EABL Leads As Foreign Investors Become Very Cautious

The Nairobi Securities Exchange closed the session with a quiet but revealing message: the market is no longer moving as one broad block. It is now being pulled by selective counters, defensive foreign flows, and concentrated liquidity in names that still carry institutional confidence. On the surface, the indices looked mixed and calm.

Beneath the surface, however, turnover fell sharply, foreign investors controlled half of the market activity, EABL became the day’s liquidity anchor, and Safaricom slipped under local selling pressure.

| Metric | Value | Metric | Value |

| NASI daily move | -0.12% | N10 daily move | +0.25% |

| NSE 20 daily move | +0.06% | NSE 25 daily move | +0.15% |

| Equity turnover | KES 468.8m / USD 3.6m | Turnover contraction | -57.3% |

| Foreign turnover share | 50.7% | Foreign buys | USD 1.773m |

| Foreign sales | USD 1.891m | Net foreign outflow | USD 120.2k |

| Market cap | USD 26.7bn | Top turnover counter | EABL: 27.6% of turnover |

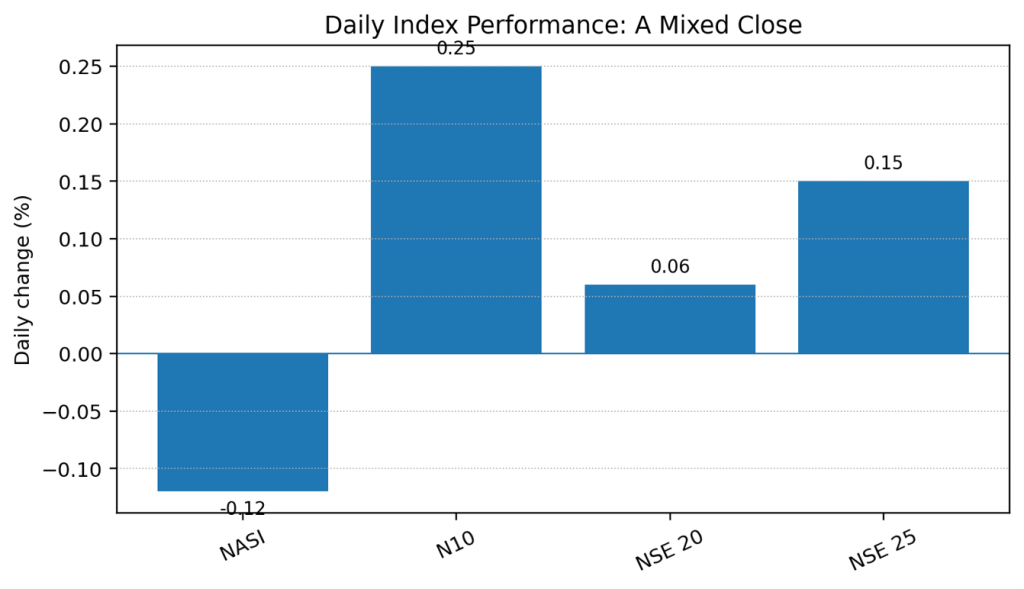

A Mixed Close That Hides a Stronger Story

The session ended on a mixed note. The N10 and NSE 25 gained 0.25% and 0.15% respectively, while the NSE 20 edged up by 0.06%. The NASI, however, slipped by 0.12%, showing that the broader market was slightly weaker even as selected blue-chip and large-cap counters provided support.

This is the kind of market where headline indices can understate what is happening inside the order book. Strength was not evenly distributed. Investors rewarded a small group of liquid counters while leaving other parts of the market thin, cautious, and vulnerable to small price moves.

Read Also: KCB Leads The Charge In A Promising Stock Market Year: A Closer Look at Top Performers

Figure 1: Daily index movements based on Standard Investment Bank data.

