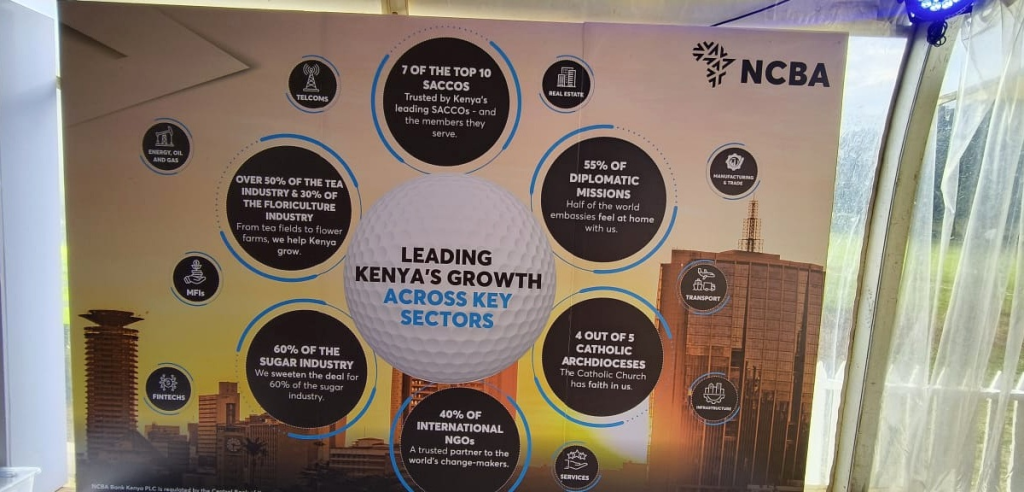

Why 7 of Kenya’s Top 10 SACCOs Bank With NCBA

Inside the technology, liquidity, security, and human relationships making NCBA a compelling bank of choice for Kenya’s cooperative economy.

| RESEARCH FOCUS Institutional banking infrastructure behind everyday SACCO services | CORE FINDING Scale matters, but specialised execution is what earns institutional trust |

At 7:03 on a Monday morning, a teacher checks whether a salary deduction has reflected in her SACCO account. A small-scale farmer waits for payment from a cooperative society. A young family needs a school-fees loan approved before the term begins. A transport operator wants to know whether a standing order cleared overnight. None of these people is thinking about banking architecture, settlement files, liquidity buffers, cyber controls or reconciliation engines. They simply expect the SACCO to work.

That expectation is where the significance of the message in the supplied photograph begins. The NCBA display states that seven of Kenya’s top ten SACCOs bank with NCBA. On the surface, it is a market-share statement. Underneath it sits a much bigger story: some of the country’s most complex member-owned financial institutions have chosen NCBA to support the money movements, risk controls and funding decisions that ultimately touch millions of Kenyans.

A SACCO may feel personal and local to its members, but a leading SACCO is a large financial institution. It receives thousands of deposits, processes payroll deductions, disburses loans, manages investment portfolios, settles supplier payments, connects to mobile and digital channels, reconciles transactions and protects member data. Its banking partner must therefore do more than open an account. It must provide dependable infrastructure.

| “The member sees a loan, a dividend or a deposit. The SACCO sees thousands of transactions. The bank behind the SACCO must see the whole system — and keep it moving.” Editorial analysis |

| What the “7 of the top 10” claim does — and does not — tell us It signals that NCBA has won substantial trust among large SACCO institutions. It does not, by itself, reveal the identities of the seven SACCOs or the ranking methodology. The more useful question is therefore not simply “who are the seven?” but “what capabilities would make leading SACCOs repeatedly choose the same bank?” |

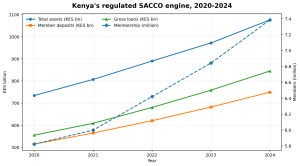

Kenya’s SACCO economy is now a trillion-shilling system

SACCOs are sometimes discussed as though they are an informal side channel to mainstream banking. The numbers show the opposite. SASRA data indicate that the assets of regulated SACCOs grew from KES 734.2 billion in 2020 to about KES 1.076 trillion in 2024. Over the same period, member deposits rose from KES 514.5 billion to KES 749.4 billion, while gross loans expanded from KES 555.1 billion to KES 845.1 billion. Membership increased from about 5.82 million to 7.39 million.

