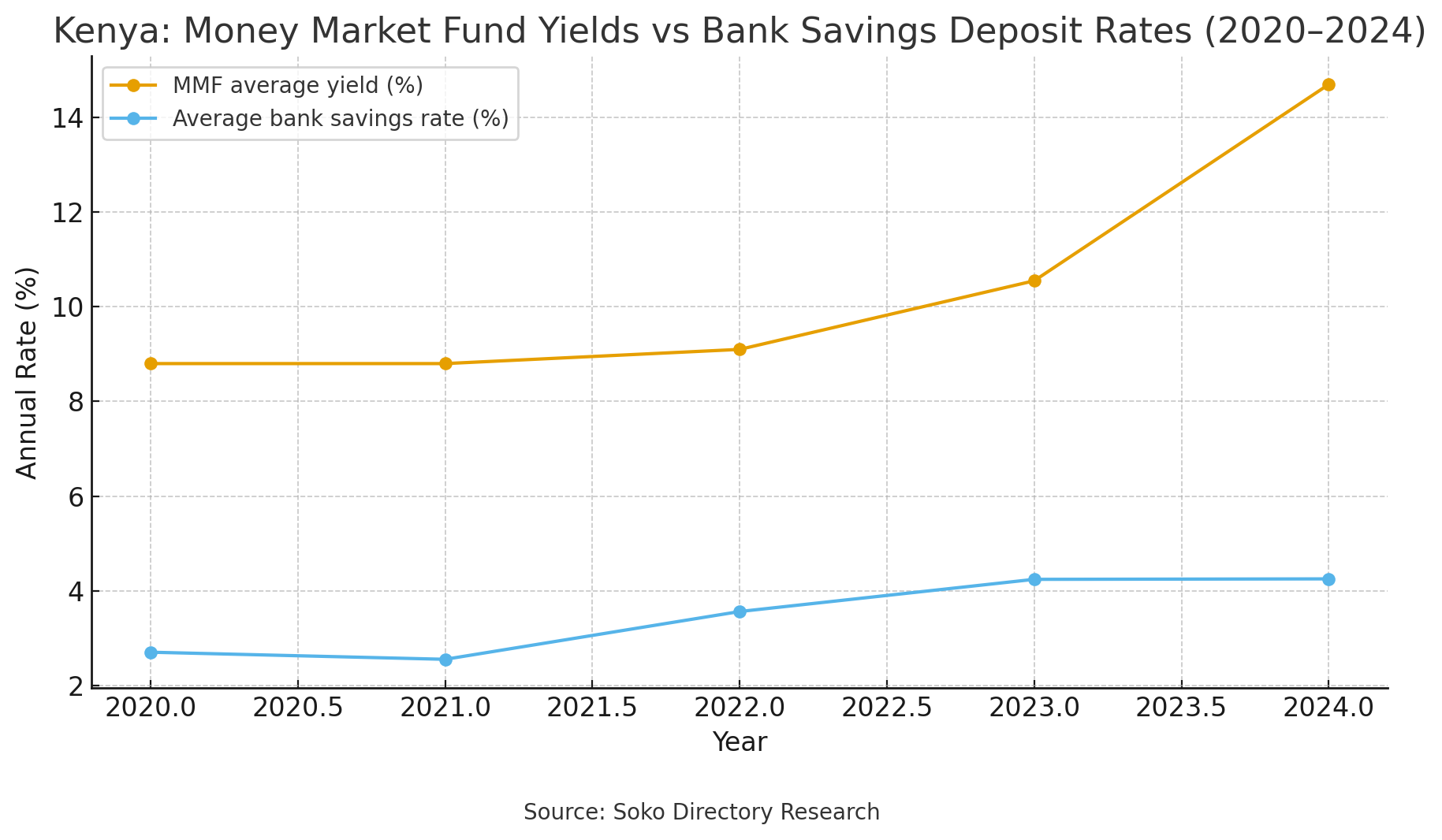

The yield gap alone makes the case for rebranding them as savings schemes. The same Cytonn report notes that in April 2025, the weighted average deposit rate in commercial banks was about 8.9 percent, while the industry average money market fund yield stood at 12.4 percent and the 91-day T-bill at about 9.0 percent. In other words, MMFs are paying roughly three to four percentage points more than bank deposits for essentially the same underlying risk—short-term government paper and term deposits in the same banks. Calling that an “investment” instead of a “super-saver account” is a marketing own goal.

