The Market Is Loud But Wealth Is Made In Silence

Modern earphones are sold with one feature that sounds almost magical: noise cancellation. They do not stop the world from making noise. They identify the disturbance, reduce its power and allow you to hear what actually matters.

That is also one of the most valuable skills an investor can develop. The stock market is never quiet. Every trading day arrives with breaking news, analyst opinions, political speeches, rumours, forecasts, social-media panic and dramatic headlines written to make people click before they think.

The problem is not that all this information is false. The problem is that much of it is incomplete, exaggerated, short-term or stripped of the context needed to make a sound investment decision. A headline may accurately report that billions of shillings have been wiped from the market in one session, yet tell you almost nothing about whether a strong company has permanently lost its ability to earn money.

Markets are emotional in the short run. Prices can fall because foreign investors need dollars, interest rates have risen, a currency has weakened, institutions are rebalancing portfolios, a war has frightened global capital or traders simply expect other traders to sell. None of these automatically means that every business on the exchange has suddenly become worthless.

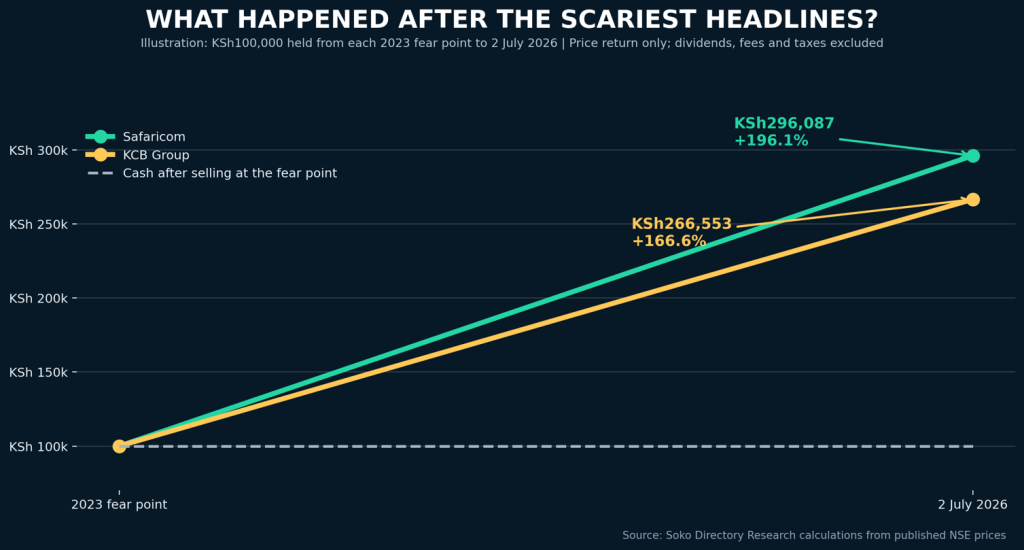

Kenyan investors saw this clearly in 2023. The Nairobi Securities Exchange was surrounded by fear. KCB Group’s market value fell below KSh100 billion after its share price dropped to KSh29.45 in May. Safaricom later fell to KSh11.50 on 3 November. The headlines were severe, the mood was dark and pessimism became so widespread that avoiding shares appeared wiser than owning them.

Many people reacted to the price instead of investigating the business. Some sold after the fall had already happened. Others decided the market was a casino and stayed away completely. A third group waited for the news to become positive again, forgetting that by the time optimism becomes obvious, the cheapest prices are normally gone.

By the close of trading on 2 July 2026, KCB was at KSh78.50 and Safaricom was at KSh34.05. From those 2023 fear points, KCB had risen by about 166.6 percent and Safaricom by about 196.1 percent, before counting dividends. A hypothetical KSh100,000 exposed to the same price movement would have grown to roughly KSh266,553 in KCB or KSh296,087 in Safaricom, excluding transaction costs, taxes and dividends.

Read Also: Djibril Tobe Named Airtel Kenya MD, Succeeding Ashish Malhotra After Four Years of Record Growth

Figure 1: The illustration compares price movement from each company’s cited 2023 fear point to 2 July 2026. It is not a claim that the exact bottom could have been predicted.

The important lesson is not that anyone could have known the exact bottom. Almost nobody can do that consistently. The lesson is that a falling price and a failing business are not the same thing. Investors who understood that distinction were able to examine the companies, assess the risks, compare price with underlying value and act without allowing fear to decide for them.

Noise says, ‘The share is falling, therefore the company is bad.’ Analysis asks, ‘What has changed in revenue, profit, cash generation, debt, asset quality, market share, regulation, management and long-term competitive strength?’ Noise watches the ticker every hour. Analysis reads financial statements and company disclosures. Noise demands certainty today. Analysis accepts uncertainty but insists on a margin of safety.

This is why stock-market wealth is often built during uncomfortable periods. When everyone feels safe, prices may already reflect the good news. When everyone is frightened, good companies can be priced as though temporary problems will last forever. The disciplined investor does not celebrate bad news or buy blindly. The disciplined investor simply understands that fear can create mispricing.

There is, however, a dangerous misunderstanding that must be removed. Ignoring noise does not mean ignoring evidence. Not every share that falls will recover. Some companies decline because their products are becoming irrelevant. Others are drowning in debt, losing customers, manipulating accounts, suffering governance failures or destroying shareholder capital. Patience cannot rescue a broken investment thesis.

True investment noise cancellation is therefore not deafness. It is filtration. It means separating information that changes the value of a business from information that merely changes the mood of the market. A profit warning, major fraud, unsustainable debt or permanent regulatory damage may be a signal. A frightening headline that repeats yesterda