Why the Nairobi Securities Exchange Deserves A Place In Every Serious Long-term Wealth Plan

For years, many Kenyans have treated wealth as something that happens somewhere else. We watch banks announce record profits, Safaricom report billions from M-PESA, insurers expand across the region and major companies distribute dividends, yet most households participate only as customers. We pay the transaction fees, service the loans, buy the airtime, renew the policies and consume the products. The Nairobi Securities Exchange offers a different relationship with the same economy: ownership.

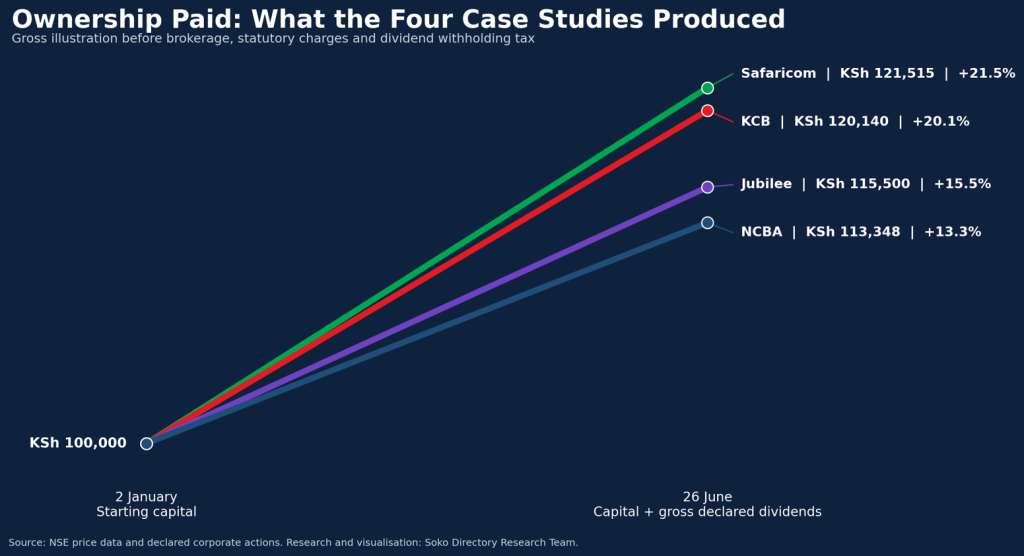

The evidence from the first half of 2026 is difficult to ignore. A simplified KSh 100,000 investment made at the beginning of January in Safaricom, KCB Group, Jubilee Holdings or NCBA Group would have appreciated materially by 26 June. Using the same price points applied in the four Soko Directory case studies, Safaricom would have produced gross total wealth of about KSh 121,515 after including the KSh 0.85 interim dividend. KCB would have reached roughly KSh 120,140 after its declared KSh 3.00 dividend. Jubilee Holdings would have stood at about KSh 115,500 after the KSh 13.00 dividend entitlement, while NCBA would have reached approximately KSh 113,348 after the declared KSh 4.60 dividend. These are gross illustrations before brokerage, statutory charges and withholding tax, but the message is still powerful: ownership created value while cash sitting idle continued to lose purchasing power.