If you move from averages to specific funds, the story is even more brutal for banks. In Q1 2025, Cytonn estimates the top five MMFs (Gulfcap, Cytonn, Lofty Corban, Etica, Kuza) delivered average effective annual rates of about 15.1 percent, versus an industry average of 12.4 percent. Vasil Africa’s July and September 2025 performance wraps show net annualised returns for leaders such as Gulfcap, Cytonn, Nabo, Lofty Corban, Etica, and Kuza still hovering in the 9.5–11 percent range even after tax. Compare that to many savings accounts at big banks still paying between 0.5 and 4.25 percent, with only a few specialised savers’ products touching 7.5 percent under strict conditions.

Now imagine a five-year linear graph plotting two lines: one representing the average MMF yield and the other the average bank savings/deposit rate from 2020 to 2025. Using CBK and Cytonn data, MMF yields have tended to oscillate around 8–12 percent while deposit rates have stayed in the lower band, mostly 6–9 percent and often below 7 percent in earlier years. The MMF line sits stubbornly above the deposit line almost the entire time, widening especially as investors flee low-yield bank products into CIS. That graph is not merely a picture of “investment performance”; it is a visual indictment of how poorly banks reward Kenyan savers relative to what is safely possible.

Reframing that graph as “Kenya’s real savings rates: banks vs money market funds” would change the national conversation. Instead of telling Kenyans “here is a risky investment that might beat the bank”, the message should be “here is a better savings home for your emergency fund, your chama float, your business cash, and your personal goals, with the same safety profile you already trust in government securities and licensed commercial banks—but with returns aligned to real inflation and opportunity cost.” That single reframing would resonate with the millions of Kenyans who are risk-averse but deeply frustrated with bank charges and low interest.

Importantly, Kenyan regulation already treats MMFs in a way that makes them closer to savings than to high-risk investments. CMA’s Collective Investment Schemes Regulations 2023 cap the weighted average tenor of MMF portfolios at 18 months and restrict holdings to short-term, interest-bearing securities like Treasury bills, call deposits, commercial paper, and fixed deposits with CBK-approved institutions. This means fund managers cannot chase exotic assets or long-duration bonds with huge price swings; they must preserve capital, maintain liquidity, and pay out interest. That is textbook savings behaviour, just executed through capital markets.

If we go back to the top 20 AUM table and read it not as a league table but as a “savings map”, we see and feel the breadth of this new savings ecosystem. CIC and Sanlam are the giants; ICEA, Absa, Old Mutual, Co-op, Britam, KCB, Jubilee, and Madison form a powerful middle class, while newer, more agile players like Etica, Nabo, Dry Associates, Lofty Corban, Ziidi, Stanbic, Cytonn, and Kuza are nibbling aggressively at the edges of traditional banking. If even a portion of these managers start branding their funds as “smart savings accounts” anchored on MMFs, bank deposit growth could stagnate further.

The best example of MMFs as mass savings is Safaricom’s Ziidi Money Market Fund. Approved by CMA in late 2024 and plugged directly into M-Pesa, Ziidi moved from around KES 1.7 billion AUM in Q4 2024 to about KES 7.4 billion by Q1 2025, a staggering 330.5 percent growth in just one quarter. More recent reporting shows Ziidi past the KES 15.1 billion mark with over a million active investors, capturing nearly half of all unit trust investors in Kenya within a year and drawing contributions from as low as KES 100 fully via mobile. That is not an “investment market”; that is a savings revolution unfolding inside people’s phones.

Ziidi succeeded not because it pitched itself like a stock market fund, but because it integrated into familiar savings behaviour: M-Pesa balances, Fuliza repayments, small business floats, “mpesa ya mama mboga”. When a kiosk owner shifts KES 500 from an M-Pesa wallet into Ziidi, they are not thinking like a Wall Street trader; they are thinking like a saver trying to earn something better than zero on idle cash. Labelling this behaviour as “investment” muddies the message; positioning MMFs as the natural next step after an M-Pesa or bank savings balance makes far more intuitive sense.