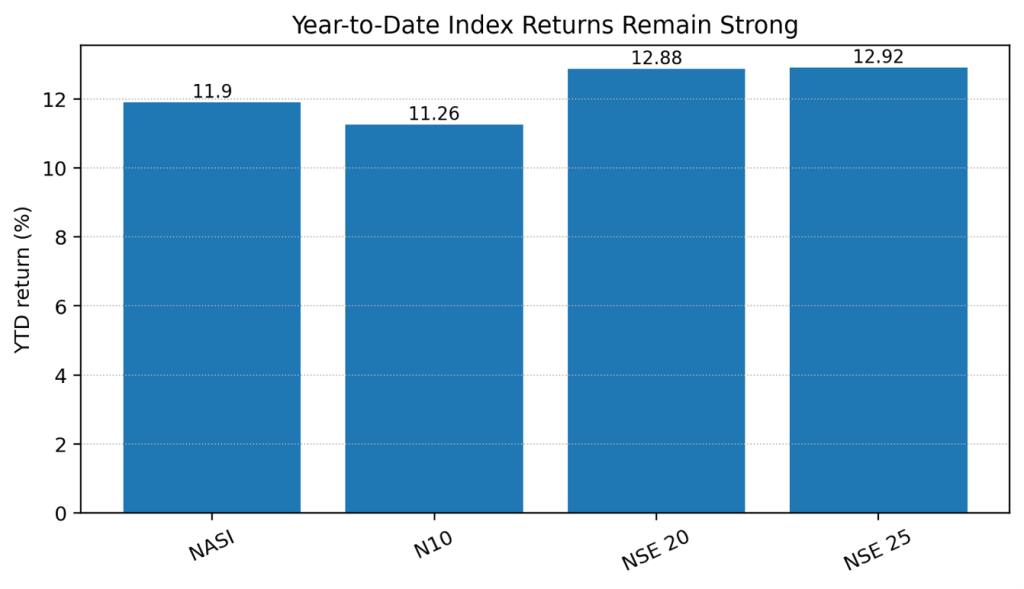

The Bigger Picture: YTD Gains Are Still Intact

Despite the soft daily tone, the broader return profile remains positive. NASI is up 11.90% year-to-date, N10 has gained 11.26%, NSE 20 is up 12.88%, and NSE 25 has advanced 12.92%. That tells us the market has not lost its 2026 upward structure; it has simply entered a more selective phase where liquidity and earnings confidence matter more than general optimism.

The strongest message from the YTD numbers is that the NSE remains in a constructive recovery cycle. But daily participation is becoming more disciplined. Investors are not blindly chasing the market. They are choosing where to deploy capital and where to reduce exposure.

Figure 2: Major NSE indices remain firmly positive year-to-date.

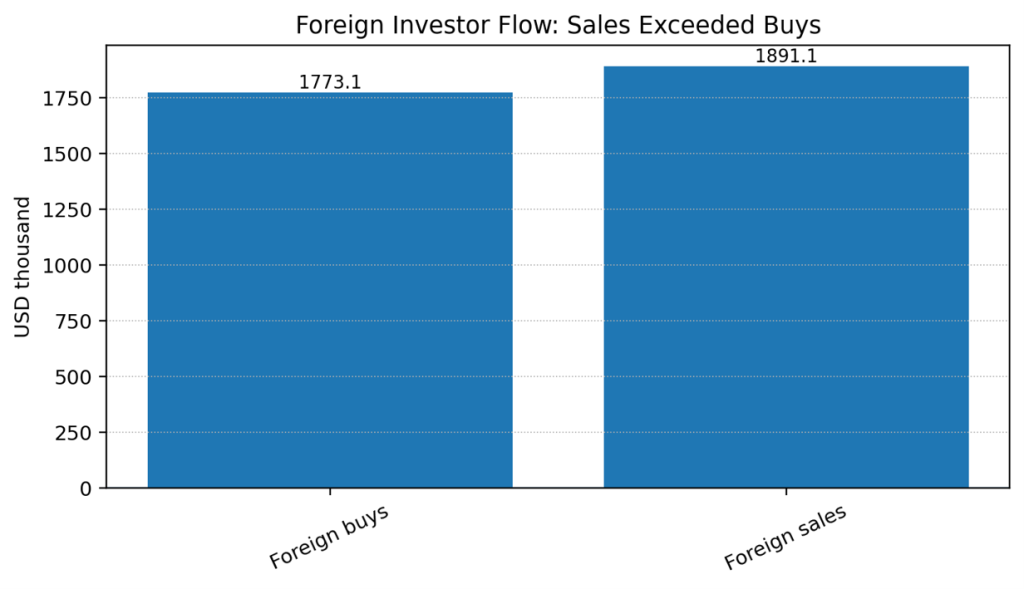

Turnover Collapsed, but Foreign Investors Took the Wheel

Equity turnover contracted to USD 3.6 million, a 57.3% decline from the previous session. A fall of this size is important because it changes the quality of price discovery. In a lower-turnover session, a few large institutional orders can heavily influence the tape, and that is exactly what the market showed.

Foreign investors accounted for 50.7% of total market turnover, up sharply from 32.6% in the previous session. That is a major shift in participation. It means foreign money was not sitting on the sidelines; it was actively shaping the market, even though the net position was bearish.

Foreign buys stood at USD 1.773 million against foreign sales of USD 1.891 million, leaving a net foreign outflow of about USD 120,200. The outflow was not dramatic in absolute terms, but it was symbolically important: foreign investors were present, active, and marginally sellers.

