43% Of The Economy To Shut Down If Fuel Prices Do Not Go Below KES 150 Per Litre In The Next Epra Review

The numbers at a glance

| Indicator | Latest level | Direction | Economic meaning | Source |

| Nairobi petrol | Sh214.25/litre | Above Sh150 by Sh64.25 (+42.8%) | Raises movement, distribution and household costs | EPRA pump prices |

| Nairobi diesel | Sh232.86/litre | Above Sh150 by Sh82.86 (+55.2%) | Direct hit to logistics, food, factories, buses and generators | EPRA pump prices |

| Nairobi kerosene | Sh191.38/litre | Above Sh150 by Sh41.38 (+27.6%) | Direct pressure on low-income households | EPRA pump prices |

| Headline inflation | 6.7% in May 2026 | Up from 5.6% in April | Cost-of-living pressure accelerating | KNBS May CPI |

| Transport inflation | 16.5% in May 2026 | Up from 10.0% in April | Transport costs are transmitting the fuel shock | KNBS May CPI |

| Private sector PMI | 46.6 in May 2026 | Third straight month below 50 | Private sector output contracting | Reuters/Stanbic PMI |

| GDP growth | 4.6% in 2025 | Below the 5.0% Treasury projection | Economy entered shock with weak momentum | Reuters/KNBS |

Kenya is standing at the edge of an avoidable economic slowdown because the most important input in the economy has been priced as if it is a luxury. Fuel is not just something motorists buy at petrol stations. Fuel is the engine of food distribution, public transport, manufacturing, construction, emergency services, county trade, electricity generation backup, school transport, retail delivery and household survival. When petrol is above Sh214, diesel above Sh232 and kerosene above Sh191 in Nairobi, the entire economy is being forced to breathe through a blocked pipe.

The immediate demand must be clear: petrol, diesel and kerosene must be pushed below Sh150 per litre. That figure is not emotional. It is an economic relief threshold. At the latest Nairobi pump prices, petrol is Sh64.25 above that level, diesel is Sh82.86 above it and kerosene is Sh41.38 above it. In percentage terms, petrol is 42.8 percent above the relief threshold, diesel is 55.2 percent above it, and kerosene is 27.6 percent above it. Diesel is the most dangerous part of this crisis because diesel is the working fuel of the productive economy.

A government that thinks it is simply collecting more money per litre is missing the larger economic danger. When fuel becomes too expensive, the economy does not keep moving normally while the Treasury celebrates revenue. Trips are cancelled. Deliveries are postponed. Farmers sell less. Factories reduce shifts. Matatus raise fares and lose passengers. SMEs reduce stock. Households cut spending. When this happens across millions of people and businesses at the same time, government revenue is not protected; it is attacked from the demand side.

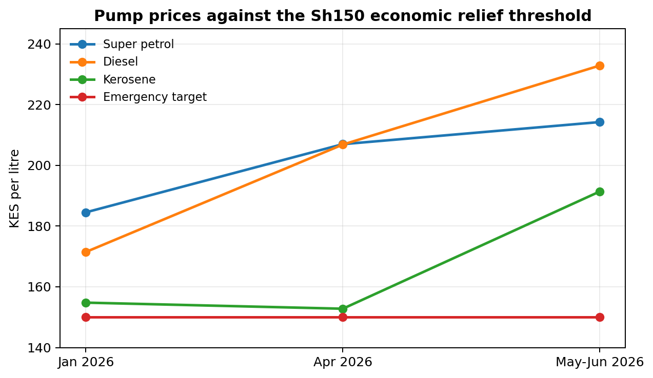

Figure 1: EPRA pump price data and the Sh150 economic relief threshold. Source: EPRA Pump Prices; Reuters reports on April and May fuel-price changes.

The graph above shows why the Sh150 demand matters. The economy had already been uncomfortable at January prices, but the movement from January to May-June has pushed fuel into a zone where the shock stops being a transport issue and becomes a national output issue. Diesel moved from Sh171.47 in January to Sh232.86 in the May-June cycle, an increase of Sh61.39 per litre, or about 35.8 percent. Petrol moved from Sh184.52 to Sh214.25, while kerosene moved from Sh154.78 to Sh191.38. That is not a small adjustment; it is a countrywide cost transfer.