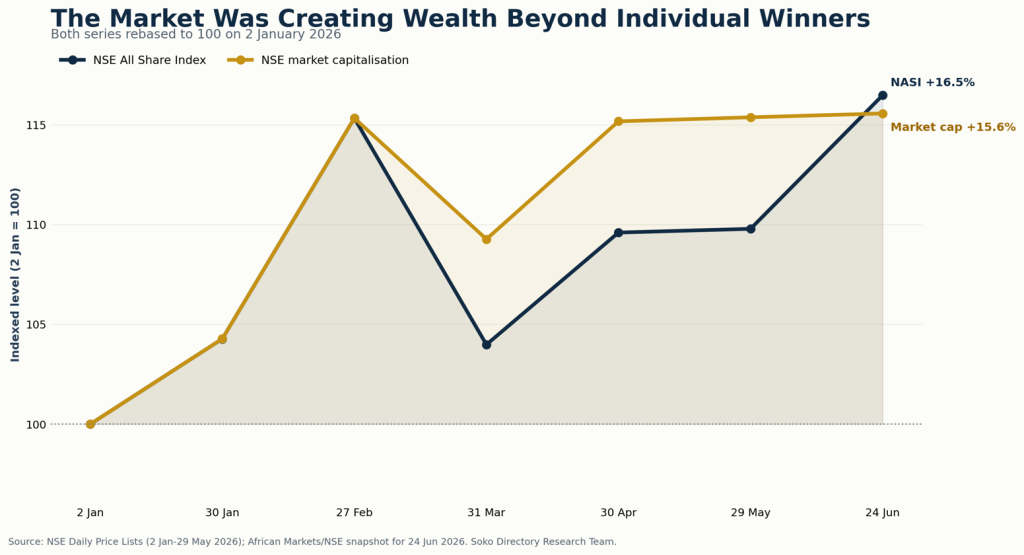

This was not simply a story of one lucky counter. The NSE All Share Index rose from 187.35 on 2 January to 222.42 on 26 June, an increase of about 18.7 per cent before dividends. Over roughly the same period, market capitalisation moved from about KSh 2.96 trillion at the opening of the year to about KSh 3.42 trillion by 24 June. That means hundreds of billions of shillings in quoted market value were created across the exchange, not hidden in a private deal that ordinary investors could never access, but visible in a regulated public market where a normal-board trade can be as small as one share.

Read Also: The Kenyan Stock Market Closes The Week Tumbling Down As Foreign Investors Drive Sell-Off

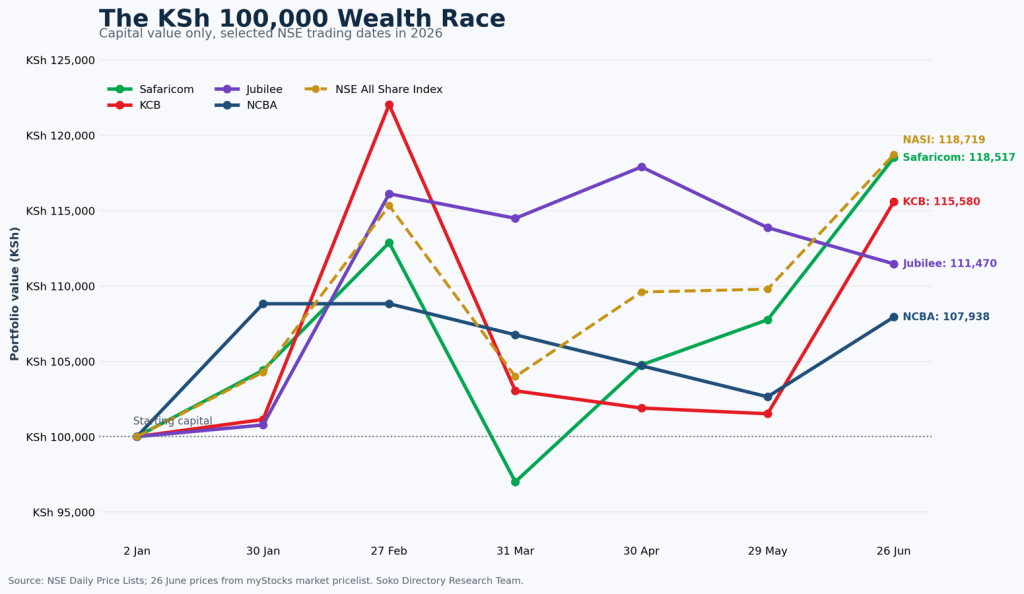

Figure 1: The four shares were volatile, but each ended above the January starting value. The NASI line shows that the wider market also advanced strongly. Capital values exclude dividends.