There is another behavioural reason to stop insisting that MMFs are “investments” first: the expectation of volatility. Equity investors expect that some months will be down and some up. But MMF investors, in Kenya’s context, are used to smooth, daily interest accruals that rarely reverse. As long as the underlying securities are held to maturity and credit risk is tightly managed, unit prices remain remarkably stable. Cytonn and other market trackers have noted that even as interest rates and inflation shifted, MMFs behaved like enhanced savings accounts: capital preserved, yield adjusted, liquidity intact. That experience is closer to “savings” than to classic “investing”.

Marketing MMFs primarily as investments also has a perverse effect: it keeps the most vulnerable savers out. The low-income Kenyan who has lost money in pyramid schemes or unregulated online products will likely resist “investments” forever—yet this is the very person who could benefit most from an 8–12 percent annualised return on their small but persistent savings. By calling MMFs “regulated savings schemes that invest in government securities on your behalf”, the industry lowers the psychological barrier and makes it easier for households to move step by step from under their mattress to M-Pesa to MMFs.

From a macroeconomic perspective, Kenya’s MMF expansion is already reshaping the savings landscape, but it is still in its infancy compared to global peers. Kenya’s MMF AUM-to-GDP ratio of about 2.0 percent in Q1 2025 is far below the global average of around 8.8 percent and drastically lower than markets like the US, where MMF AUM exceeds 20 percent of GDP. That gap is not a curse; it is an opportunity. Reframing MMFs as the nation’s default savings rail could multiply their AUM several-fold, pushing savings rates up without new taxes or heavy-handed policy.

To understand the power of this shift, consider a typical Nairobi worker earning KES 80,000 a month. If she saves KES 10,000 per month in a bank account yielding 3 percent, after five years, she will have contributed KES 600,000 and earned roughly KES 47,000 in interest. If she instead channels the same amount into a conservative MMF averaging 11 percent net, her interest could easily cross KES 200,000 over the same period, depending on compounding and tax treatment—a difference that buys a plot, pays a semester of university, or seeds a side hustle. Multiply that gap across millions of savers and you get a structural shift in household wealth.

Banks, of course, will protest that MMFs are “stealing” their deposits, but that is a lazy argument. Banks still control the payments infrastructure, current accounts, loans, and a significant portion of term deposits. What MMFs are doing is disciplining banks by forcing them to pay savers more fairly or risk losing cheap funding. The Cytonn data showing UTF AUM growing 27.5 percent while listed banks’ deposits decline in Q1 2025 is a clear signal: savers will walk where they are respected. In a competitive, mature financial system, banks and MMFs should coexist, with MMFs owning savings and banks specialising in credit and transactions.

Positioning MMFs as savings schemes also aligns perfectly with the Kenyan government’s own narrative about boosting the savings rate and building long-term pools of patient capital. As policymakers pursue sovereign wealth and infrastructure funds and seek to deepen domestic capital markets, they need citizens to channel small surpluses into regulated, pooled vehicles rather than unregulated schemes. MMFs are the lowest hanging fruit because their risk profile is close to bank deposits, but their asset allocation nudges the economy toward capital markets funding and away from short-term consumption.

The digital layer is the final piece that makes rebranding inevitable. Safaricom’s Ziidi, bank app–based funds from NCBA, KCB, Co-op, I&M, and others, plus USSD and web portals from independent managers, mean that opening, topping, and redeeming MMF units is now as simple as moving money between mobile wallets. When the user experience mimics mobile savings, the language should follow. Call these products “smart savers”, “goal-based savings plans”, or “digital savings funds”, with the MMF engine under the hood, mentioned second, not first. The majority of Kenyans care more about safety, withdrawal time, and daily interest than about the names of underlying instruments.