Figure 3: Foreign sales exceeded foreign buys, creating a mild net outflow.

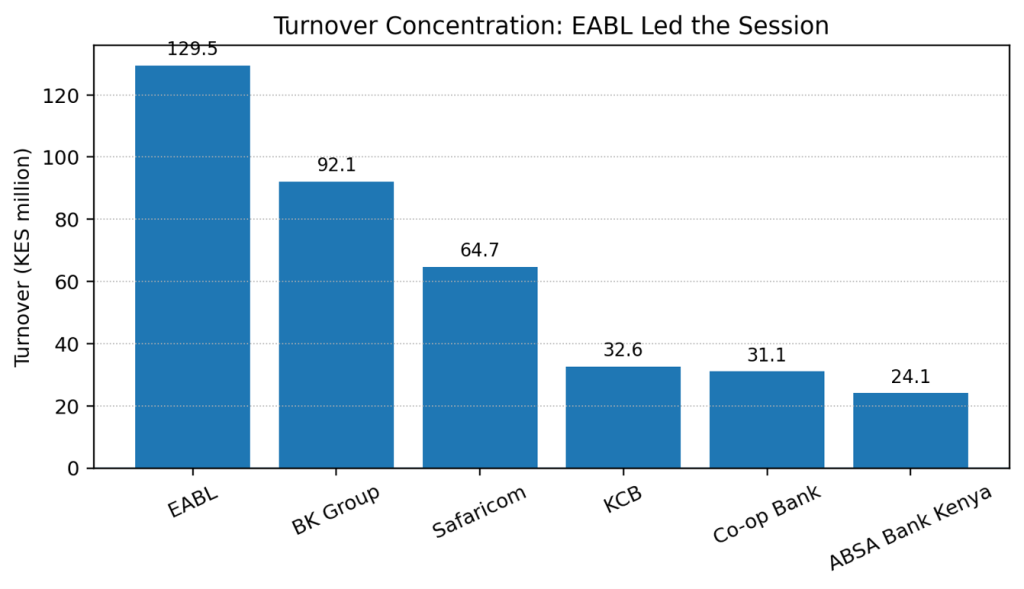

EABL Was the Market’s Liquidity Anchor

EABL dominated the session, accounting for 27.6% of the day’s turnover. Its share price strengthened by 0.6% to KES 250.00, supported largely by foreign investor activity. In a market where turnover had dropped sharply, EABL stood out as the counter that still attracted serious institutional participation.

This matters because liquidity is a form of confidence. When institutions continue to trade a counter heavily in a low-turnover market, it usually signals that the stock remains useful for portfolio positioning, rebalancing, or defensive exposure. EABL’s performance therefore gave the session one of its clearest positive anchors.

Figure 4: EABL led the top movers by turnover, followed by BK Group and Safaricom.

Banks Were Split, Not Weak

The banking counters sent a mixed but important signal. Co-op Bank rose 1.3% to KES 31.70, showing continued demand for selected domestic banking exposure. KCB remained unchanged at KES 69.25, suggesting price stability despite active foreign buying interest. Absa Bank Kenya declined 1.2% to KES 28.20, while BK Group softened by 0.5% to KES 53.75.

This split performance does not point to a banking selloff. It points to discrimination. Investors are separating the sector into individual stories based on liquidity, valuation, earnings confidence, dividend expectations, and foreign accessibility. In a selective market, sector labels matter less than counter-specific conviction.

Safaricom Slipped Under Local Pressure

Safaricom dipped 0.6% to KES 31.15, largely driven by local investor activity. This is important because Safaricom remains one of the NSE’s most watched counters and a key sentiment gauge for both retail and institutional investors. When Safaricom weakens while foreign buyers are active elsewhere, it suggests local investors may be taking profits, reallocating liquidity, or responding to short-term valuation pressure.

The counter still accounted for KES 64.7 million in turnover, making it one of the most active stocks of the day. The price decline therefore did not come from neglect. It came from meaningful participation on the sell side, especially from local investors.

