From KSh100,000 to KSh113,077 in Six Months: Why Owning Great Companies Could Be Kenya’s Most Powerful Wealth-Creation Habit

There is a difference between working for money and making money work. For millions of Kenyans, income enters through a salary, a business, a contract or a side hustle, but most of it is consumed by rent, school fees, food, transport, debt and emergencies. Whatever remains is often left in cash, where it feels safe but may not create meaningful long-term wealth. The stock market offers a different proposition: instead of merely storing money, an investor can use it to acquire ownership in productive companies that earn profits, expand, pay dividends and increase in value.

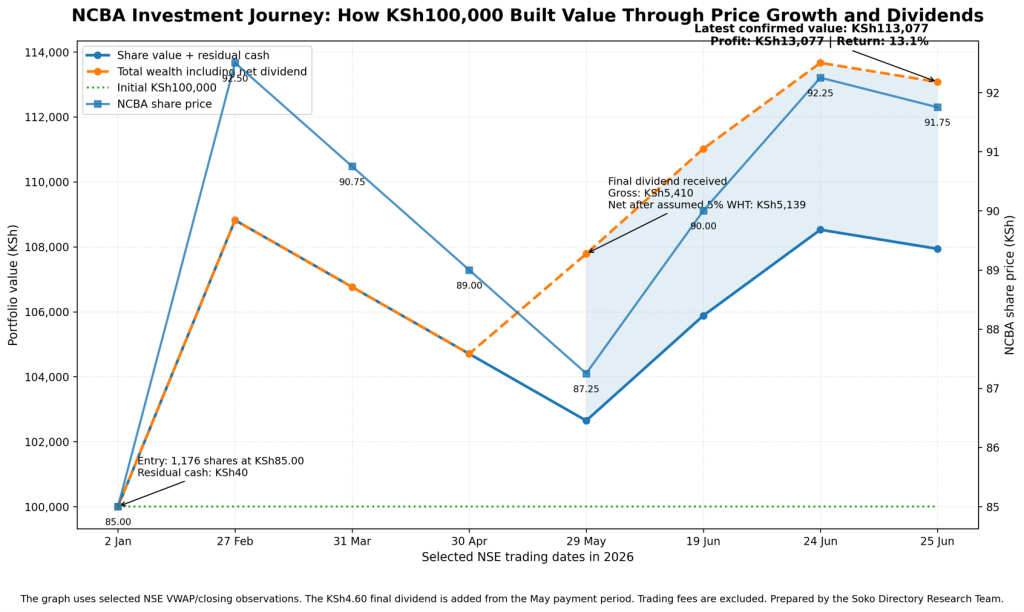

NCBA Group provides a timely illustration. Using the first trading day of 2026 as the entry point, KSh100,000 invested at an NSE volume-weighted average price of KSh85.00 would have bought 1,176 shares and left KSh40 uninvested. At the latest confirmed closing price used in this analysis, KSh91.75, those shares would be worth KSh107,898. The investor would also have qualified for the KSh4.60 final dividend, producing KSh5,410 gross, or approximately KSh5,139 after an assumed 5% resident withholding tax.

That brings the total position to roughly KSh113,077 before brokerage and statutory trading charges. The wealth created is approximately KSh13,077, equivalent to 13.1% in under six months. Of that return, about KSh7,938 came from the increase in the market value of the shares, while KSh5,139 came from the cash dividend. This is the central power of direct equity ownership: the investor can benefit from both capital appreciation and a share of the company’s distributed profits.