The danger is that fuel costs do not remain inside fuel. They migrate. A litre of diesel enters the final price of milk, unga, vegetables, cement, building stones, bread, school transport, water delivery, security operations, hospital supplies and every item that has to be moved. Once diesel rises, the country should expect a delayed wave of price increases even in products that do not appear directly related to fuel. This is why policymakers who treat fuel as a narrow petroleum matter are intellectually negligent.

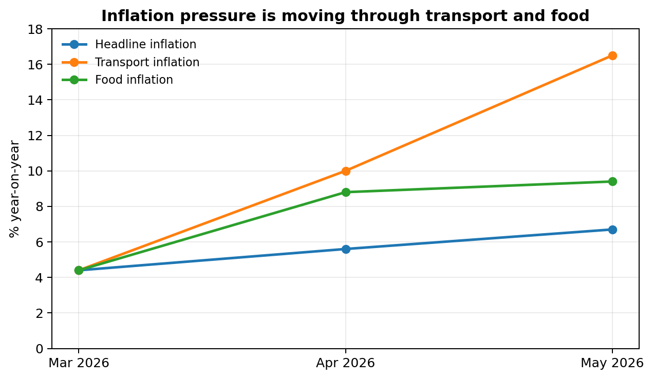

The inflation data already confirms the transmission. KNBS reported headline inflation at 5.6 percent in April 2026 and 6.7 percent in May 2026. More importantly, transport inflation accelerated from 10.0 percent in April to 16.5 percent in May. That means the fuel shock is moving into daily living costs. Food inflation also moved from 8.8 percent in April to 9.4 percent in May. Transport and food are the two categories that hit ordinary households first and hardest.

Figure 2: Inflation pressure from KNBS April and May 2026 CPI releases; March headline inflation added as a recent baseline point reported in market coverage.

This is how an economy begins to shut down without an official announcement. The first sign is not always a collapse in GDP. It is a contraction in private sector activity, weaker new orders, reduced customer traffic and fewer businesses willing to expand. Reuters reported that Kenya’s private sector PMI fell to 46.6 in May 2026 from 49.4 in April, marking the third straight month below the 50-point line that separates expansion from contraction. That is a serious warning. When businesses are already contracting, a fuel shock is not a small inconvenience; it is a multiplier of distress.

The current leadership of the economy appears to believe that Kenyans can absorb every shock because Kenyans have always survived. That is lazy thinking. Survival is not growth. Endurance is not prosperity. A citizen who uses all income on fare, food, tokens and rent is not participating in economic expansion. A business that remains open but stops hiring, stocking and investing is not healthy. A country can look busy while its productive base is being hollowed out.

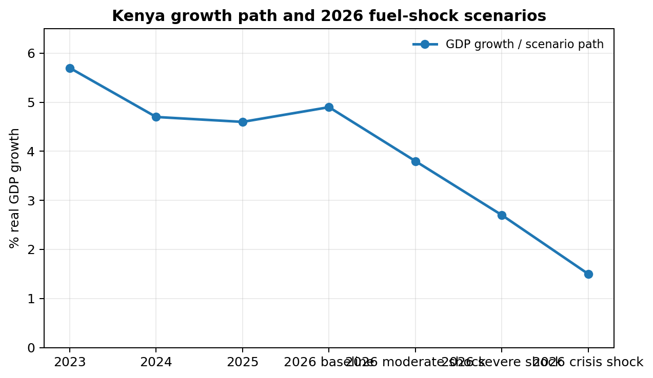

Kenya’s recent growth path was already not strong enough to absorb this kind of energy shock. The economy grew by 5.7 percent in 2023, slowed to 4.7 percent in 2024 and recorded 4.6 percent growth in 2025. KNBS had projected 4.9 percent growth for 2026, but that projection becomes fragile when fuel prices, inflation, transport costs and private-sector contraction all move in the wrong direction at the same time.

Figure 3: Historical growth from public economic reporting; 2026 scenarios are Soko Directory Research Team stress projections based on persistence of high fuel prices, inflation and PMI weakness. They are projections, not official forecasts.

The projection in Figure 3 is deliberately presented as a scenario model, not as an official forecast. If fuel prices are reduced quickly, the economy can still defend a growth path near the baseline. If fuel remains around current levels for several more months, growth can easily slip toward the 3.8 percent range as transport, retail and production slow down. If the shock persists through the budget cycle and triggers wider business closures, reduced consumption and social unrest, a severe scenario around 2.7 percent becomes possible. In a crisis scenario, where the fuel shock combines with transport paralysis, weak purchasing power and policy confusion, growth could be pushed toward 1.5 percent.