The graph matters because it destroys two myths at once. The first myth is that shares move in a straight line. They do not. February was strong, March delivered a visible pullback, and the four counters did not move together. That volatility is the price of participating in productive businesses whose valuations respond to earnings, interest rates, regulation, investor flows and changing expectations. The second myth is that volatility makes the market useless for wealth creation. It does not. Volatility becomes destructive mainly when an investor buys blindly, concentrates everything in one counter, borrows to speculate or sells in panic. For a disciplined investor, price fluctuations are not proof that ownership has failed; they are a reminder that wealth requires time, diversification and emotional control.

An equal KSh 25,000 allocation to the four companies would have grown to about KSh 117,596 after adding gross declared dividends, a return of roughly 17.6 per cent in less than six months. That basket would have combined telecommunications, banking and insurance rather than depending on one business model. It would also have produced cash income through dividends, demonstrating the two engines of equity wealth: capital appreciation and distributions from corporate profits. The best investors understand that the share price is only one part of the return. Dividends can be reinvested to buy more shares, those shares can earn future dividends, and the compounding cycle can continue for years.

The four companies also represent real economic infrastructure. Safaricom is not a screen symbol detached from daily life; it is a communications, data and payments platform whose FY2026 group service revenue reached KSh 414.1 billion and whose net income approached KSh 100 billion. KCB Group reported FY2025 profit after tax of KSh 68.4 billion and followed it with KSh 24.4 billion in pre-tax profit in the first quarter of 2026, up 15.3 per cent. NCBA delivered KSh 23.4 billion in FY2025 profit after tax and reported KSh 6.0 billion in the first quarter of 2026, nine per cent higher than a year earlier. Jubilee Holdings reported an 18 per cent rise in 2025 net profit to KSh 5.6 billion and declared a record KSh 13 dividend. Buying their shares is not chasing abstract numbers. It is acquiring a claim on businesses earning money from communication, credit, payments, asset finance, regional banking, health, life and general insurance.

Figure 2: Gross total shareholder value on 26 June 2026. Dividends are included as declared entitlements; taxes and trading costs would reduce realised proceeds.

Read Also: KCB Leads The Charge In A Promising Stock Market Year: A Closer Look at Top Performers

The comparison with the wider economy is equally important. In late June, the Central Bank Rate stood at 8.75 per cent, the 91-day Treasury-bill rate was about 8.83 per cent, the average deposit rate was 6.88 per cent and the average savings rate was only 3.31 per cent. Inflation was 6.68 per cent in May, while the average commercial-bank lending rate remained 14.69 per cent in April. These figures are not directly comparable because Treasury-bill, deposit and lending rates are annual rates while the share returns above cover about six months, and equities carry substantially more risk. Even with that caution, the contrast is revealing. Money that does not earn above inflation is quietly shrinking in real terms. A serious wealth plan therefore needs assets capable of growing faster than the cost of living over time.

That does not mean every shilling should be thrown into shares. An emergency fund belongs in liquid, low-risk instruments. School fees due next term should not be exposed to market swings. Rent, payroll and working capital should not be gambled on a short-term price forecast. The correct argument is more disciplined: after protecting essential liquidity, Kenyans who want long-term wealth should convert part of their recurring income into ownership of productive assets. The NSE is one of the clearest places to do that because it provides transparent prices, audited disclosures, regulated intermediaries, corporate actions, settlement infrastructure and the ability to sell when liquidity is needed.

The exchange is also changing. The Kenya Pipeline Company and Africa Logistics REIT listings in March 2026 widened the menu of investable assets. Family Bank began trading in June, adding another banking counter. Safaricom’s Ziidi Trader has placed share-market access inside the M-PESA ecosystem, reducing the psychological and practical distance between a mobile-money user and a securities investor. The NSE’s own strategy targets millions of active retail investors, while new derivatives, REITs, exchange-traded funds, corporate bonds and government securities are gradually turning the market from a narrow share-trading venue into a broader capital-allocation platform.