Read Also: Mwalimu Sacco, NCBA Launch Salo Xpress to Streamline Payroll Processing

The Numbers Behind the KSh100,000 Investment

| Component | Calculation | Result |

| Shares purchased | Floor(100,000 ÷ 85.00) | 1,176 shares |

| Cash used | 1,176 × 85.00 | KSh 99,960 |

| Residual cash | 100,000 − cash used | KSh 40 |

| Market value | 1,176 × 91.75 | KSh 107,898 |

| Gross final dividend | 1,176 × 4.60 | KSh 5,410 |

| Net dividend | Gross dividend less assumed 5% WHT | KSh 5,139 |

| Total wealth | Market value + residual cash + net dividend | KSh 113,077 |

| Total profit | Total wealth − initial capital | KSh 13,077 |

The Detailed Investment Trajectory

Figure 1: The portfolio did not rise in a straight line. The dividend created a second return stream and helped lift total wealth above the value of the shares alone.

This Was Ownership, Not a Get-Rich-Quick Bet

The most important lesson is not that every share will rise by 13% in six months. Markets do not move in straight lines, and no company is guaranteed to repeat past performance. The lesson is that a disciplined investor can convert ordinary savings into ownership of an operating business. Once the purchase is made, the investor is no longer standing outside the economy as a customer only. The investor becomes a shareholder with an economic interest in the company’s future profits, assets, strategy and distributions.

The chart in this report makes the journey visible. NCBA’s price rose strongly in February, softened in March and April, dipped further by late May, then recovered in June. An investor who panicked during the decline could have sold too early. A patient investor who remained focused on the underlying business received the dividend and participated in the recovery. Wealth creation through equities is therefore not only about identifying a strong company. It is also about emotional discipline, time in the market and the ability to separate temporary price movement from long-term business value.

Why NCBA Has Become a Bank to Watch

The share-price performance is supported by business momentum. NCBA reported profit after tax of KSh6.0 billion in the first quarter of 2026, up 9% from the same period a year earlier. Operating income rose 15% to approximately KSh20.0 billion. Net interest income increased 22%, while non-funded income grew 6%. These figures matter because they show that earnings growth was not dependent on one narrow revenue source.

The balance sheet also expanded. Customer deposits reached approximately KSh544 billion, representing 10% year-on-year growth, while total assets rose 13% to about KSh741 billion. Net loans and advances increased 13% to roughly KSh324 billion. A growing deposit base gives a bank funding capacity; a growing loan book shows that it is deploying capital into households, companies and economic activity. When this expansion is combined with improving income, the business begins to offer shareholders a stronger platform for future earnings.

NCBA is also more diversified than a conventional branch-based lender. The Group reported KSh391 billion in digital loans disbursed during Q1 2026, a 27% increase. Its digital banking subsidiaries delivered 50% profit growth, while assets under management in the investment business rose to about KSh102 billion. Insurance, bancassurance, leasing and investment banking add additional earnings streams. This matters to investors because diversified businesses are generally better positioned to absorb pressure in one segment while continuing to grow elsewhere.

The Group remains a major player in asset finance, with a reported market share of about 32%. That gives it exposure to vehicle purchases, logistics, mobility, corporate investment and household consumption. In this sense, NCBA is not simply a bank counter on the NSE. It is a window into several parts of the economy: credit demand, digital borrowing, corporate transactions, insurance penetration, wealth management and regional commerce.

There are risks that investors must monitor. NCBA’s Q1 2026 impairment charge rose sharply as the Group took a more prudent view of credit risk. A bank can grow loans and income while still facing pressure from bad debts, economic weakness or regulatory changes. The correct investment response is therefore neither blind praise nor fear. It is continuous analysis of profitability, asset quality, capital strength, dividends, valuation and strategy.

Why Direct Stock-Market Ownership Is Such a Strong Wealth-Building Route

First, shares give ordinary people access to productive assets. Building a bank, a telecommunications network, a cement factory or a national retail business requires enormous capital. Buying listed shares allows an individual with a much smaller amount to own a fraction of these enterprises. The investor gains exposure to professional management, established brands, infrastructure, customers and future expansion without having to create the entire business from the ground up.

Second, equities can create two return streams. The market price can appreciate as earnings, assets and investor expectations improve. The company may also distribute part of its profits as dividends. In the NCBA example, the share-price gain alone lifted the original capital above KSh107,000, while the dividend added more than KSh5,000 net. Reinvested dividends can purchase additional shares, which may generate more dividends and further gains. That is compounding: returns begin to earn returns.