That is the macroeconomic danger. But the lived economy may feel worse than the GDP number. GDP is an annual national measure; daily economic activity is what families and businesses experience. A trader who cannot restock has suffered a 100 percent interruption for that day. A matatu that parks because diesel is too expensive has suffered a complete operating shutdown for that unit. A factory that cuts shifts has not waited for GDP to confirm pain. The shutdown begins at unit level before it appears in national accounts.

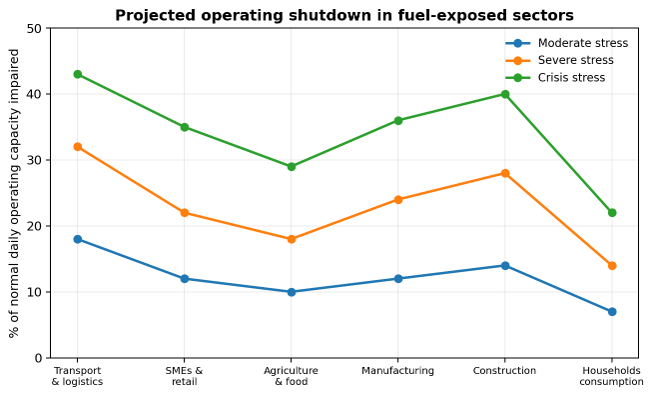

For that reason, the 43 percent figure should be understood carefully. It should not be presented as an official forecast that national GDP will fall by 43 percent. That would be inaccurate. The more defensible position is that, under a crisis scenario, up to 43 percent of normal daily operating capacity in the most fuel-exposed sectors can be impaired. Transport and logistics are the clearest example because every trip requires fuel, every delay affects supply chains and every fare increase reduces mobility.

Figure 4: Soko Directory Research Team operating-stress model. The chart estimates daily operating capacity impaired in fuel-exposed sectors under moderate, severe and crisis scenarios if pump prices remain elevated.

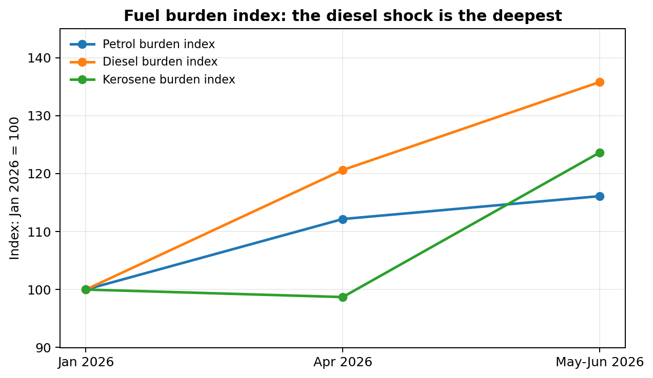

The fuel burden index shows the same story from another angle. Using January 2026 as the base, diesel has become the deepest shock. That matters because diesel powers the economic arteries. Petrol affects mobility and services; kerosene affects household survival; diesel affects the movement of almost everything. If diesel does not come down, even a household that does not own a car will still pay for diesel through food, fares, school fees, rent, construction materials and retail prices.

Figure 5: Fuel burden index calculated from EPRA and Reuters-reported pump price levels. January 2026 = 100.

The first sector to break is transport. Matatus, buses, boda riders, taxis, lorries and delivery vans cannot run on patriotic speeches. If diesel and petrol remain above Sh200, fares rise. When fares rise, workers travel less, consumers avoid town centres, students struggle, small traders reduce market trips and service businesses lose customers. The country then experiences mobility destruction, which is a direct attack on productivity.

The second sector to suffer is food. Kenya’s food system is transport-heavy. Farm produce moves from rural farms to aggregation centres, then to markets, wholesalers, retailers and households. Each stage has a fuel cost. Expensive diesel means tomatoes, potatoes, maize, milk, vegetables, meat, flour and cooking oil become more expensive even before the farmer earns more. The consumer pays more, the farmer may not benefit, and the middle of the chain becomes more expensive and more fragile.

