Why The Hardest Part Of Investing Is Not Finding The Perfect Asset, But Becoming The Person Who Can Keep Building Capital Through Every Milestone

Investing is a series of firsts. The first time you buy a share, a Treasury bond, a money-market fund, a unit trust or any productive asset, you cross an invisible line. You stop being only a consumer of money and begin becoming an owner of capital. The amount may be small, but the identity shift is enormous: part of your income is no longer being spent to solve today alone; it has been assigned the duty of building tomorrow.

That is why the first KSh 50,000 invested can be the most psychologically testing money you will ever accumulate. It is usually built when your salary still feels insufficient, emergencies are frequent, temptations are loud and the reward is almost invisible. You may contribute for months, open your statement and wonder why the balance does not yet look impressive. At this stage, the investment is not mainly testing your intelligence. It is testing whether your future can defeat your appetite for immediate comfort.

KSh 50,000 is small enough for the world to dismiss but large enough to prove that you can keep a promise to yourself. It teaches you that wealth begins before wealth becomes visible. The real return from this first milestone is discipline: the ability to earn money, separate a portion from your lifestyle, place it in a productive instrument and leave it untouched long enough to develop roots.

Your first KSh 100,000 feels different. The figure finally has weight. You begin to understand that the process is not a motivational slogan; it can actually work. The account can now absorb a bad week without collapsing. A dividend, distribution or interest payment becomes noticeable. You have evidence that money can produce money, even though the production is still modest.

This is also a dangerous stage because excitement can mutate into impatience. Once people see progress, some begin chasing shortcuts. They abandon a sound plan to pursue rumours, fashionable assets or promises of extraordinary returns. The first KSh 100,000 should deepen your respect for process, not seduce you into gambling. Capital that took months to build can be destroyed in minutes when conviction is replaced by greed.

The first KSh 250,000 is often the most difficult milestone because the novelty has disappeared but the portfolio is not yet large enough to feel life-changing. Consistency becomes repetitive. Friends may appear to be living better. New obligations arrive. You may be tempted to withdraw the money for a car deposit, a holiday, a phone upgrade or an avoidable emergency created by poor planning. This is the long middle, where many investment journeys quietly die.

Yet KSh 250,000 is where financial character begins to harden. You learn that successful investing is frequently boring. It is standing orders, automatic deductions, reinvested distributions, controlled fees, patient asset selection and the refusal to interrupt a good strategy because the market or social media has become noisy. The portfolio grows because you keep feeding it when nobody is applauding.

At KSh 500,000, conviction starts to mature. Half a million shillings is not financial freedom, but it is no longer an experiment. It is proof of capacity. You have shown that you can build a meaningful pool of capital from ordinary cash flows. More importantly, your decisions begin to change. You compare purchases with the return that money could have generated. You start asking whether an expense improves your life or merely advertises a lifestyle.

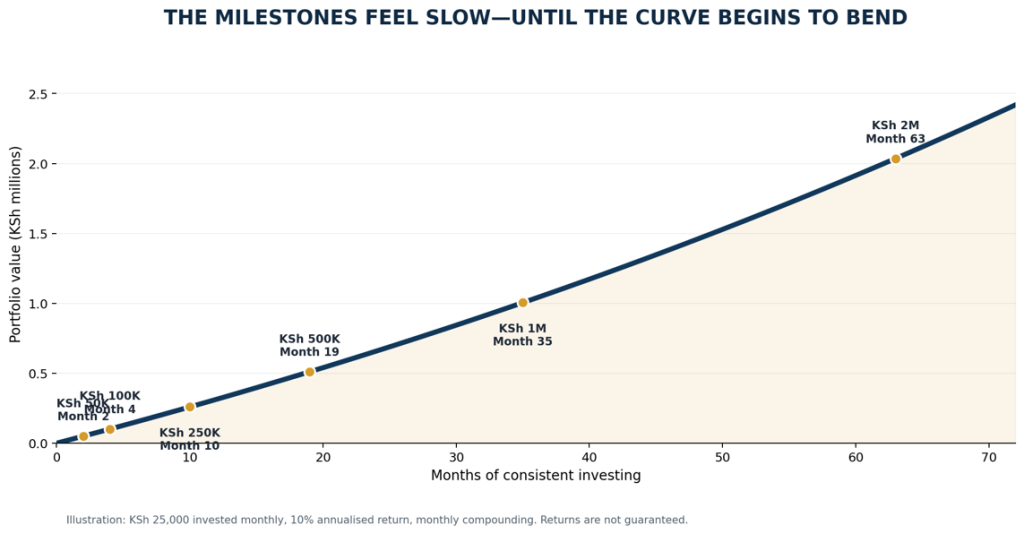

Figure 1: An illustrative path through the six milestones. Early progress is driven mainly by contributions; the curve gradually steepens as the portfolio base grows.

The first KSh 500,000 also teaches diversification. The question is no longer only how to save, but how to allocate. How much should remain liquid? How much can accept market volatility? What belongs in fixed income, equities, property, business or other assets? At this stage, good investing becomes less about finding one magical product and more about constructing a portfolio in which each asset has a clear job.

Then comes the first KSh 1,000,000. For many investors, this is the moment the journey becomes emotionally real. A million shillings is not an automatic passport to wealth, but it creates a meaningful buffer. It can generate returns that are visible, absorb market movements without instantly threatening your entire plan and give you room to think beyond survival. You are no longer trying to prove that you can start. You are proving that you can sustain.

