Kenya’s Credit Upgrade: Relief, Not Redemption

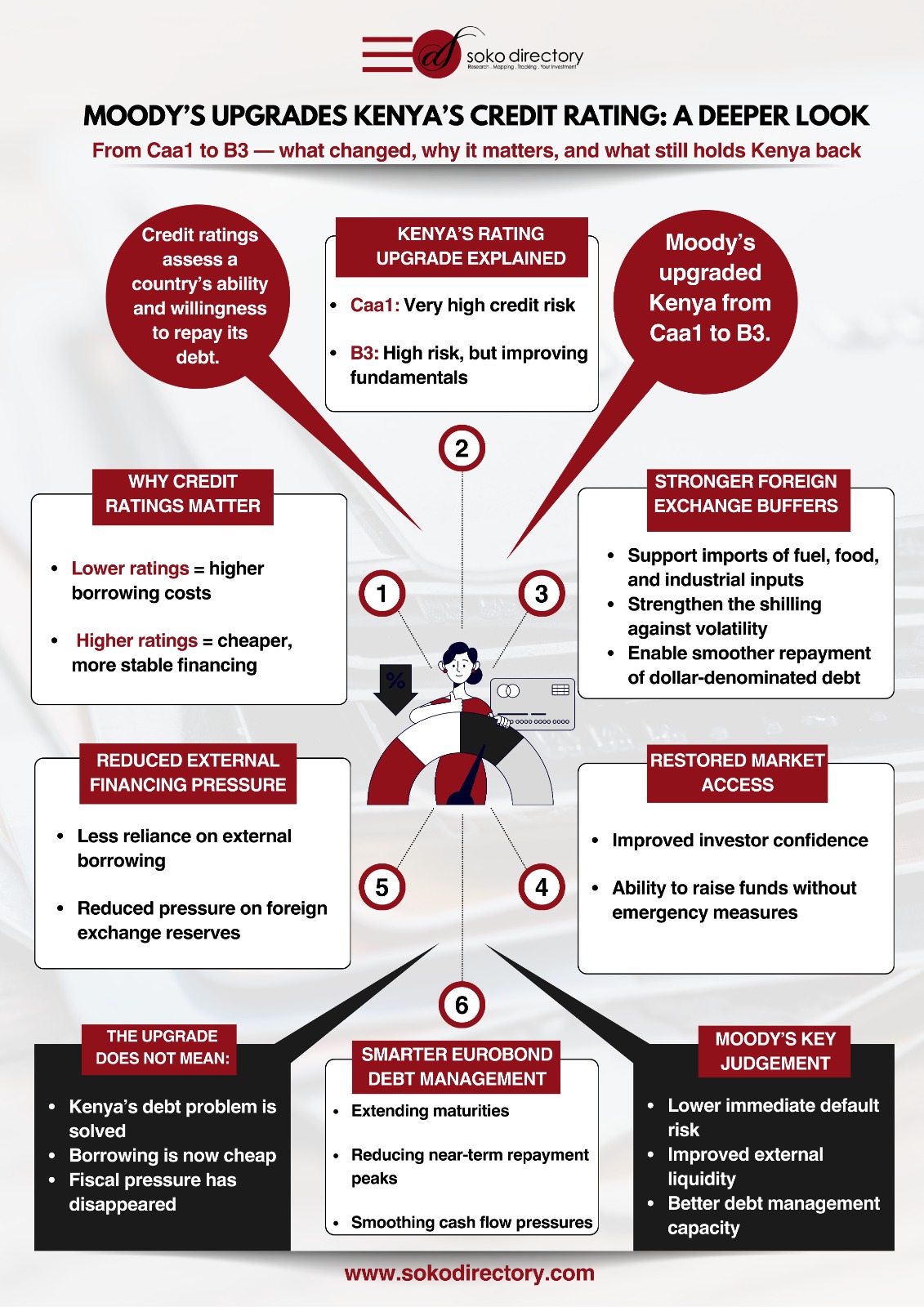

Moody’s decision to upgrade Kenya’s credit rating from Caa1 to B3 is not a celebration of success, but a recognition that the country has stepped back from the edge of a financial cliff.

In plain terms, Kenya is now viewed as slightly safer to lend to than it was before, and the fear of an immediate default has eased. That alone tells you how low the bar had fallen.

This is not a vote of confidence in economic brilliance; it is an acknowledgment that the bleeding has slowed.

The upgrade is anchored in one critical improvement: Kenya’s foreign exchange reserves are stronger. This matters because the country runs on dollars.

Fuel, medicine, machinery, and debt repayments all demand hard currency. With more dollars in reserve, Kenya can meet its external obligations with less panic, fewer emergency loans, and reduced pressure on the shilling.

At the same time, the current account deficit has narrowed, meaning the country is importing less relative to what it earns, a small but important step toward balance.

Equally important is Kenya’s return to international capital markets. After months of fear, speculation, and near exclusion, the country has shown it can still raise money and manage its Eurobond obligations.

Read Also: Moody’s assigns first-time ratings to Kenya’s Equity Bank and Coop Bank

By refinancing and restructuring debt, the government has pushed back repayment timelines and eased short-term pressure. This is not debt reduction, but debt rearrangement, buying time rather than solving the problem. Markets reward breathing space, even when structural weaknesses remain.

But this is where the optimism must stop. Kenya’s debt is still heavy, expensive, and growing. Interest costs are swallowing a dangerous share of government revenue, leaving little room for development, services, or emergencies.

The state continues to spend more than it earns, relying on borrowing to close the gap. This is not sustainability; it is endurance. You can survive like this for a while, but the bill always arrives.

Moody’s itself is clear: the upgrade has limits. Weak debt affordability caps further progress. High interest rates mean every new loan tightens the noose. Large fiscal deficits signal a government that has not yet aligned spending with reality.

In other words, Kenya is no longer in free fall, but it is still flying too low, too heavy, and with too little fuel.

This rating change should be read as a warning, not a victory lap. It tells policymakers that markets are watching, that discipline matters, and that cosmetic fixes are no longer enough.

Strong reserves and clever debt management can calm nerves, but they cannot replace serious fiscal reform, spending control, and growth driven by production rather than taxation.

Kenya has bought time. What it does with that time will determine whether this upgrade becomes the foundation of recovery or just a brief pause before the next downgrade. The window is open, but it will not stay open forever.

Read Also: Moody’s Affirms East African Development Bank’s Baa3 Rating

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com