That is roughly 10.0% annualised growth in assets, 9.9% in deposits, 11.1% in loans and 6.1% in membership over four years. In practical terms, a bank serving the largest SACCOs is helping to carry part of a financial system that is growing faster than many households realise.

Figure 1: Growth of regulated SACCO assets, deposits, loans and membership, 2020-2024

Source: SASRA, Sacco Supervision Annual Reports 2023 and 2024. Values rounded.

This scale changes the standard by which a SACCO banking partner should be judged. A delay in a reconciliation file is not a minor inconvenience when tens of thousands of member records are involved. A weak collection channel can slow loan repayments. A cyber incident can damage years of trust. An inadequate liquidity arrangement can force a SACCO to postpone lending when members need it most. Institutional banking, in this environment, is operational infrastructure.

Why leading SACCOs would choose NCBA: seven practical reasons

| 1. NCBA treats SACCOs as a specialised institutional segment The first advantage is focus. NCBA publicly describes a SACCO banking proposition built around transactional banking, cash management, digital banking, investments, trade finance, foreign exchange and dedicated relationship management. That is materially different from handing a SACCO a standard business account and asking it to adapt. A large SACCO’s needs cut across departments. It may require a collection solution for monthly remittances, a credit line for liquidity, treasury support for surplus funds, asset finance for vehicles or equipment, and an integration path between its core system and the bank. A specialised desk reduces the risk that every request starts from zero. |

| 2. It provides the transaction rails that make member service feel effortless The most visible SACCO experience is often the least visible banking work. Members want payments to reflect quickly, deductions to be allocated correctly and withdrawals to reach the right destination. NCBA’s corporate transaction channels include host-to-host integration, APIs, bulk payments, direct debits, M-Pesa collections, PesaLink, cash-management tools and corporate internet banking with audit trails and approval controls. For a SACCO, these are not decorative digital features. They reduce manual file handling, duplicate entries, and reconciliation delays. They also create a cleaner trail for internal audit and management oversight. When the underlying rails work, the member experiences speed. When they fail, the SACCO absorbs the frustration. |

| 3. It can support liquidity, lending and asset acquisition under one relationship SACCOs collect deposits and extend credit, but the timing of cash inflows and member demand does not always match perfectly. School-opening periods, dividend seasons, payroll cycles and agricultural calendars can create sudden pressure. A capable banking partner must understand those cycles and respond with appropriate liquidity and credit structures rather than generic lending. NCBA’s broader strength in corporate banking and asset finance gives it room to support working-capital needs, structured facilities and acquisition of operational assets. The benefit is not only access to money; it is the ability to structure money around the SACCO’s cash-flow reality. |

| 4. Cybersecurity and control are treated as core business issues The cooperative model depends on trust, and trust now lives partly in code. SACCOs hold identity records, member balances, loan histories and payment instructions. As digital access expands, so does exposure to phishing, credential theft, social engineering, system intrusion and insider abuse. NCBA has publicly worked with SACCOs on cyber resilience and has linked that work to solutions such as virtual accounts for diaspora remittances, check-off automation, open banking and automated direct debits. The strategic value is clear: innovation must be paired with authentication, segregation of duties, monitoring, backups and incident response. A fast system without strong controls is merely a faster route to loss. |

| 5. Treasury, foreign exchange and diaspora flows can be managed within the same ecosystem A mature SACCO does not only collect deposits and lend. It also manages liquidity surpluses, investment maturities, cross-border payments, donor or employer relationships and, increasingly, diaspora member flows. These activities create foreign-exchange, counterparty and timing risks that require specialist support. NCBA’s treasury, investment, and foreign-exchange capabilities allow a SACCO to consolidate more of that activity with a single institution. That can improve visibility, speed up decisions and reduce the fragmentation that arises when collections, investments and international payments sit in unrelated systems. |

| 6. The balance sheet is large enough to inspire institutional confidence Institutional clients look beyond advertising. They examine capital, liquidity, profitability, asset quality, operational continuity and the bank’s capacity to invest in technology. NCBA ended 2025 with total assets of about KES 716.0 billion, customer deposits of KES 531.9 billion and profit after tax of KES 23.4 billion. Profit after tax grew from KES 4.6 billion in 2020, an annualised increase of about 38.6% over five years. The line chart also shows that balance sheets do not move in a perfectly straight line. Assets and deposits rose strongly through 2023, adjusted in 2024 and strengthened again in 2025. The important institutional signal is resilience: earnings continued to grow while the group maintained substantial scale. |