This evolution matters because Kenya cannot borrow and tax its way into prosperity forever. A country creates sustainable wealth when household savings finance productive businesses, those businesses invest and employ people, and citizens share in the value created. The stock exchange is the bridge. It moves capital from consumption today into factories, networks, branches, technology, logistics, housing, insurance pools and regional expansion. It also imposes discipline. Listed companies must publish results, disclose material information, hold shareholder meetings and face daily market judgment. Public ownership does not eliminate failure, but it creates visibility that private arrangements often lack.

Figure 3: The rally was market-wide. From 2 January to 24 June, both the broad index and total quoted market value moved materially higher, although the path included a sharp March correction.

The March correction shown in the graph should be studied, not hidden. It is the best argument for investing gradually rather than trying to identify one perfect entry date. A Kenyan who commits a fixed amount every month buys fewer shares when prices are high and more when prices are lower. This approach, commonly called cost averaging, replaces prediction with a system. The habit matters more than the drama of one trade. KSh 5,000 invested consistently, diversified carefully and reinvested over many years can be more powerful than KSh 100,000 invested once and then abandoned.

Research must sit at the centre of that habit. A share is not attractive merely because its price has fallen, and a company is not safe merely because its brand is familiar. Investors should examine profitability, cash generation, debt, asset quality, governance, dividend sustainability, competitive position and valuation. Bank investors must understand non-performing loans and capital adequacy. Insurance investors must consider underwriting performance and investment income. Telecommunications investors must follow regulation, capital expenditure, customer growth and the economics of new markets. The NSE rewards ownership, but it does not reward laziness consistently.

Diversification is equally non-negotiable. The four case studies performed well, but that does not prove they will lead in the next six months. A responsible portfolio should spread exposure across businesses and, where appropriate, combine equities with Treasury securities, money-market funds, pension savings, REITs or other regulated assets. The objective is not to win every week. It is to avoid one mistake destroying years of savings while allowing successful companies and compounding income to carry the portfolio forward.

There is also a cultural change Kenya must make. Too many people understand the monthly cost of a loan better than the annual dividend of a share. We can calculate a vehicle instalment instantly but hesitate to open a CDS account. We celebrate consumption publicly and build ownership privately, if at all. The result is an economy where citizens help create corporate profits but do not receive enough of the profit distribution. The solution is not to stop consuming or borrowing completely. It is to ensure that part of every productive season is converted into assets that can work after the salary, contract or business sale has been spent.

The lesson from Safaricom, KCB, Jubilee and NCBA is therefore bigger than four price charts. It is that the Nairobi Securities Exchange can translate economic participation into personal ownership. It gives a teacher, farmer, journalist, entrepreneur, driver, civil servant or student’s family a legal route to own part of the companies they encounter every day. It allows wealth to be built in units smaller than a plot of land, without waiting to raise millions for a building, and without managing tenants, stock or employees. It makes capital divisible, visible and transferable.

The NSE is not a casino, and it should never be marketed as one. It is a marketplace for claims on real assets and future cash flows. Prices can fall. Dividends can be cut. Companies can disappoint. Past performance cannot promise future returns. But refusing to invest also carries a risk: inflation, missed compounding and permanent dependence on earned income. The answer is not reckless speculation. The answer is educated, regulated, diversified and patient ownership.

Kenya’s next wealth revolution will not come only from discovering another hustle. It will come when millions of people learn to preserve the proceeds of their hustle by buying productive assets. It will come when workers become shareholders, entrepreneurs invest outside their own businesses, young adults begin before obligations become overwhelming, and families teach children the difference between buying from a company and owning it. The Nairobi Securities Exchange is not the only place to create wealth, but the data shows that it deserves to become one of the first places a serious Kenyan wealth builder considers. Stop watching companies make money. Study them. Value them. Own them. Let the economy you help build begin paying you back.