Third, listed shares are generally more divisible and liquid than many traditional Kenyan wealth assets. A plot of land may require a large lump sum, legal searches, transfer costs and time to sell. A listed equity portfolio can be built gradually and, subject to market liquidity, sold in portions. An investor can add KSh5,000, KSh10,000 or KSh20,000 at a time rather than waiting for millions. This makes the stock market particularly relevant to salaried workers, entrepreneurs and young investors building capital progressively.

Fourth, the market offers transparency. Listed companies publish financial statements, dividend notices, corporate actions and material disclosures. Prices are visible, and trades take place through regulated market infrastructure and licensed intermediaries. Transparency does not eliminate risk, but it gives the investor information with which to assess that risk. The Capital Markets Authority’s investor toolkit also emphasises that people do not need to be financial professionals to begin; they need education, proper market access and an understanding of their rights and responsibilities.

Fifth, direct equity ownership aligns personal wealth with economic growth. When a strong bank finances businesses, when a manufacturer expands output, when a telecom company adds customers or when an insurer grows premiums, shareholders can participate in the resulting value. The stock exchange becomes a bridge between household savings and enterprise growth. That is more productive than allowing all surplus cash to remain idle or be consumed by lifestyle inflation.

The Case for Starting Early and Staying Consistent

The amount invested matters, but time and consistency matter just as much. A person who waits until they have KSh1 million may remain outside the market for years. A person who begins with KSh10,000 and adds a fixed amount every month begins accumulating assets immediately. During market declines, the same monthly contribution can buy more shares. During recoveries, the larger accumulated position participates in the upside.

This is why the best investment habit is often systematic rather than dramatic. Salary day or business collection day can include an automatic allocation to investment. Dividends can be reinvested instead of being consumed. Over time, the investor moves from owning a few shares to owning a portfolio, and from receiving small dividends to receiving cash flows capable of paying real household obligations.

The psychological shift is equally important. Wealth is not only the money visible in a bank balance. It is the ownership of assets that can continue producing value. A person who directs every increase in income toward a larger car, more expensive rent or short-lived consumption may look prosperous while remaining financially fragile. A person who steadily accumulates shares may appear less flashy while building genuine net worth.

How to Invest Directly Without Turning Investing Into Gambling

Direct investing works best when it is approached as business ownership, not price chasing. Before buying a share, an investor should understand how the company makes money, whether profits and cash flows are growing, how much debt it carries, the quality of its management, its dividend record, the risks in its sector and whether the market price is reasonable relative to earnings and assets.

Diversification is essential. The NCBA result is an illustration, not an instruction to place all savings in one bank. A resilient portfolio may include several strong companies across banking, telecommunications, manufacturing, energy, insurance and other sectors. Investors can also combine equities with safer or more stable assets depending on their goals, age, income stability and tolerance for price fluctuations.

An emergency fund should come before aggressive equity investing. Money needed for rent, school fees, medical needs or near-term obligations should not be exposed to market volatility. Shares are most suitable for capital that can remain invested for several years. This long horizon gives the investor time to survive market declines and allows the underlying companies time to grow.

Costs must also be included. Brokerage commissions, levies, taxes and the bid-offer spread reduce the amount ultimately received. The KSh113,077 figure in this article is therefore a clean, pre-trading-cost illustration. Actual returns depend on the broker’s tariff, the execution price and the investor’s tax position. Using a licensed intermediary and keeping contract notes is part of responsible investing.

The Risks Are Real—But So Is the Cost of Never Owning Assets

Share prices can fall. Dividends can be reduced. A company can make poor strategic decisions, suffer fraud, face regulatory pressure or be damaged by an economic slowdown. Banking shares are particularly exposed to credit quality, interest rates, currency movements and the health of borrowers. Investors must therefore review results rather than treating any company as permanently safe.