Figure 2: NCBA total assets, customer deposits and profit after tax, 2020-2025

Source: NCBA Group annual reports and audited financial statements. Values rounded.

| Latest available snapshot: Q1 2026 NCBA reported total assets of KES 741.1 billion, customer deposits of KES 544.4 billion and profit after tax of approximately KES 6.0 billion for the quarter ended 31 March 2026. Profit was about 9% higher than in Q1 2025, and the reported group liquidity ratio was 63.9%. These are important indicators of capacity, although no single quarter should be used alone to judge a bank. |

| 7. Technology is backed by people who understand the institution Banking relationships become most valuable when something is unusual: a failed bulk file, a new collection structure, a liquidity squeeze, a regulatory query or a system integration that requires several teams to work together. At that moment, the SACCO needs accountable people, not a maze of generic channels. NCBA’s SACCO proposition emphasises dedicated relationship management and customised solutions. That human layer matters because every SACCO has its own bylaws, employer linkages, member demographics, branch footprint and technology stack. Digital scale solves repetition; experienced relationship teams solve exceptions. |

The strongest banking partnership is felt even when the member never sees it

For an ordinary member, the identity of a SACCO’s banker may appear remote. Yet the quality of that bank can influence the services the member experiences every day. A stronger collection and reconciliation setup can help deductions reflect sooner. Better liquidity planning can support timely loan disbursement. Secure digital channels can reduce the risk of fraud. Reliable payments infrastructure can make supplier, dividend, and refund payments more predictable.

| Member outcome | How the banking infrastructure contributes |

| Faster reflection of funds | Integrated collections and automated reconciliation reduce the time between payment and correct member allocation. |

| More dependable access to credit | Liquidity and funding facilities can help the SACCO respond to seasonal or unusually high loan demand. |

| Safer digital service | Layered controls, audit trails and cyber-resilience measures protect transactions and member information. |

| Better institutional decisions | Treasury visibility, reporting and relationship support help management deploy member funds more deliberately. |

This is why the “seven of the top ten” message has resonance beyond corporate bragging rights. If a bank is deeply embedded in the institutions that hold members’ savings and finance their homes, education, farms and businesses, its reliability becomes part of the country’s economic plumbing.

THE WIDER PROPOSITION

Why this makes NCBA a compelling bank of choice in Kenya

The case for NCBA is strongest when its capabilities are considered together. It combines a sizeable balance sheet, rising profitability, corporate transaction technology, a strong asset-finance franchise, digital lending scale, regional reach and a sector-specific SACCO proposition. Many banks can offer one or two of these strengths. Fewer can bring them into one coordinated relationship.

For a large SACCO, that coordination can reduce operational fragmentation. For a business, it can mean combining collections, payments, credit, asset finance and treasury support. For an individual, it can mean access to a bank whose systems serve both everyday retail needs and complex institutions. The same discipline required to process a SACCO’s bulk files or protect its digital channels should, when executed consistently, improve the bank’s wider service culture.

This does not mean NCBA will be the cheapest or perfect choice for every customer, product or transaction. Responsible banking decisions still require a comparison of fees, interest rates, eligibility, service locations, digital reliability and the exact terms offered. “Best bank” should never be reduced to a slogan. It should be earned through relevance, resilience and execution.

| “NCBA’s most persuasive advertisement is not the size of its logo. It is the confidence of institutions that must protect other people’s money every single day.” Conclusion |

On that test, the SACCO statistic is powerful. Leading SACCOs are demanding clients. They operate under regulation, answer to boards and members, handle high transaction volumes and carry reputational risk on every member balance. Winning their trust suggests that NCBA has built more than products; it has built infrastructure, expertise and relationships that can operate at institutional scale.

The result is a credible positioning: NCBA is not merely a bank participating in Kenya’s growth story. It is one of the institutions helping the country’s cooperative economy collect, move, protect and multiply capital. That is why seven of the top ten SACCOs banking with NCBA matter — and why the bank has a strong claim to be considered among the best places to bank in Kenya.

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (279)

- August 2026 (62)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)