Read Also: Kenyan Stock Market Shows Mixed Performance Amid Currency Fluctuations

About Steve Biko Wafula

Steve Biko is the CEO OF Soko Directory and the founder of Hidalgo Group of Companies. Steve is currently developing his career in law, finance, entrepreneurship and digital consultancy; and has been implementing consultancy assignments for client organizations comprising of trainings besides capacity building in entrepreneurial matters.He can be reached on: +254 20 510 1124 or Email: info@sokodirectory.com

- January 2026 (220)

- February 2026 (248)

- March 2026 (287)

- April 2026 (208)

- May 2026 (191)

- June 2026 (238)

- July 2026 (278)

- August 2026 (43)

- January 2025 (119)

- February 2025 (191)

- March 2025 (212)

- April 2025 (193)

- May 2025 (161)

- June 2025 (157)

- July 2025 (227)

- August 2025 (211)

- September 2025 (267)

- October 2025 (297)

- November 2025 (230)

- December 2025 (220)

- January 2024 (238)

- February 2024 (227)

- March 2024 (190)

- April 2024 (133)

- May 2024 (157)

- June 2024 (145)

- July 2024 (136)

- August 2024 (154)

- September 2024 (212)

- October 2024 (255)

- November 2024 (196)

- December 2024 (143)

- January 2023 (182)

- February 2023 (203)

- March 2023 (322)

- April 2023 (297)

- May 2023 (267)

- June 2023 (214)

- July 2023 (212)

- August 2023 (257)

- September 2023 (237)

- October 2023 (264)

- November 2023 (286)

- December 2023 (177)

- January 2022 (293)

- February 2022 (329)

- March 2022 (358)

- April 2022 (292)

- May 2022 (271)

- June 2022 (232)

- July 2022 (278)

- August 2022 (253)

- September 2022 (246)

- October 2022 (196)

- November 2022 (232)

- December 2022 (167)

- January 2021 (182)

- February 2021 (227)

- March 2021 (325)

- April 2021 (259)

- May 2021 (285)

- June 2021 (272)

- July 2021 (277)

- August 2021 (232)

- September 2021 (271)

- October 2021 (304)

- November 2021 (364)

- December 2021 (249)

- January 2020 (272)

- February 2020 (310)

- March 2020 (390)

- April 2020 (321)

- May 2020 (335)

- June 2020 (327)

- July 2020 (333)

- August 2020 (276)

- September 2020 (214)

- October 2020 (233)

- November 2020 (242)

- December 2020 (187)

- January 2019 (251)

- February 2019 (215)

- March 2019 (283)

- April 2019 (254)

- May 2019 (269)

- June 2019 (249)

- July 2019 (335)

- August 2019 (292)

- September 2019 (306)

- October 2019 (313)

- November 2019 (362)

- December 2019 (318)

- January 2018 (291)

- February 2018 (213)

- March 2018 (275)

- April 2018 (223)

- May 2018 (235)

- June 2018 (176)

- July 2018 (256)

- August 2018 (247)

- September 2018 (255)

- October 2018 (282)

- November 2018 (282)

- December 2018 (184)

- January 2017 (183)

- February 2017 (194)

- March 2017 (207)

- April 2017 (104)

- May 2017 (169)

- June 2017 (205)

- July 2017 (189)

- August 2017 (195)

- September 2017 (186)

- October 2017 (235)

- November 2017 (253)

- December 2017 (266)

- January 2016 (164)

- February 2016 (165)

- March 2016 (189)

- April 2016 (143)

- May 2016 (245)

- June 2016 (182)

- July 2016 (271)

- August 2016 (247)

- September 2016 (233)

- October 2016 (191)

- November 2016 (243)

- December 2016 (153)

- January 2015 (1)

- February 2015 (4)

- March 2015 (164)

- April 2015 (107)

- May 2015 (116)

- June 2015 (119)

- July 2015 (145)

- August 2015 (157)

- September 2015 (186)

- October 2015 (169)

- November 2015 (173)

- December 2015 (205)

- March 2014 (2)

- March 2013 (10)

- June 2013 (1)

- March 2012 (7)

- April 2012 (15)

- May 2012 (1)

- July 2012 (1)

- August 2012 (4)

- October 2012 (2)

- November 2012 (2)

- December 2012 (1)