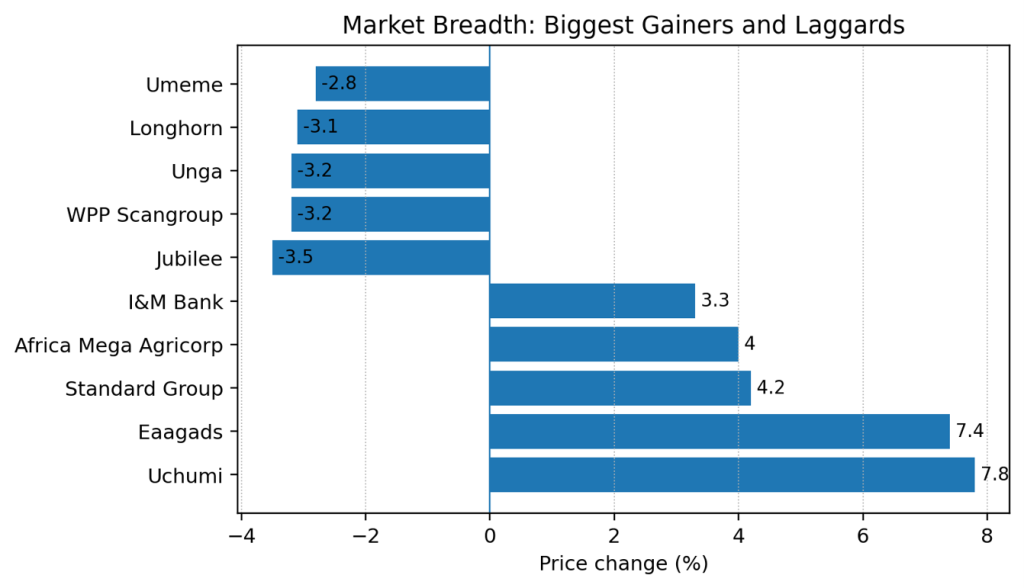

The Day’s Extremes: Uchumi Rallied, Jubilee Fell

Uchumi closed as the top gainer after rallying 7.8% to KES 1.65, followed by Eaagads at 7.4%, Standard Group at 4.2%, Africa Mega Agricorp at 4.0%, and I&M Bank at 3.3%. I&M’s advance to a record high of KES 55.00 was especially notable because it suggests continued investor confidence in the counter’s fundamentals and price momentum.

On the losing side, Jubilee shed 3.5% to KES 368.00, closing as the leading laggard after its KES 13.00 final dividend book closure. WPP Scangroup and Unga each fell 3.2%, Longhorn lost 3.1%, and Umeme declined 2.8%. The Jubilee move appears linked more to dividend adjustment dynamics than to a broad collapse in insurance sentiment.

Figure 5: Uchumi led gainers while Jubilee led the laggards after dividend book closure.

What This Session Really Tells Investors

The market’s message was not panic. It was selectivity. Turnover fell heavily, but the NSE did not break. Foreign investors were active, but slightly bearish. EABL attracted strong institutional interest. Banking counters moved in different directions. Safaricom weakened under local selling. Small-cap gainers produced sharp percentage moves, but the real liquidity remained concentrated in blue-chip names.

This is the type of market where serious investors must look beyond the headline index. The most important question is not whether the NASI was up or down by a fraction of a percentage point. The real question is where money actually moved, who was buying, who was selling, and which counters continued to command liquidity when total turnover contracted.

On that basis, the session was a disciplined reminder that liquidity is power. EABL had it. Safaricom had activity but faced local pressure. Banks were selective. Foreign investors came back to the centre of trading but ended the day as net sellers. The NSE remains positive for the year, but the next leg of the market will likely be driven by earnings quality, dividend clarity, foreign flow consistency, and confidence in Kenya’s macro direction.

Market Data Tables

| Counter | Price (KES) | % chg | Turnover (KES m) | Turnover (USD k) | Shares traded (k) | Foreign buys | Foreign sales |

| EABL | 250.00 | 0.6 | 129.5 | 998.9 | 518.0 | 93.6% | 99.5% |

| BK Group | 53.75 | -0.5 | 92.1 | 710.3 | 1,713.5 | 99.2% | 99.2% |

| Safaricom | 31.15 | -0.6 | 64.7 | 498.7 | 2,074.7 | 0.0% | 7.7% |

| KCB | 69.25 | 0.0 | 32.6 | 251.7 | 470.9 | 42.4% | 32.6% |

| Co-op Bank | 31.70 | 1.3 | 31.1 | 239.9 | 981.1 | 0.0% | 0.0% |

| ABSA Bank Kenya | 28.20 | -1.2 | 24.1 | 185.5 | 853.1 | 0.0% | 0.0% |

Read Also: The Kenyan Stock Market Closes The Week Tumbling Down As Foreign Investors Drive Sell-Off

About Soko Directory Team

Soko Directory is a Financial and Markets digital portal that tracks brands, listed firms on the NSE, SMEs and trend setters in the markets eco-system.Find us on Facebook: facebook.com/SokoDirectory and on Twitter: twitter.com/SokoDirectory

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (278)

- August 2026 (26)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)