The first million changes your relationship with risk. Before it, every loss may feel personal and every market decline may look like a disaster. After it, you begin to see volatility in shillings rather than fear. You understand that a temporary decline is not necessarily permanent destruction, that diversification matters and that capital preservation is as important as capital growth. The objective is not to avoid every red day; it is to remain invested without allowing one mistake to erase years of work.

A million shillings can also become a trap when it creates false confidence. Investors may assume that reaching a round number means they have mastered the market. They increase concentration, borrow to invest, ignore valuation or mistake a favourable season for personal genius. The wiser response is humility. The larger the portfolio becomes, the more carefully you must manage liquidity, taxes, fees, time horizon, risk and the quality of the assets you own.

At KSh 2,000,000, compounding becomes easier to see. A ten per cent year on KSh 50,000 is KSh 5,000 before costs and taxes; the same percentage on KSh 2 million is KSh 200,000. The rate has not changed, but the base has. This is the central power of capital: once the foundation becomes substantial, the same percentage return carries more financial force.

Compounding, however, is not magic and it is not guaranteed. It requires time, a reasonable return, reinvestment and the avoidance of catastrophic losses. Taxes and fees reduce the result. Markets can fall. Businesses can fail. Inflation can weaken purchasing power. The purpose of the compounding illustration is not to promise a smooth future; it is to show why patience becomes more valuable as the capital base expands.

The investment journey therefore has two engines. The first is contribution: the money you deliberately add from salary, business income or other cash flow. The second is return: the money produced by the assets already in the portfolio. In the early years, contribution does most of the heavy lifting. Later, if the portfolio performs reasonably and remains invested, returns can become an increasingly powerful partner.

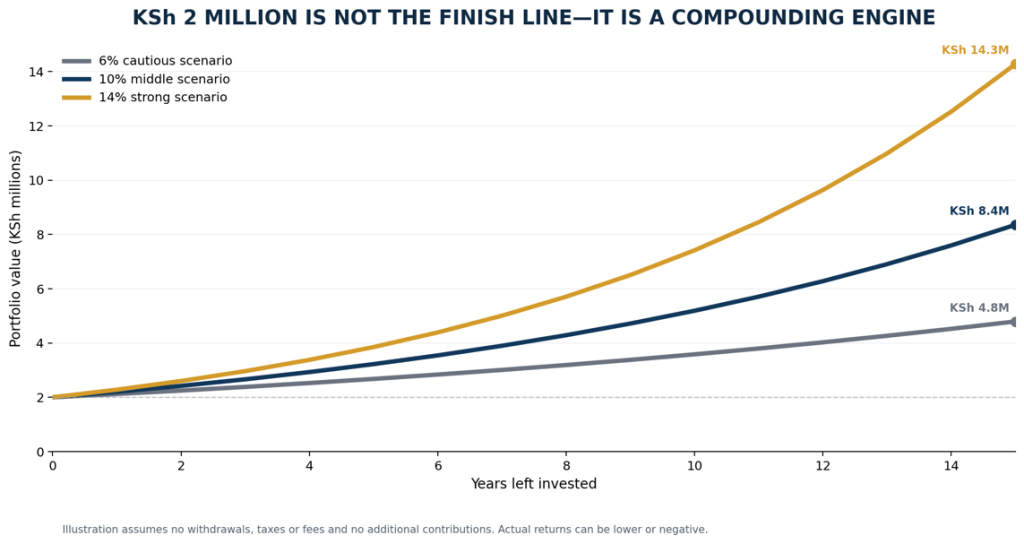

Figure 2: The same KSh 2 million can produce very different outcomes depending on return and time. The scenarios are illustrations, not forecasts or promises.

This is why investors should not despise modest beginnings. A person waiting to invest until they have a large amount may lose the habit-building years that matter most. The first objective is not to look rich. It is to create a repeatable system: earn, budget, protect against emergencies, invest, review, rebalance and continue. A strong system can survive changes in mood; a weak system depends on inspiration.

It is equally important to understand that the milestone amounts are not universal commandments. KSh 50,000 may be enormous for one household and easily available to another. Age, income, debt, dependants, health, location and financial responsibilities differ. The deeper principle is progression. Choose a milestone that stretches you without forcing reckless risk, then build the habits required to reach the next one.

Before pursuing aggressive growth, protect the foundation. Maintain an emergency reserve appropriate to your circumstances, manage expensive debt, insure major risks where suitable and avoid investing money that must pay rent, school fees or medical costs next month. Long-term capital needs time. When short-term obligations are mixed with long-term investments, the investor may be forced to sell at the worst possible moment.

The most powerful portfolio is not necessarily the one with the most complicated products. It is the one the investor understands, can fund consistently, can hold through difficult seasons and can align with a real goal. Wealth may be intended for retirement, education, a home, business expansion, family security or freedom from dependence. The clearer the purpose, the easier it becomes to resist distractions.

So celebrate the first KSh 50,000 because it proves you can begin. Respect the first KSh 100,000 because it reveals possibility. Defend the first KSh 250,000 because it is where patience is forged. Build carefully through KSh 500,000 because conviction is becoming structure. Protect the first KSh 1 million because the buffer is finally meaningful. Then allow KSh 2 million and every milestone after it to work—not as a trophy for display, but as productive capital assigned to your future.

In the end, the greatest transformation is not that the numbers become larger. It is that you become harder to distract, more deliberate with consumption, more patient with growth and more capable of thinking in years instead of weekends. The account balance records the money, but the real asset is the person disciplined enough to build it. Your first million does not make the journey complete. It makes the next chapter possible.

Read Also: When Africa Turns On Itself: Xenophobia Is The Fire, Failed Governance Is The Fire

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (236)

- July 2026 (33)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (270)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)