One potential concern with marketing MMFs as savings is the risk of complacency about underlying credit and liquidity risks. This is where regulators and fund managers must elevate transparency, diversification, and risk management. CMA’s restrictions on asset tenor and composition already provide a strong safety framework, but managers should go further by publishing simplified fact sheets showing what proportion of the fund is in T-bills, term deposits, and other instruments, and what historical daily unit price volatility looks like. Honest disclosure will ensure that savers understand that while MMFs are low-risk, they are not legally guaranteed like insured deposits.

We also cannot ignore the role of taxation and fees in cementing MMFs as superior savings. Many Kenyan savers suffer a double hit in banks: low interest plus multiple ledger, transaction, and SMS fees that quietly eat into returns. MMFs typically charge a single management fee netted off before quoting the gross or net yield, making the cost structure more transparent. Cytonn’s data shows that even after management fees, top MMFs delivered net annualised returns above 10 percent in 2025, far outstripping typical bank savings rates even before charges. A national financial education push should explicitly compare “effective net yield” between MMFs and bank savings over five years using linear graphs that show cumulative balances, not just annual percentages.

From a policy standpoint, there is a strong argument for integrating MMFs into payroll, government cash management, and social protection programmes as the default savings leg. Employers could offer staff the option to auto-sweep a portion of salary into licensed MMFs, while NGOs and government cash transfers could default to MMF-linked wallets rather than dormant bank accounts. Corporate treasurers are already using MMFs to optimise short-term cash, as recent Business Daily commentary notes, but households remain underserved. Treating MMFs as savings would accelerate their adoption in exactly these mass-market contexts.

The narrative shift also protects Kenyans from dangerous, unregulated products masquerading as “investments”. When financial literacy campaigns emphasise that “for safe, short-term savings above KES 1,000, your default should be a CMA-licensed money market fund, not a WhatsApp group promising 30 percent a month”, you redirect savings flows into regulated channels and starve scammers of oxygen. Every shilling that moves from dubious online schemes to a regulated MMF is a shilling that remains in the formal economy and can be recycled into Treasury bills and real-sector lending.

For platforms like Soko Directory, this is a golden content and advocacy opportunity. Articles, explainer videos, podcasts, and interactive calculators can show Kenyans exactly how much they lose by leaving money in current or low-interest savings accounts compared to MMFs over five, ten, or fifteen years. SEO-optimised pieces titled “Best Savings Scheme in Kenya: Why Money Market Funds Beat Bank Accounts” will not just pull traffic; they will shift behaviour. Embedding linear graphs of deposit rates vs MMF yields vs 91-day T-bill over time, and tables comparing the top 20 funds by AUM and return, will make the argument unanswerable.

Ultimately, the question is simple: what do Kenyans want their money to do while they sleep? For most people, the answer is not “beat the NSE 20 by 15 percent” but “be safe, accessible, and grow faster than inflation”. On those metrics, money market funds in Kenya already win. They pool savings, invest in short-term government and bank instruments, pay daily interest, and allow redemptions within 24–72 hours. That’s a savings scheme by any reasonable definition. Calling it an investment may please regulators and brochures, but it doesn’t reflect how ordinary Kenyans actually use these products—or what they really need from them.

If the industry, regulators, media, and influencers embrace the language of “savings” rather than “investments” for MMFs, banks will be forced into the uncomfortable but healthy position of competing for deposits on price and service, not just inertia and switching costs. That competition will flush out lazy balance sheets, reduce abusive fees, and push banks to specialise where they add real value: credit underwriting, transaction processing, and complex corporate finance. Meanwhile, MMFs will continue building a parallel savings infrastructure—transparent, digital, and performance-driven—anchored securely in Kenya’s own government paper and financial system.

For the Kenyan saver reading this on sokodirectory.com, the next step is not theoretical. Open your banking app, look at the effective annual return on your savings account for the last twelve months, then check the published net yield of a reputable money market fund from the top 20 list—CIC, Sanlam, ICEA, Absa, Old Mutual, Co-op, Britam, KCB, Jubilee, Etica, Madison, Nabo, Dry Associates, Lofty Corban, Ziidi, Stanbic, Cytonn, Kuza and others.

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (236)

- July 2026 (46)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)