The third sector is manufacturing. Factories pay for raw materials, transport, power, backup generators, packaging and distribution. High fuel and high electricity costs squeeze both input and output sides. A manufacturer cannot simply pass every cost to the consumer because demand is already weak. The likely result is reduced shifts, delayed expansion, lower production, layoffs or higher prices. None of those outcomes supports growth.

The fourth sector is construction. Cement, steel, ballast, sand, timber, tiles, glass, labour movement and site machinery all carry fuel costs. Construction is one of Kenya’s major job creators, especially for young people and informal workers. When fuel rises, building slows, developers postpone projects, transporters charge more and casual workers lose daily income. The pain moves from the pump to the fundi, the mason, the supplier and the tenant.

The fifth sector is retail and SMEs. A small shop depends on affordable stock movement and customers with disposable income. High fuel damages both. The trader pays more to bring stock, then faces customers whose money has already been eaten by fare, food, rent and tokens. The shopkeeper is trapped: raise prices and lose customers, or keep prices low and lose margin. That is how many SMEs die without making headlines.

The sixth and most politically dangerous impact is households. Kerosene at Sh191.38 is not an elite problem. It is a poor household problem. Expensive paraffin means families cook less, light less and cut other essentials. Petrol and diesel then hit the same household through fares and food. Electricity costs add the final layer. At that point, citizens are not merely complaining; they are being economically cornered.

Scenario projection: what happens if fuel does not come down

| Scenario | Fuel condition | Likely GDP growth path | Operating shutdown risk | Practical meaning |

| Relief correction | Fuel cut below Sh150 within the pricing cycle | 4.5% to 4.9% | Low to moderate | Inflation cools, movement improves, SMEs regain breathing space |

| Moderate stress | Fuel remains near current levels for 2-3 months | Around 3.8% | 10% to 18% in exposed activities | Transport, retail and food prices remain under pressure |

| Severe stress | Fuel remains high through the budget cycle | Around 2.7% | 18% to 32% in exposed activities | Closures, fare hikes, weak consumption and reduced production accelerate |

| Crisis stress | High fuel combines with unrest, shortages and policy confusion | Around 1.5% | 22% to 43% in exposed activities | Daily economic activity in transport-heavy sectors partially shuts down |

The most incompetent response would be to wait and see. Waiting is itself a decision. Every pricing cycle that leaves fuel at these levels transfers more cost into food, transport, power, rent and wages. Every month of delay increases the probability that businesses will not merely complain but adjust permanently by reducing staff, reducing operations or shutting down.

The government must stop pretending that expensive fuel is a clean revenue strategy. A high tax per litre can still produce lower total revenue if litres sold fall, businesses shrink and taxable transactions reduce. VAT is collected when people buy. PAYE is collected when people work. Corporate tax is collected when businesses make profits. Excise is collected when economic activity continues. Kill activity and the tax base dies with it.

The policy answer must be immediate and measurable. First, reduce the tax and levy load per litre until petrol, diesel and kerosene move below Sh150. Second, publish a transparent breakdown of every shilling in the pump price. Third, protect diesel as a strategic economic input because it powers food, logistics, factories and public transport. Fourth, cushion kerosene because it is the fuel of poor households. Fifth, audit procurement and landed costs so that global shocks are not multiplied locally by domestic inefficiency.

Kenya also needs honesty. Not every fuel increase is caused by the global market. KNCCI has already warned that while global shocks are real, domestic cost build-up through taxes, levies, exchange-rate effects, margins and landed costs amplifies the pain. That means the state cannot hide behind the Middle East, crude oil or external war while refusing to fix the Kenyan part of the price.

Those in charge of the economy must be told directly: this is not a spreadsheet exercise. It is a survival issue. An economy where diesel is above Sh232, petrol above Sh214 and kerosene above Sh191 is an economy being forced to run while bleeding. If the fuel price does not come down, Kenya will not only face inflation. It will face reduced movement, reduced demand, reduced production, reduced tax collection and rising public anger.

Fuel below Sh150 is therefore not populism. It is emergency economic repair. It is the fastest way to lower transport pressure, protect food affordability, reduce business costs, support SMEs, defend jobs and restore confidence. The economy runs on fuel. Any leadership that cannot understand this is not managing the economy; it is gambling with the country’s productive life.

Read Also: KRA Sacrifices Ksh 9.1 Billion in Revenue to Cushion Kenyans from High Fuel Costs

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (278)

- August 2026 (35)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)