Yet avoiding every market risk creates another risk: the risk of never building ownership. Cash that is not invested may lose purchasing power over time, while income can be consumed without leaving an asset behind. The sensible answer is not reckless concentration and not permanent fear. It is informed participation: research, diversification, patience, reasonable valuation and regular investing.

The Bigger Lesson for Kenyan Households

Kenya cannot build a broad ownership economy if the stock market is viewed as a private club for institutions, wealthy families or finance experts. Workers, business owners and professionals should be able to convert part of their monthly income into ownership of the companies shaping the economy. That shift would deepen domestic capital, reduce dependence on speculative fads and allow more Kenyans to benefit from corporate growth.

The NCBA example turns this argument into a number that is easy to understand. KSh100,000 did not have to buy land, launch a new enterprise or remain untouched in a cash account. It bought a stake in an established financial group. Within months, that stake generated both a market gain and a cash dividend. The result does not guarantee the future, but it demonstrates the mechanism by which wealth can be created.

For anyone serious about long-term wealth, direct stock-market ownership deserves a central place in the conversation. It is accessible, scalable, transparent and linked to productive enterprise. The strongest path is not to chase every rising counter. It is to build knowledge, buy quality at sensible prices, diversify, reinvest returns and allow time to do the heavy lifting.

Conclusion: Build Ownership, Not Only Income

On the conservative assumptions used here, KSh100,000 placed in NCBA at the beginning of January grew to approximately KSh113,077 by late June before trading costs. That is a KSh13,077 increase in wealth, created not by a lottery, a shortcut or a promise of guaranteed returns, but by owning shares in a profitable listed business and remaining invested through normal market movement. The lesson is bigger than NCBA: wealth grows when income is regularly converted into productive assets. For disciplined Kenyans prepared to research, diversify and think long term, the stock market is not merely a place where prices move. It is one of the most practical machines available for turning today’s earnings into tomorrow’s ownership.

A Responsible Direct-Equity Wealth Plan

- Keep a separate emergency fund before committing money to shares.

- Use a CMA-licensed stockbroker or investment bank and retain all contract notes.

- Buy businesses you understand, not counters that are merely trending.

- Diversify across several companies and sectors rather than concentrating in one share.

- Invest money that can remain in the market for years, not funds needed next month.

- Reinvest dividends where appropriate to accelerate compounding.

- Review company results, valuation, debt, cash flow, asset quality and governance.

- Include brokerage, levies and taxes when measuring the final return.

Important investment note

This article is an educational case study, not a recommendation to buy, hold or sell NCBA shares or any other security. Past performance does not guarantee future returns. Share prices and dividends can fall, and investors may lose capital. The appropriate investment mix depends on personal goals, time horizon, liquidity needs and risk tolerance. Professional advice may be appropriate before making material investment decisions.

Appendix: Selected NCBA Price and Portfolio Observations

The table below shows the observations used in the investment trajectory. Portfolio values include the KSh40 residual cash; total wealth includes the estimated net dividend from the May payment period.

| Date | NCBA price | Share value + cash | Total wealth incl. dividend |

| 2 Jan | KSh 85.00 | KSh 100,000 | KSh 100,000 |

| 27 Feb | KSh 92.50 | KSh 108,820 | KSh 108,820 |

| 31 Mar | KSh 90.75 | KSh 106,762 | KSh 106,762 |

| 30 Apr | KSh 89.00 | KSh 104,704 | KSh 104,704 |

| 29 May | KSh 87.25 | KSh 102,646 | KSh 107,785 |

| 19 Jun | KSh 90.00 | KSh 105,880 | KSh 111,019 |

| 24 Jun | KSh 92.25 | KSh 108,526 | KSh 113,665 |

| 25 Jun | KSh 91.75 | KSh 107,938 | KSh 113,077 |

Read Also: Why NCBA’s Visible Auctions Are Evidence of Scale and Transparency—Not a Broken Credit Model

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (222)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)